How to Read Your Credit Report Like a Pro (2026 Guide)

Ashley Rivera

Credit Repair Specialist

Your credit report is one of the most powerful documents in your financial life — yet most people have never read one carefully. If you’ve ever been denied a loan, a rental, or even a job, your credit report may hold the answer. Learning how to read your credit report isn’t just for finance nerds.

It’s a skill every adult needs.

This 2026 guide walks you through every section of your credit report, shows you what lenders actually look for, and teaches you how to spot errors that could be costing you thousands of dollars in higher interest rates.

Step 1: Get Your Free Credit Report

Federal law entitles you to one free credit report per year from each of the three major credit bureaus — Equifax, Experian, and TransUnion. The official (and only government-authorized) source is AnnualCreditReport.com. Avoid third-party sites that advertise “free” reports but require a credit card.

Here’s a smart strategy: since there are three bureaus, pull one report every four months. That way, you’re monitoring your credit year-round without spending a dime. Set a calendar reminder for January (Equifax), May (Experian), and September (TransUnion).

You can also access your reports weekly for free through AnnualCreditReport.com — a provision that became permanent after the COVID-19 pandemic. Take advantage of it.

Step 2: Understanding Your Credit Report — Section by Section

Once you pull your report, don’t be intimidated by the pages of data. Every credit report follows the same basic structure. Here’s what you’ll find and what it means.

Personal Information

This section includes your name (including variations or maiden names), current and past addresses, Social Security number (partially masked), date of birth, and employment history.

What to check: Make sure everything is accurate. Incorrect names or addresses can be signs of identity theft or mixed files (where another person’s data gets merged with yours). This is more common than people think, especially if you have a common name.

Credit Accounts (Trade Lines)

This is the heart of your credit report. Each account — credit cards, mortgages, auto loans, student loans, personal loans — appears here as a “trade line.” For each account, you’ll see:

- Creditor name and account number (partially masked)

- Account type (revolving, installment, mortgage)

- Date opened

- Credit limit or loan amount

- Current balance

- Payment history — typically shown as a month-by-month grid (30, 60, 90+ days late)

- Account status (open, closed, in collections, charged off)

What to check: Scan for accounts you don’t recognize — that’s a red flag for fraud. Check that balances and credit limits are accurate. Most importantly, verify your payment history. Even one 30-day late payment can drop your score significantly.

Want to go deeper? Read our full guide on understanding your credit report.

Public Records

Public records on a credit report historically included bankruptcies, civil judgments, and tax liens. As of 2018, the major bureaus removed most civil judgments and tax liens. Today, bankruptcies are the primary public record that appears on credit reports.

A Chapter 7 bankruptcy can stay on your report for up to 10 years. A Chapter 13 stays for 7 years. These are serious derogatory marks that significantly impact lending decisions.

Inquiries

Inquiries are records of who has accessed your credit report. There are two types:

- Hard inquiries: Generated when you apply for credit. These can slightly lower your score and stay on your report for 2 years (though they only affect your score for 12 months).

- Soft inquiries: Generated when you check your own credit, or when companies pre-screen you for offers. These do NOT affect your score.

What to check: Look for hard inquiries you don’t recognize. An unauthorized hard pull could indicate identity theft or a creditor error. You have the right to dispute unauthorized inquiries.

Step 3: How to Spot Errors on Your Credit Report

A Federal Trade Commission study found that 1 in 5 Americans has an error on at least one credit report. Many of these errors are significant enough to affect lending decisions. Here’s what to look for:

Common Credit Report Errors

- Accounts that aren’t yours — could be identity theft or a mixed file

- Incorrect payment status — being shown as late when you paid on time

- Wrong account balances or credit limits — affects your credit utilization ratio

- Duplicate accounts — same debt listed twice, especially after debt sales

- Outdated negative items — most negative items should fall off after 7 years; check that old collections or charge-offs aren’t lingering past their reporting window

- Incorrect personal information — wrong address, misspelled name, wrong SSN

- Accounts closed by you, reported as closed by creditor — minor, but worth correcting

