How to Remove Hard Inquiries From Your Credit Report in 2026

Ashley Rivera

Credit Repair Specialist

You checked your credit report and found six hard inquiries you don't remember authorizing. Maybe it was a car dealership that shotgunned your application to twelve lenders. Maybe a cell phone store ran your credit without telling you. Or maybe someone opened accounts in your name entirely.

Whatever the cause, those hard inquiries are sitting on your report — and while each one only costs you about 5 to 10 points individually, stack a handful of them together and you're looking at a 30 to 50 point drop that makes everything from mortgage rates to auto loans more expensive.

The good news: you have legal rights under the Fair Credit Reporting Act (FCRA) to dispute any inquiry that shouldn't be on your report. Here's exactly how to do it in 2026.

What Counts as a Hard Inquiry (And What Doesn't)

Before you start disputing everything, you need to understand the difference between hard and soft inquiries — because only one of them actually affects your score.

Hard inquiries happen when a lender or creditor pulls your credit because you applied for something: a credit card, mortgage, auto loan, personal loan, apartment rental, or even a new cell phone plan. You typically have to authorize these, either by signing an application or clicking "agree" online.

Soft inquiries happen when someone checks your credit for non-lending purposes — like when you check your own score on Credit Karma, when a company sends you a pre-approved offer in the mail, or when an employer runs a background check. Soft pulls don't affect your score at all and don't show up to lenders.

Here's a quick breakdown:

- Hard pulls (affect score): Credit card applications, mortgage pre-approvals with full applications, auto loan applications, personal loan applications, apartment applications (some landlords), cell phone contracts

- Soft pulls (no score impact): Checking your own credit, pre-qualification offers, employer background checks, insurance quotes, account reviews by existing creditors

One important exception: rate shopping. If you're comparing mortgage rates or auto loan rates, multiple hard inquiries within a 14 to 45 day window (depending on the scoring model) count as a single inquiry. FICO and VantageScore both have this built in because they recognize that shopping around for the best rate is responsible behavior, not a sign of financial distress.

How Much Do Hard Inquiries Actually Hurt Your Score?

FICO says a single hard inquiry typically lowers your score by fewer than 5 points. That doesn't sound like much until you consider a few things:

- They stack up. Three unauthorized inquiries from a dealership that ran your credit at multiple banks? That's potentially 15 points gone.

- They stick around for 2 years. Hard inquiries stay on your report for 24 months, though they usually stop affecting your score after about 12 months.

- They matter most when you're borderline. If you're sitting at a 618 and need a 620 for an FHA loan, those 5 points from a hard inquiry are the difference between approval and denial.

- Multiple inquiries signal risk. Lenders see a cluster of recent hard pulls and think: "This person is desperately seeking credit." That perception alone can influence underwriting decisions beyond just the score number.

Inquiries make up roughly 10% of your FICO score calculation under the "New Credit" category. It's the smallest factor — behind payment history (35%), amounts owed (30%), length of credit history (15%), and credit mix (10%) — but when every point matters, it's worth addressing.

When Can You Legally Remove a Hard Inquiry?

Under the FCRA, creditors are required to verify the accuracy of everything they report to the credit bureaus — and that includes hard inquiries. You have the right to dispute any inquiry, and the bureau must investigate within 30 days.

The strongest cases for removal include:

1. Unauthorized inquiries

You never applied for credit with that company. Maybe a car dealership ran your credit at multiple lenders without your explicit consent for each one. Maybe a store clerk signed you up for a credit card you didn't ask for. These are the easiest to get removed because you can demonstrate you never authorized the pull.

2. Fraudulent inquiries

Someone used your personal information to apply for credit. This is identity theft, and the FCRA gives you strong protections. You can file a dispute with each bureau, submit an FTC identity theft report, and request a fraud alert or credit freeze.

3. Duplicate inquiries from rate shopping

If the scoring model didn't properly group your rate-shopping inquiries into a single event, you can dispute the extras. This happens more often than you'd think, especially with auto loans where dealerships submit applications to multiple lenders on the same day.

4. Inquiries that can't be verified

Here's where it gets interesting. When you dispute an inquiry, the credit bureau contacts the creditor to verify it. If the creditor can't — or simply doesn't — respond within 30 days, the bureau must remove the inquiry under Section 611 of the FCRA. Companies merge, close, or simply lose records. It happens.

