Credit RepairJune 2, 20268 min read

How Summer Vacation Spending Can Destroy Your Credit Score (And How to Recover)

Ashley Rivera

Credit Repair Specialist

How Vacation Spending Actually Damages Your Credit Score

Most people think that as long as they make their minimum payments, their credit score is fine. That's not how it works. Summer vacation spending hits your credit score in four specific ways:1. Credit Utilization Spikes

Your credit utilization ratio is the amount you owe divided by your total available credit. It accounts for 30% of your FICO score. Credit experts recommend keeping utilization below 30%, ideally under 10%. When you charge a $4,000 vacation to a card with a $10,000 limit, you just jumped to 40% utilization on that card. If your total credit limit across all cards is $20,000 and you previously had $2,000 in balances (10% utilization), that vacation pushed you to 30% utilization. Even worse: credit scoring models look at both per-card utilization and overall utilization. Maxing out one card hurts your score even if your overall utilization is low. A utilization spike from 10% to 40% can drop your credit score by 20-50 points immediately. The higher your utilization climbs, the more damage it does.2. Multiple New Credit Applications

Many travelers apply for new travel credit cards right before summer to get sign-up bonuses or better rewards. Each credit card application triggers a hard inquiry, which stays on your credit report for two years and can drop your score by 5-10 points per inquiry. Applying for 2-3 cards within a few months sends a red flag to credit scoring models: you're taking on new debt quickly, which statistically correlates with higher default risk. If you opened a new card and immediately maxed it out for vacation, that's even worse. New accounts with high utilization hurt more than established accounts.3. Missed or Late Payments After You Get Home

This is where vacation spending turns into long-term credit damage. You spent $5,000 on vacation, came home, and now you're facing credit card bills you can't pay in full. The minimum payments are manageable, but barely. Then life happens. An unexpected car repair. A medical bill. Another summer expense (wedding, graduation, home project). Suddenly you're juggling bills, and a credit card payment slips through the cracks. One payment that's 30+ days late stays on your credit report for seven years and can drop your score by 60-110 points. Payment history is 35% of your FICO score—the single biggest factor. Missing even one payment because of vacation overspending creates years of credit damage.4. Carrying High Balances for Months