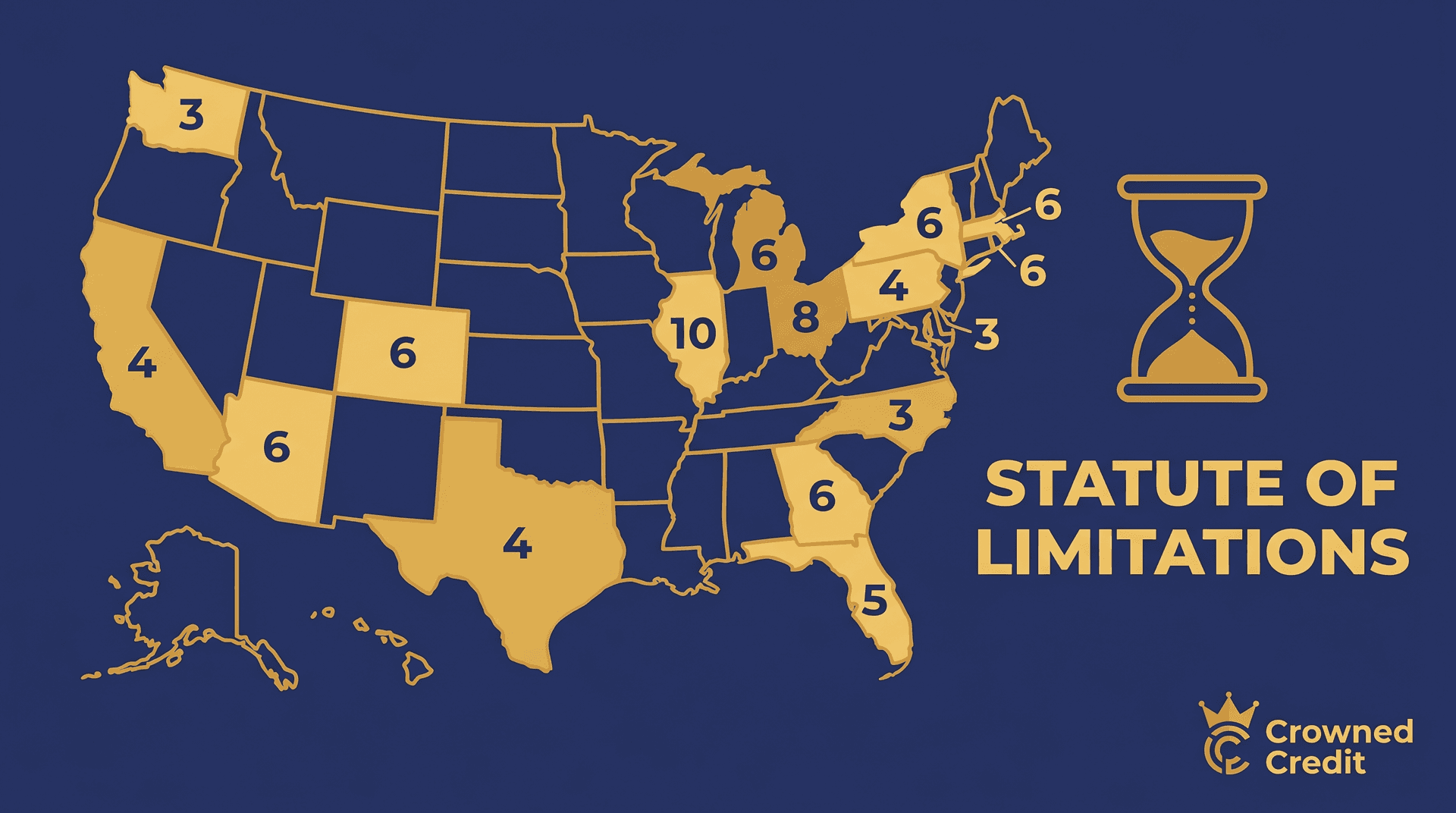

The 7-Year Reporting Rule

Under the Fair Credit Reporting Act (FCRA), most negative items — late payments, collections, charge-offs — can only stay on your credit report for 7 years from the date of first delinquency. Bankruptcies are the main exception (10 years for Chapter 7). If you see items past their legal reporting window, that’s an error you can and should dispute.

Step 4: What to Dispute and How

Found something wrong? You have the legal right to dispute it. Here’s the process:

Option 1: Dispute Directly with the Bureau

Each of the three bureaus has an online dispute portal:

- Equifax: equifax.com/personal/credit-report-services/credit-dispute/

- Experian: experian.com/disputes

- TransUnion: dispute.transunion.com

Once you file a dispute, the bureau has 30 days to investigate (45 days if you provide additional information). They must contact the creditor who reported the item. If the creditor can’t verify the information, it must be removed.

Option 2: Dispute Directly with the Creditor

You can also dispute errors directly with the company that furnished the information. Send a certified letter with documentation explaining the error. The furnisher has 30 days to investigate and report corrections to the bureaus.

What You Need for a Strong Dispute

- A clear, specific explanation of what’s wrong and why

- Supporting documentation (bank statements, payment confirmations, correspondence)

- Copies of your ID and proof of address

Vague disputes like “this isn’t mine” without supporting context are often rejected. Be specific.

Step 5: Know When to Get Professional Help

DIY disputing works for straightforward errors — wrong address, duplicate account, a payment misreported. But if you’re dealing with multiple negative items, complex errors, or simply don’t have the time to manage the process, professional credit repair can be worth considering.

At Crowned Credit, we specialize in identifying and disputing inaccurate, unverifiable, and outdated items on your behalf. Our team knows the FCRA inside and out, and we track every dispute to make sure nothing falls through the cracks.

We offer three plans to fit your situation:

- Basic Plan — $150 setup + $99/month: Great for clients with a handful of items to address

- Standard Plan — $249 setup + $149/month: Our most popular plan, covers all three bureaus with comprehensive disputing

- Premium Plan — $249 setup + $199/month: Full-service with priority support and advanced strategies

Disclaimer: Results vary based on individual credit history. We cannot guarantee specific outcomes or timelines, as credit reporting is governed by federal law and creditor cooperation.

Ready to see what’s possible? View our full pricing plans or book a free consultation today.

Final Checklist: How to Read Your Credit Report

- ✅ Pull all three reports from AnnualCreditReport.com

- ✅ Verify your personal information is accurate

- ✅ Review every trade line — check status, balance, payment history

- ✅ Look for accounts you don’t recognize

- ✅ Check for outdated negative items (past 7-year window)

- ✅ Review hard inquiries for anything unauthorized

- ✅ Document any errors with supporting evidence

- ✅ File disputes with the bureau, creditor, or both

- ✅ Follow up — bureaus have 30 days to respond

Understanding your credit report is the foundation of credit health. Once you know how to read it, you’re in control. And if what you find is overwhelming, you don’t have to tackle it alone.

👉 Learn more about understanding your credit report or book a consultation with our credit specialists.

Disclaimer: Results vary by individual. Credit repair timelines depend on your unique credit history and the nature of the items being disputed. Crowned Credit cannot guarantee specific results or timeframes.