Can the Same Debt Appear Twice on Your Credit Report in 2026?

Ashley Rivera

Credit Repair Specialist

You pull your credit report, scan the negative accounts, and then notice something that makes your stomach drop: the same debt looks like it is showing up twice.

That is not a small detail. If one account turns into what looks like two derogatory entries, it can make your report look worse than it really is. It can also confuse lenders, drag down your scores, and make you feel like you are getting hit twice for the same mistake.

Here is the good news: sometimes it is a real reporting problem, and sometimes it only looks like one. Those are two very different situations. If you treat them the same, you can waste a lot of time disputing the wrong thing.

According to the CFPB, if the same debt is listed multiple times, you should dispute the multiple listings with the credit reporting company and the original creditor or furnisher. They also make the point people miss all the time: a multiple listing is not harmless. It can affect your credit score and the terms lenders offer you.

This guide will show you what duplicate debt reporting actually looks like in 2026, when it is legitimate, when it crosses the line, and exactly what to do if it is hurting your file.

If you want a professional set of eyes on all three reports, you can book a consultation with Crowned Credit or compare plans on our pricing page.

Short answer: can the same debt appear twice?

Yes, but not every “double listing” is an error.

There are really three buckets here:

- Normal and legal reporting: the original creditor reports a charge-off, and a collection agency reports the collection account.

- Questionable or inaccurate reporting: the same debt is being reported twice in a way that makes the balance or status look duplicated.

- Flat-out bad data: two collection agencies, or two nearly identical tradelines, are reporting the same debt at the same time with no good reason.

The hard part is that people often see two entries and assume the answer is obvious. It is not. You have to read the account details before deciding whether you are looking at a lawful charge-off plus collection, or a true duplicate that needs to come off.

When two entries are not automatically an error

This is where a lot of people get tripped up.

Say you had a credit card with a $2,400 balance. You stopped paying. The original creditor eventually charged it off. Later, the account got placed with or sold to a collection agency.

Now your reports may show:

- the original creditor tradeline, showing a charge-off and payment history

- the collection account, showing the debt is now with a collector

That can feel like one debt being reported twice, but in many cases it is standard credit reporting. The original account history does not just disappear because the debt went to collections.

What matters is whether the information is being reported accurately. For example:

- the dates should line up logically

- the original creditor should not keep reporting a balance if it sold the debt and no longer owns it

- the collection account should not create the appearance that you owe two separate debts when there was only one obligation

If you want background on how collection accounts work, read our collections guide and what collections mean on a credit report.

What a real duplicate debt problem looks like

A true duplicate problem usually looks more like one of these:

- Two collection agencies are reporting the same debt at the same time.

- The same collector appears twice with slightly different account numbers or dates.

- The original creditor and collector both show an active balance in a way that makes the debt look doubled.

- The debt was sold, but the previous furnisher never updated its reporting.

- The account was reinserted or re-aged incorrectly after it should have been updated or removed.

That is where the problem stops being cosmetic and starts hurting you in real ways.

Imagine a landlord collection for $1,850. If one collector reports it and then a second collector also reports it without the first one closing out properly, an underwriter may read your file as if you have two separate unpaid rental collections totaling $3,700. That can change a lending decision fast.

And if you are already in the middle of trying to qualify for an apartment, car, or mortgage, the timing gets brutal.

How duplicate debt entries can hurt your credit

The impact depends on the rest of your profile, but duplicate negatives can absolutely make things worse.

- Lower scores: Multiple derogatory entries can signal more risk than actually exists.

- Worse underwriting: Lenders may think your debt load or collection activity is heavier than it really is.

- Higher interest rates: Even if you still get approved, your pricing may get worse.

- Rental denials: Property managers are often quick to reject applicants with collection-heavy reports.

- More cleanup work before closing: Mortgage files get delayed all the time over reporting issues like this.

People sometimes ask, “Can one duplicate really matter that much?” Yes. On a borderline file, one bad reporting issue can be the difference between approval and a denial, or between an okay rate and an ugly one.

CROA Disclosure: No company can legally promise a specific score increase, approval result, or timeline. Credit score impact depends on the full file, the scoring model, lender standards, and whether the information is updated or removed by the bureaus.

How to tell whether you are looking at a legal charge-off plus collection, or a duplicate error

Do not rely on Credit Karma summaries or alert apps alone. Pull the actual reports and compare the details line by line.