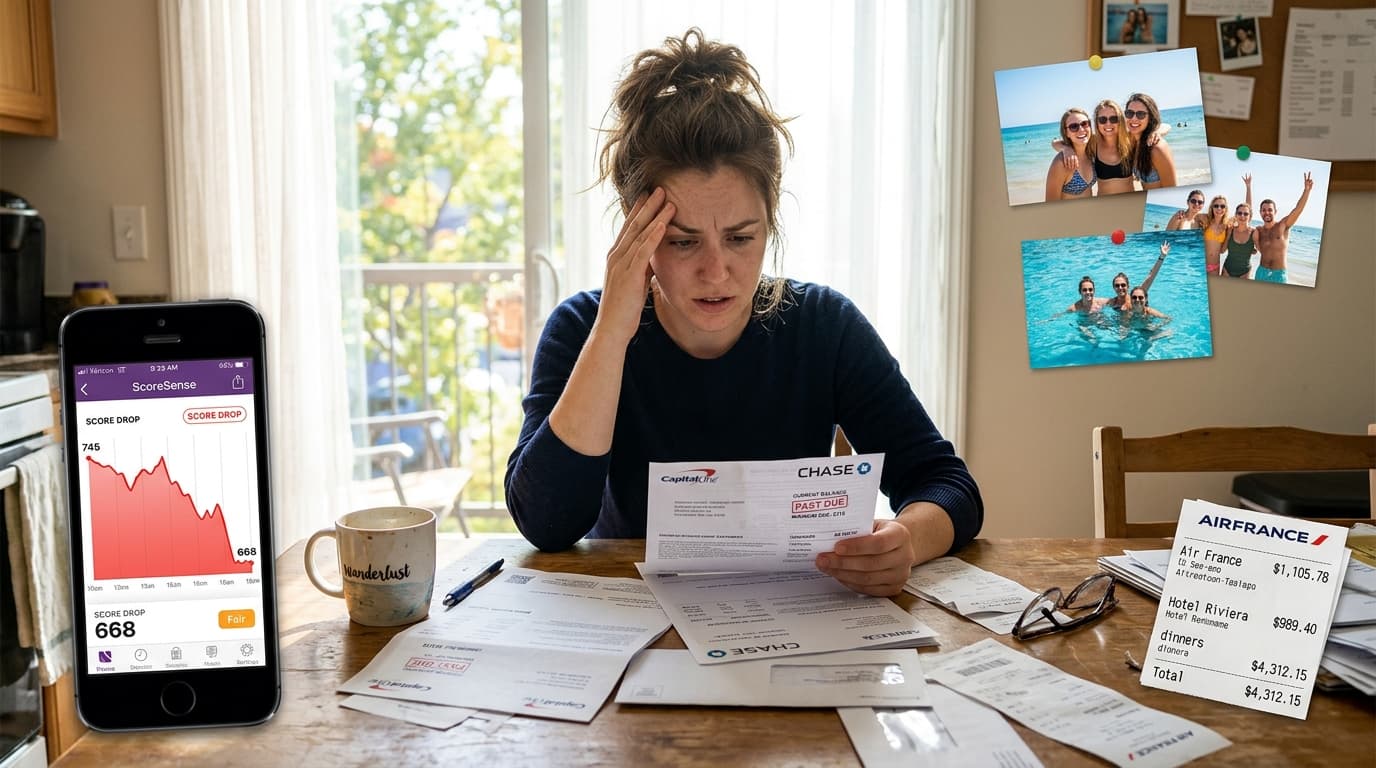

Even if you make every minimum payment on time, carrying high balances month after month keeps your utilization elevated and your score suppressed. Your credit score won't recover until those balances come down. Many people assume they can "pay it off slowly" without consequences. But every month your utilization stays high, you're being penalized. You're also paying interest that makes it harder to pay down the balance. The average credit card APR in 2026 is over 20%. If you're carrying a $5,000 vacation balance and paying $150/month, it'll take 48 months to pay off, and you'll pay $2,100 in interest. Your credit score stays suppressed the entire time.Real Example: How a $4,500 Vacation Dropped Sarah's Score 73 Points

Sarah came to us in August 2025 after her credit score dropped from 702 to 629 in two months. She couldn't figure out what happened—she hadn't missed any payments or opened new accounts. Here's what we found: Sarah charged a $4,500 family vacation to Disney in June. Her credit card had a $6,000 limit, so the vacation pushed her to 75% utilization on that card. Her overall utilization jumped from 15% to 42%. When she got home, she had $800 in unexpected expenses (car issue, vet bill). She made minimum payments on her cards but couldn't pay down the Disney balance. Her utilization stayed at 42% for two months. Then in August, she missed a payment on a different credit card by five days while juggling bills. It wasn't reported as late (that requires 30 days), but the combination of high utilization and financial strain pushed her to cut expenses, which meant she closed her oldest credit card to "avoid temptation." Closing that card:- Reduced her total available credit from $18,000 to $12,000

- Pushed her utilization from 42% to 58%

- Reduced her average account age

The Warning Signs You're Headed for Vacation Credit Damage

Most people don't realize they're in trouble until the damage is done. Watch for these red flags:- You're planning to "figure out how to pay for it later" — this is how vacation debt spirals

- You're using credit cards because you don't have the cash — vacation spending should come from savings, not debt

- You're justifying it as "I deserve this" or "I'll work extra to pay it off" — emotional spending decisions create financial problems

- You're putting daily expenses (gas, meals, activities) on credit "just for points" — but you're not paying the balance off immediately

- You opened a new credit card specifically for the trip — and you're planning to max it out

- Your utilization is already above 30% — adding vacation spending will push it even higher

- You're not sure what your credit card balances are right now — if you're not tracking it, you're probably overspending

How to Protect Your Credit Score During Summer Travel

You don't have to skip vacation to protect your credit. You just need to be strategic:Pay Down Balances Before You Travel

If you're going to charge vacation expenses, start with the lowest utilization possible. Pay down your existing credit card balances before your trip. Getting your utilization below 10% before vacation gives you room to spend without triggering penalties.Spread Charges Across Multiple Cards

Instead of putting everything on one card, split expenses across 2-3 cards to keep per-card utilization lower. Just make sure you track every charge and can pay them all off.Pay As You Go

