How to Remove Collections from Your Credit Report in 2026 (Step-by-Step)

Ashley Rivera

Credit Repair Specialist

Having a collection account on your credit report feels like carrying a financial anchor — it drags down your score, limits your borrowing power, and can follow you for up to seven years. But here’s what most people don’t know: you have more power to remove collections from your credit report than you think.

This guide breaks down every legitimate strategy available in 2026 — from disputing inaccurate entries to negotiating pay-for-delete agreements — so you can take action and start rebuilding your credit today.

What Is a Collection Account and How Does It Hurt Your Credit?

When you fall behind on a debt — a medical bill, credit card, or utility account — the original creditor may eventually sell or transfer that debt to a collection agency. Once that happens, a collection account appears on your credit report.

A single collection account can drop your credit score by 50 to 100+ points, depending on how high your score was and how recently the collection occurred. More recent collections hurt more. That said, FICO 9 and VantageScore 4.0 no longer count paid collections against you — which is why getting these resolved matters.

Collections stay on your credit report for seven years from the date of first delinquency — unless you successfully dispute or remove them sooner.

Step 1: Pull All Three Credit Reports

Before you do anything, get your free credit reports from all three bureaus — Equifax, Experian, and TransUnion — at AnnualCreditReport.com. You’re entitled to free weekly reports through 2026.

Document every collection account you find, noting:

- The collection agency name

- The original creditor

- The date of first delinquency

- The balance owed

- Whether it’s marked as paid or unpaid

Step 2: Check the Collection for Errors

Here’s a powerful truth: many collection accounts contain errors. According to the FTC, 1 in 5 consumers has a mistake on at least one credit report. Common collection errors include:

- Wrong balance amount

- Incorrect date of first delinquency (this affects the 7-year removal clock)

- Accounts that don’t belong to you (identity theft or mixed files)

- Duplicate entries for the same debt

- Paid collections still showing as unpaid

If you find any inaccuracy, you have the right to dispute it — and if the bureau can’t verify it within 30 days, they must remove it.

Step 3: Dispute Inaccurate Collections with the Credit Bureaus

Send a dispute letter to each bureau reporting the inaccurate collection. You can dispute online, by phone, or by certified mail (mail is recommended — it creates a paper trail).

Your dispute letter should include:

- Your full name and address

- A clear description of the error

- Copies (not originals) of supporting documents

- A request to correct or delete the entry

Under the Fair Credit Reporting Act (FCRA), bureaus must investigate disputes within 30 days. If they can’t verify the information, it must be removed.

Pro Tip: Dispute each bureau separately. An item removed from Experian may still appear on Equifax and TransUnion.

Step 4: Send a Debt Validation Letter to the Collection Agency

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request proof that a debt is yours and that the amount is correct. This is called a debt validation letter, and it must be sent within 30 days of first contact from the collector.

If the collection agency can’t provide proper validation, they must stop collection activity and have the item removed from your credit report.

A solid debt validation letter asks for:

- Proof the collector owns or is authorized to collect the debt

- A copy of the original signed agreement

- Complete payment history

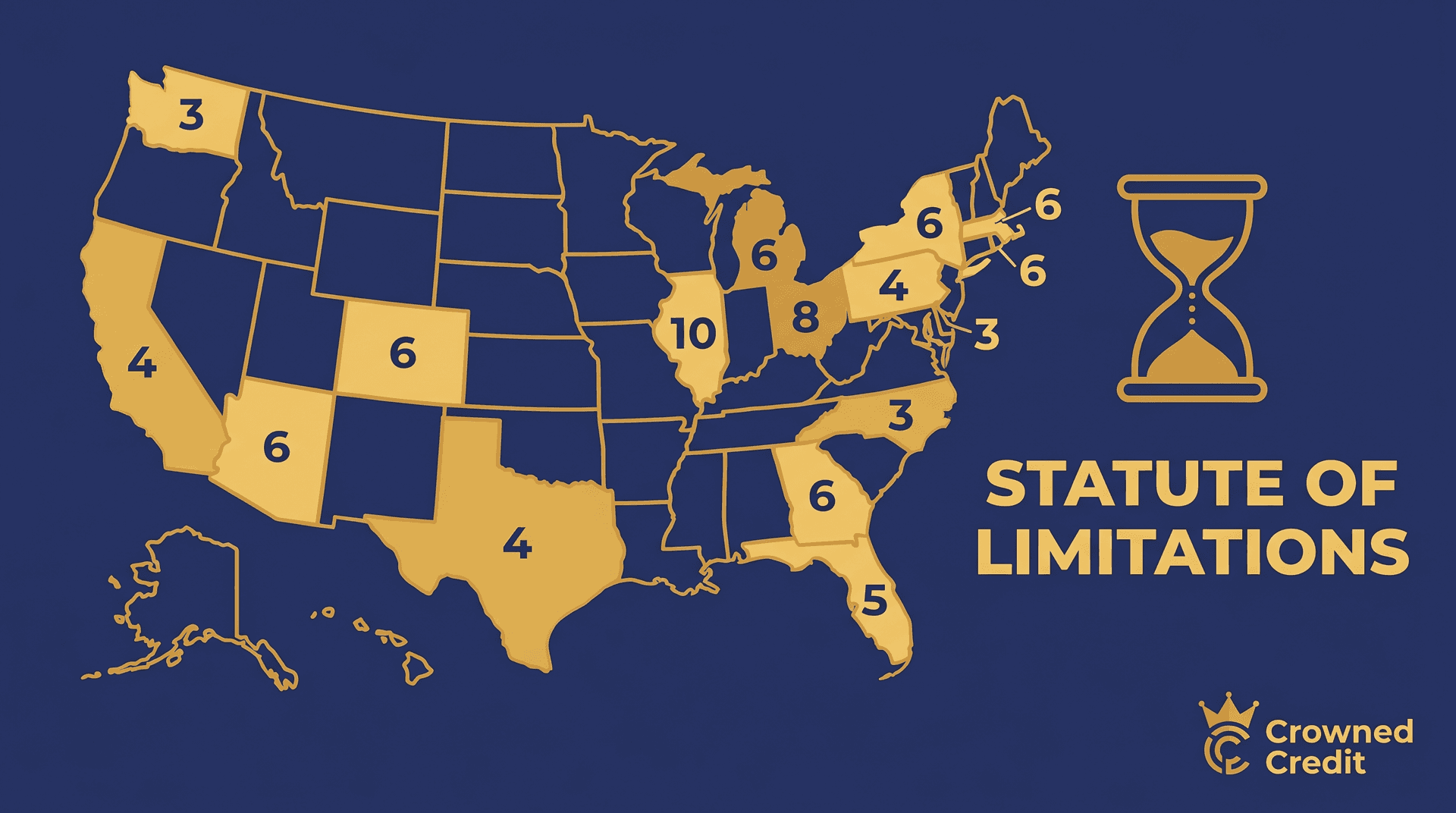

- Proof the statute of limitations hasn’t expired

Step 5: Negotiate a Pay-for-Delete Agreement

If the debt is valid and yours, consider negotiating a pay-for-delete — an agreement where you pay the debt (in full or as a settlement) in exchange for the collector removing the entry from your report.

Key points about pay-for-delete:

- Get the agreement in writing before you pay

- Not all collectors will agree (original creditors are often more resistant than third-party collectors)

- Even if they won’t delete it, paying a collection changes its status to “paid,” which still improves your score under newer FICO and VantageScore models

Step 6: Send a Goodwill Deletion Letter

If the debt is already paid or you have a strong payment history elsewhere, try a goodwill deletion letter. This is a letter asking the creditor or collection agency to remove the negative entry as a gesture of goodwill, acknowledging you’ve gotten back on track.

This strategy works best when:

- The collection is older and isolated

- You have an otherwise good payment record

- The amount was relatively small

It won’t work every time, but it costs nothing to try and has helped thousands of consumers clean up their reports.

Step 7: Get Professional Help to Accelerate Results

If you want faster results and expert-level dispute strategy, working with a professional credit repair company makes a significant difference. A reputable firm knows the laws, the dispute processes, and how to challenge collection accounts in ways that get results faster than going it alone.

At Crowned Credit, we’ve helped thousands of clients remove inaccurate and unverifiable collection accounts from their reports — legally and efficiently. Our process is transparent, compliant, and built around your specific credit situation.

👉 See our pricing options here or get started with a free consultation today.

What About Medical Collections?

Medical debt collections are treated differently in 2026 than in prior years. The CFPB has proposed rules to remove medical debt from credit reports entirely, and the three major bureaus have already removed paid medical collections and collections under $500 from credit reports.

If you have a medical collection showing on your report that’s paid or under $500, dispute it immediately — it shouldn’t be there.

Frequently Asked Questions

How long does it take to remove a collection from my credit report?

If you’re disputing an error, credit bureaus have 30 days to investigate. If the dispute is successful, the account can be removed within 30–45 days. More complex situations may take 3–6 months.

Does paying a collection remove it from my credit report?

Not automatically. Paying a collection changes its status to “paid,” which helps with newer scoring models. To get it fully removed, you’d need a pay-for-delete agreement in writing before paying.

Can I remove a collection I actually owe?

Yes — through pay-for-delete negotiations or if the collection agency fails to properly validate the debt. Even valid debts can be removed if the collector can’t meet legal verification requirements.

Will removing a collection raise my credit score?

Yes. Removing a collection — especially a recent one — can increase your score by 50–150 points depending on your overall credit profile.

Should I hire a credit repair company to remove collections?

If you have multiple collections, errors across multiple bureaus, or you’re short on time and knowledge of the law, professional help is often worth the investment. Crowned Credit offers transparent, results-focused credit repair services.

Ready to take control of your credit? Explore our plans or get started today — your better credit score is closer than you think.

Disclaimer: Results vary by individual. Credit repair timelines depend on your unique credit history and the nature of the items being disputed. Crowned Credit cannot guarantee specific results or timeframes.