Here is what to check:

- Creditor name: Is one the original creditor and the other a collector, or are there two collectors?

- Account status: Does one show charged off while the other shows collection?

- Balance: Is the same balance effectively being counted twice?

- Date of first delinquency: Do the dates support a normal sequence, or does one account look illegally re-aged?

- Ownership notes: Was the debt sold, transferred, or assigned for collection?

- Bureau consistency: Does Equifax show one version while Experian and TransUnion show something else?

One easy rule: if the reporting creates the impression that you owe more than you actually owe, or that you have more derogatory accounts than you actually have, it deserves a closer look.

For a deeper breakdown of tradelines and report sections, read how to read your credit report and our guide to understanding your credit report.

What to do if the same debt is being reported twice

1. Pull all three credit reports

Do not guess from one app. Get all three bureau reports and identify exactly where the duplicate appears. Sometimes it only shows on one bureau. Sometimes the data conflict is different on each one.

2. Gather documents before you dispute

Save anything that helps prove the timeline:

- credit report screenshots or PDFs

- collection letters

- old billing statements

- settlement agreements

- proof the debt was sold or transferred

- proof the balance was already paid or resolved

The stronger your paper trail, the harder it is for a furnisher to brush off the dispute with a lazy verification.

3. Dispute with the bureaus and the furnisher

This is the part many people skip. If the same debt is listed multiple times, dispute it with the credit bureau reporting it and with the creditor or collector furnishing the data.

Be specific. Do not write a vague complaint like, “This account is wrong.” Say what is wrong.

Example:

“This debt is being reported multiple times. The collection account from XYZ Collections duplicates the same underlying debt already reported under ABC Recovery. Please investigate and remove the duplicate or update the reporting so the same debt is not listed more than once.”