Step-by-Step: How to Dispute Hard Inquiries in 2026

You can handle this yourself, and here's exactly how to do it:

Step 1: Pull All Three Credit Reports

Go to AnnualCreditReport.com and pull your reports from Experian, Equifax, and TransUnion. You get free weekly reports, so there's no excuse not to check all three.

Hard inquiries don't always appear on every bureau. A creditor might pull from just one, so you need to check each report separately. Write down every hard inquiry, the date it was made, and whether you recognize the company.

Step 2: Identify Which Inquiries to Dispute

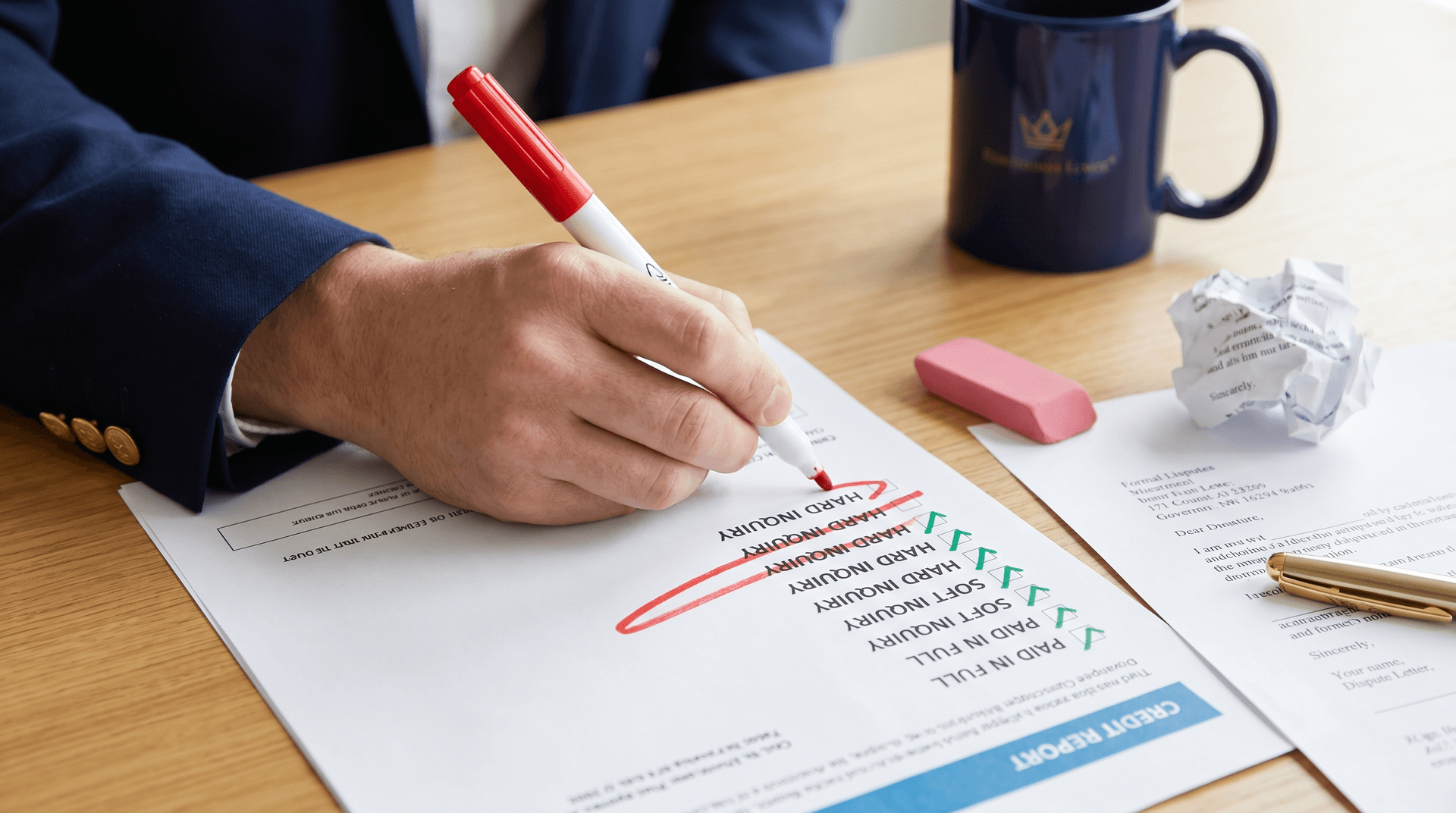

Go through each hard inquiry and sort them into three categories:

- Authorized and accurate: You applied, you remember it, it's legit. Leave these alone — they'll fall off after 2 years anyway.