Don't wait until you get home to start paying off vacation charges. Make payments from your hotel room or during the trip. Paying down the balance before your statement closes keeps your reported utilization low. Credit card companies report your balance on your statement closing date, not your payment due date. If you charge $3,000 during vacation but pay $2,500 before your statement closes, only $500 gets reported to the credit bureaus.Use a Vacation Savings Account

The best way to protect your credit during vacation is to pay cash. If you're charging for the rewards points, that's fine—but pay off the charges immediately from savings. Don't carry vacation debt.Avoid Opening New Cards Right Before Travel

If you want a new travel card, open it 3-6 months before your trip, not right before. This gives the hard inquiry time to fade and your credit score time to recover before vacation spending hits.How to Recover If Vacation Already Damaged Your Credit Score

If you already took the vacation and you're looking at credit card debt and a lower credit score, here's your recovery plan:Step 1: Stop Using the Cards

Put the credit cards away. Switch to cash or debit for daily expenses. You can't dig out of debt while you're still adding to it.Step 2: Pay More Than the Minimum

Minimum payments keep you in debt for years. Even an extra $50-100 per month makes a massive difference in how fast you pay it off and how much interest you pay. Use the avalanche method: pay minimums on all cards, then put every extra dollar toward the card with the highest interest rate. Once that's paid off, roll that payment into the next highest rate card.Step 3: Make a Mid-Cycle Payment

Your credit card reports your balance on your statement closing date. Making a payment mid-cycle (before your statement closes) lowers the balance that gets reported to the credit bureaus, which improves your utilization immediately. Example: Your statement closes on the 15th. You have a $4,000 balance. On the 10th, you make a $1,000 payment. Your statement will show $3,000, and that's what gets reported to the credit bureaus. Your credit score improves even though you still owe the money.Step 4: Request a Credit Limit Increase

If you've been a customer in good standing for 6+ months, call your credit card company and request a credit limit increase. If they raise your limit, your utilization drops immediately even if your balance stays the same. Warning: some credit card companies do a hard pull for limit increases. Ask if they'll do a soft pull first. Don't accept a hard inquiry if you're already dealing with recent inquiries.Step 5: Address Any Late Payments Immediately

If you missed a payment, get current immediately. The longer it's late, the more damage it does. If it hasn't hit 30 days yet, it won't be reported to the credit bureaus. If you're at risk of missing a payment, contact the credit card company before the due date and ask for an extension or hardship program. Many issuers will work with you if you're proactive.Step 6: Check Your Credit Report for Errors

Vacation financial stress often coincides with other credit issues. Pull your credit reports from all three bureaus and look for errors, old accounts that should have fallen off, or inaccurate reporting. Disputing errors can give you a quick score boost while you're working to pay down debt. Our guide to credit disputes walks through the process step-by-step.Step 7: Consider Professional Credit Repair

If vacation spending revealed bigger credit issues—collections, charge-offs, late payments, high utilization across multiple cards—professional credit repair can accelerate your recovery. At Crowned Credit, we've helped thousands of clients recover from vacation-related credit damage. We handle the dispute process, negotiate with creditors, and develop a personalized plan to rebuild your credit fast. **Disclaimer:** Crowned Credit provides credit repair services in compliance with the Credit Repair Organizations Act (CROA). While we work to dispute inaccurate, unverifiable, or unfair items on your credit report, we cannot guarantee specific results or score improvements. Individual results vary based on your unique credit situation. We do not guarantee that we can remove all negative items from your credit report or achieve any particular credit score outcome. Any statements about timelines or improvements are estimates based on typical client experiences and not guarantees of your results. Book a free consultation to see how we can help you bounce back from summer spending.What to Do If You're Planning Summer Travel and Already Have Bad Credit

Maybe you're reading this before vacation, and your credit is already in rough shape. Can you still travel without making things worse? Yes, but you need to be extremely careful:- Use debit or cash only — no credit cards at all if your utilization is already high

- Scale down the trip — cheaper accommodations, shorter duration, less spending on activities

- Wait until you've paid down debt — delay the trip a few months while you improve your credit situation

- Use a secured credit card with a small limit — this prevents overspending while still allowing you to build credit