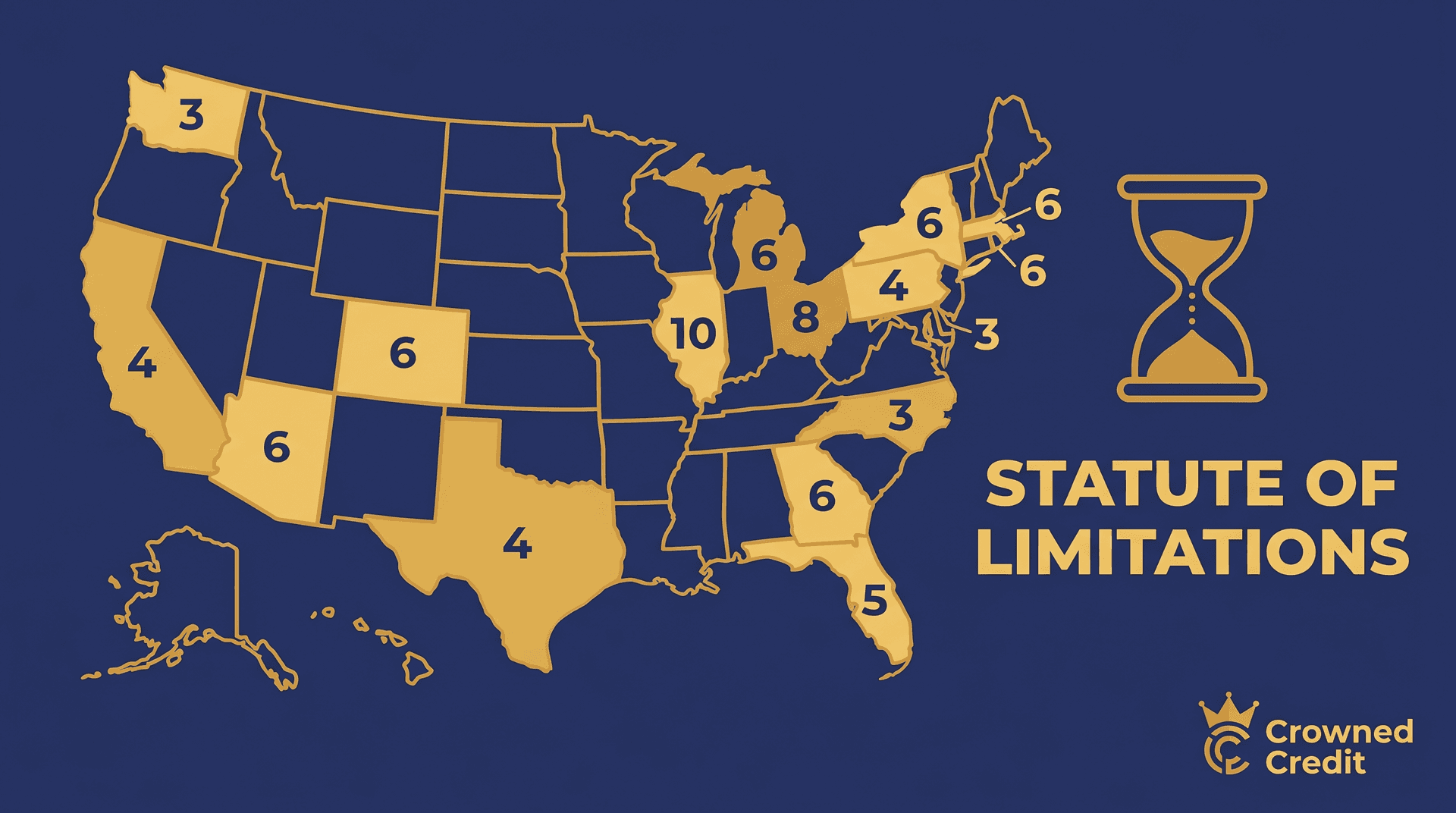

If you need the legal framework first, read your FCRA dispute rights and what the FCRA is.

4. Watch for re-aging issues

Some duplicate-looking accounts are really re-aging problems in disguise. If a debt was moved, sold, or reinserted with a newer delinquency date than it should have, that can illegally extend how long it damages your report.

If you suspect that is happening, read our debt re-aging guide. That issue is serious and worth attacking quickly.

5. Follow up after the investigation window

Under the FCRA, credit bureaus generally have about 30 days to investigate a dispute. When the results come back, do not just look for the word “completed.” Check whether the actual reporting changed.

People get fooled here all the time. They see a dispute closed, assume it is fixed, and never verify the updated tradeline.

What if the debt is accurate, but still looks unfair?

That is a different problem.

If the original creditor charge-off and the collection account are both being reported correctly, the issue may not be “duplicate reporting” in the legal sense. It may just be a rough file that needs a strategy.

In that case, the better questions are:

- Is the collection valid?

- Is the balance accurate?

- Is the date of first delinquency correct?

- Can the collection be challenged as inaccurate, incomplete, outdated, or unverifiable?

- Would resolving other negatives improve the file faster?

That is why you do not want to fire random disputes at everything. A smarter strategy is usually faster than a louder one.

When professional help makes sense

You may be able to handle a simple duplicate listing yourself. But professional help makes more sense when:

- multiple collectors are reporting the same debt

- the balances or dates do not make sense

- the account keeps coming back after prior disputes

- you are close to applying for a mortgage, apartment, or auto loan

- your file has other negatives layered on top of the duplicate issue

Crowned Credit helps clients challenge inaccurate, incomplete, outdated, and unverifiable negative items across all three bureaus while building a plan for the full report, not just one account in isolation.

If you want help, book now or call 336-310-0090.

Current pricing:

- Essential: $150 setup + $99/month

- Accelerated: $249 setup + $199/month

- Momentum: $1,095 one-time

The bottom line

Yes, the same debt can appear twice on your credit report, but that does not automatically mean the reporting is illegal. Sometimes it is a normal charge-off plus collection sequence. Sometimes it is a real duplicate that needs to be disputed.

The difference comes down to the details: who is reporting, what balance is showing, whether the timeline makes sense, and whether the reporting makes your debt look larger or more active than it really is.

If you are seeing duplicate debt entries, do not ignore them and do not assume the bureaus will clean it up on their own. Pull all three reports, document the problem, dispute it precisely, and verify the result.

If you want help sorting out whether you are looking at a legal collection sequence or a credit report error, Crowned Credit can review the file with you and help map the next move. Start on the pricing page, read more at our credit report errors guide, or book a consultation.

Disclaimer: Results vary based on each person’s credit profile, reporting history, and lender standards. Credit score impacts and timelines are never guaranteed. This content is for educational purposes only and should not be considered legal or financial advice. Crowned Credit assists clients in disputing inaccurate, incomplete, outdated, or unverifiable information on credit reports in accordance with the Fair Credit Reporting Act (FCRA) and the Credit Repair Organizations Act (CROA).