- Unauthorized or unrecognized: You don't remember applying. You didn't give permission. The company name doesn't ring a bell. Dispute these.

- Suspicious or excessive: Maybe you went to one dealership and suddenly have 8 inquiries from different banks. You authorized one credit pull, not eight. Dispute the extras.

Step 3: File Disputes With Each Bureau

You need to dispute separately with each credit bureau that's showing the inquiry. Here's how:

Experian: File online at experian.com/disputes or mail a dispute letter to Experian, P.O. Box 4500, Allen, TX 75013.

Equifax: File online at equifax.com/personal/disputes or mail to Equifax Information Services LLC, P.O. Box 740256, Atlanta, GA 30374-0256.

TransUnion: File online at transunion.com/disputes or mail to TransUnion LLC, Consumer Dispute Center, P.O. Box 2000, Chester, PA 19016.

When filing, be specific. Don't write "I want all inquiries removed." Instead, identify each inquiry by company name and date and state clearly: "I did not authorize [Company Name] to pull my credit on [date]. I am requesting this unauthorized hard inquiry be investigated and removed per my rights under Section 611 of the FCRA."

Step 4: Send a Dispute Letter Directly to the Creditor

This is the step most people skip, and it's arguably the most effective. While the bureau handles one side of the investigation, you can simultaneously send a letter directly to the company that made the inquiry.

In your letter, request:

- Proof that you authorized the credit pull

- A copy of the signed application or consent form

- If they can't provide it, a request that they notify the credit bureau to remove the inquiry

Send it via certified mail with return receipt requested. This creates a paper trail that's critical if you need to escalate later.

Step 5: Follow Up and Escalate if Needed

The bureaus have 30 days to investigate (45 if you submit additional documentation during the process). If they verify the inquiry as legitimate and you disagree, you have options:

- File a complaint with the CFPB at consumerfinance.gov/complaint. CFPB complaints have teeth — companies respond to them quickly because regulators are watching.

- Add a consumer statement to your credit report explaining the dispute. It won't change your score, but lenders who manually review your report will see your side of the story.

- Consult a consumer rights attorney. Under the FCRA, you may be entitled to damages if a company violated your rights by making unauthorized credit pulls.

What About Legitimate Inquiries — Can Those Be Removed?

Technically, a hard inquiry you actually authorized is accurate information. The bureaus aren't required to remove accurate data before the 2-year expiration.

That said, there are a couple of approaches people use:

Goodwill requests: You can contact the creditor directly and ask them to remove the inquiry as a courtesy. This occasionally works with smaller lenders, credit unions, or if you ended up becoming a customer. It's a long shot, but a polite letter costs you nothing but a stamp.

Conditional removal: Some creditors will agree to remove an inquiry if you open an account with them or meet certain conditions. This is rare in 2026, but it does happen with certain credit card issuers.

The honest truth: most legitimate hard inquiries are going to stay until they age off. Your energy is usually better spent on the factors that carry more weight — like removing late payments, dealing with charge-offs, or fixing your credit utilization.

How to Prevent Unwanted Hard Inquiries

Prevention beats disputes every time. Here's how to protect yourself going forward:

Freeze your credit. A credit freeze blocks anyone from pulling your credit without you lifting the freeze first. It's free at all three bureaus and takes about 5 minutes to set up at each one. You can temporarily lift it when you actually need to apply for credit.

Read the fine print before signing anything. Car dealerships, furniture stores, electronics retailers — they all want to run your credit. Before you sign any application, ask: "Will this result in a hard inquiry on my credit report?" If you're just browsing, don't let them pull your credit.

Set up credit monitoring. Services like Credit Karma (free), Experian's free monitoring, or your bank's credit monitoring tools will alert you immediately when a new hard inquiry hits your report. The sooner you catch an unauthorized pull, the faster you can dispute it.

Use pre-qualification tools. Most major credit card issuers and lenders offer pre-qualification that uses a soft pull. Check if you're likely to be approved before you formally apply and trigger a hard inquiry.

Be direct at car dealerships. Tell the finance manager upfront: "I authorize you to pull my credit at [specific lender] only. Do not submit my application to any other lender without my written consent." Get it in writing if possible.

The Bigger Picture: Hard Inquiries vs. Everything Else

If your credit report has hard inquiries and collections, late payments, charge-offs, or high utilization — the inquiries are the least of your worries. Removing a couple of hard pulls might get you 10 to 20 points. Removing a collection account or correcting a misreported late payment could swing your score 50 to 100 points.

That's why at Crowned Credit, when clients come in focused solely on hard inquiries, we usually help them see the full picture first. A comprehensive credit report review often reveals bigger opportunities they didn't even know about — items that are hurting their score far more than a few hard pulls.

Our team works through every negative item on your report using your rights under the FCRA, challenging creditors and bureaus to verify what they're reporting. Hard inquiries are part of that process, but they're usually just one piece of a larger strategy.

If you want help tackling everything at once — inquiries, collections, late payments, charge-offs, the whole report — book a free consultation and we'll walk through your specific situation. Plans start at $150 enrollment with $99/month for our Essential plan, or $249 enrollment with $199/month for our Accelerated plan if you want faster results across all three bureaus simultaneously.

Common Myths About Hard Inquiries

There's a lot of bad advice floating around social media about hard inquiries. Let's clear some up:

Myth: "You can remove all hard inquiries with one dispute letter."

Reality: Each inquiry must be disputed individually with the specific bureau reporting it. There's no magic letter that wipes them all at once.

Myth: "Hard inquiries destroy your credit score."

Reality: They're worth about 10% of your FICO score. A single inquiry drops your score by roughly 5 points or less. They're annoying, not devastating.

Myth: "Checking your own credit creates a hard inquiry."

Reality: Checking your own credit is always a soft inquiry. Always. Check it as often as you want — it won't hurt your score.

Myth: "Hard inquiries stay on your report for 7 years."

Reality: Hard inquiries fall off after exactly 2 years. You're thinking of collections, charge-offs, and other negative items, which stick around for 7 years.

Myth: "Paying off the account removes the inquiry."

Reality: The inquiry is a record of the credit pull, not the account itself. Closing or paying off the associated account has zero effect on the inquiry.

Timeline: What to Expect When Disputing Hard Inquiries

Here's a realistic timeline so you know what you're getting into:

- Day 1: Pull your credit reports from all three bureaus and identify unauthorized inquiries

- Day 2-3: File online disputes with each bureau and send certified letters to the creditors who made the pulls

- Day 5-10: Bureaus acknowledge your dispute and begin investigation

- Day 30-45: Investigation concludes. You'll receive results by mail or through the bureau's online portal

- If removed: Your updated score should reflect the change within 1-2 billing cycles

- If not removed: Escalate to CFPB or consider professional help

When to Get Professional Help

Disputing a couple of hard inquiries? You can probably handle that yourself. But if you're dealing with a more complex situation — multiple unauthorized inquiries from identity theft, inquiries mixed in with collections and other negative items, or bureaus that aren't responding to your disputes properly — working with a credit repair professional can save you months of back-and-forth.

At Crowned Credit, we handle the entire dispute process across all three bureaus, not just for inquiries but for every negative item weighing down your report. Our team knows exactly how to leverage FCRA provisions, when to escalate to the CFPB, and how to build a dispute strategy that addresses the highest-impact items first.

Ready to clean up your credit report? Schedule your free consultation or call us at (336) 310-0090.

Disclaimer: Individual results vary. Crowned Credit does not guarantee specific credit score improvements or timelines. The credit repair process depends on individual credit profiles, creditor responses, and bureau investigation outcomes. Crowned Credit exercises your rights under the Fair Credit Reporting Act (FCRA) and other consumer protection laws on your behalf.