Debt-to-Income Ratio: How to Calculate Yours and Why Lenders Care So Much

Ashley Rivera

Credit Repair Specialist

You check your credit score religiously. You've paid down a couple of collections. Your score finally cracked 680. Then you apply for a mortgage — and get denied.

The reason? Your debt-to-income ratio (DTI) was too high.

Most people obsess over their credit score and completely ignore DTI. That's a mistake. Lenders use your debt-to-income ratio as a core approval factor for mortgages, auto loans, personal loans, and credit cards. A strong credit score with a bloated DTI will still get you rejected — or stuck with a worse interest rate than you deserve.

Here's everything you need to know about DTI: how to calculate it, what lenders actually want to see, and exactly how to bring yours down.

What Is Debt-to-Income Ratio?

Your debt-to-income ratio is the percentage of your gross monthly income that goes toward paying debts. It tells lenders one simple thing: how much of your paycheck is already spoken for?

The formula is straightforward:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

If you earn $5,000 per month before taxes and your total monthly debt payments add up to $1,800, your DTI is 36%.

That number matters more than you think. When a lender pulls your application, they're looking at two things side by side: your credit score (can this person manage credit responsibly?) and your DTI (can this person actually afford another payment?). You need both to be solid.

Front-End vs. Back-End DTI: Lenders Look at Both

There are actually two versions of DTI that lenders calculate:

Front-end DTI (also called the housing ratio) only includes housing costs — your mortgage payment or rent, property taxes, homeowner's insurance, and HOA fees if applicable. Most lenders want this under 28%.

Back-end DTI includes housing costs plus every other recurring debt payment: car loans, student loans, credit card minimum payments, personal loans, child support, and alimony. This is the number lenders focus on most, and it's the one that trips people up.

When someone says "your DTI," they usually mean back-end DTI. That's the number we'll focus on here.

How to Calculate Your DTI Right Now

Grab your most recent pay stub and your monthly statements. Then add up every recurring debt payment:

- Mortgage or rent payment (including escrow for taxes and insurance)

- Car loan payment

- Student loan payment (use the amount on your credit report, even if you're on an income-driven plan showing $0 — some lenders calculate 0.5-1% of the balance)

- Credit card minimum payments (the minimum due on each statement, not what you actually pay)

- Personal loan payments

- Child support or alimony

- Any other debt that shows on your credit report

Now divide that total by your gross monthly income (before taxes, before deductions — your total earnings).

Real example: Marcus earns $6,200/month gross. His monthly debts look like this:

- Rent: $1,400

- Car payment: $485

- Student loans: $320

- Credit card minimums (3 cards): $210

- Personal loan: $175

Total monthly debt: $2,590

DTI: $2,590 ÷ $6,200 = 41.8%

Marcus has a decent credit score of 695, but that 41.8% DTI is going to make getting a conventional mortgage tough. Most conventional lenders cap DTI at 43-45%, and Marcus is already close to the ceiling before adding a mortgage payment.

What DTI Do Lenders Actually Want?

Different loan types have different DTI limits, but here's the general breakdown for 2026:

- Conventional mortgages: Most lenders want 43% or less. Some will go up to 45% or even 50% with strong compensating factors (high credit score, large down payment, significant cash reserves).

- FHA loans: Officially up to 43%, but many FHA lenders approve up to 50% with a credit score of 580+ and compensating factors.

- VA loans: No hard DTI cap, but most lenders prefer 41% or below. The VA uses a residual income test instead, which measures how much money you have left after all debts and living expenses.

- USDA loans: Generally capped at 41% back-end DTI.

- Auto loans: Vary widely by lender, but most prefer under 50%. Subprime auto lenders may go higher.

- Credit cards: No published DTI requirement, but issuers absolutely factor your reported income and existing debts into approval decisions.

- Personal loans: Most lenders prefer 35-40% or below.

Here's the reality: lower is always better. A DTI of 20% tells a lender you have breathing room. A DTI of 48% tells them you're stretched thin and one unexpected expense away from missing payments.

DTI and Your Credit Score: How They Work Together

Your DTI ratio doesn't appear on your credit report and doesn't directly affect your credit score. FICO and VantageScore don't use DTI in their calculations.

But here's where it gets interesting: the factors that cause a high DTI often overlap with factors that hurt your credit score.

High credit card balances? That inflates your DTI through minimum payments and wrecks your credit utilization ratio. Multiple loan payments? More chances for a late payment to show up on your report.

The two metrics are separate but connected. Fixing one often improves the other. That's why a full credit strategy — not just score chasing — matters so much when you're preparing for a major purchase like a home or car.

7 Ways to Lower Your Debt-to-Income Ratio

If your DTI is above 40%, you've got work to do before applying for new credit. Here are the most effective strategies, ranked by impact:

1. Pay Off Small Debts Completely

This is the fastest way to move the needle. That $75/month personal loan with $600 left? Pay it off. The credit card with a $180 minimum and $2,100 balance? Knock it out if you can.

Every debt you eliminate removes its full monthly payment from your DTI calculation. Paying off a $300/month car loan drops your DTI by nearly 5 percentage points if you earn $6,000/month. That alone could be the difference between approval and denial.

2. Stop Taking on New Debt

Sounds obvious, but it's the most common mistake people make when preparing for a mortgage. Financing new furniture, opening a store credit card for the 15% discount, co-signing someone's loan — all of these add monthly obligations that inflate your DTI right when you need it low.

Rule of thumb: freeze all new borrowing at least 6 months before applying for a mortgage.

3. Attack High-Payment Debts First

DTI cares about monthly payment size, not total balance. A $15,000 student loan with a $150/month payment hurts your DTI less than a $5,000 credit card balance with a $250/month minimum.

Look at your debts and ask: which ones have the highest monthly payment relative to their remaining balance? Those are your priority targets. This is basically the debt avalanche method optimized for DTI reduction.

4. Increase Your Income

Since DTI is a ratio, you can improve it from the income side too. A raise, a side gig, or overtime hours all count. If you're self-employed or have variable income, lenders typically average your last 24 months of tax returns.

Even a $500/month increase in gross income can drop your DTI by 2-3 percentage points when your debts are in the $2,000-$3,000/month range.

5. Refinance to Lower Monthly Payments

If you have a car loan at 11% interest, refinancing to 7% could drop your monthly payment by $80-$120. That directly reduces your DTI. Same with student loans — consolidating or refinancing into a lower payment can help, though be careful about losing federal loan protections.

6. Request Credit Card Limit Increases (Without Spending More)

This one is sneaky. Higher credit limits don't change your minimum payment, but they lower your credit utilization ratio, which can improve your credit score. A better score gives you access to refinancing options that reduce monthly payments, which lowers DTI.

It's an indirect play, but effective over 3-6 months.

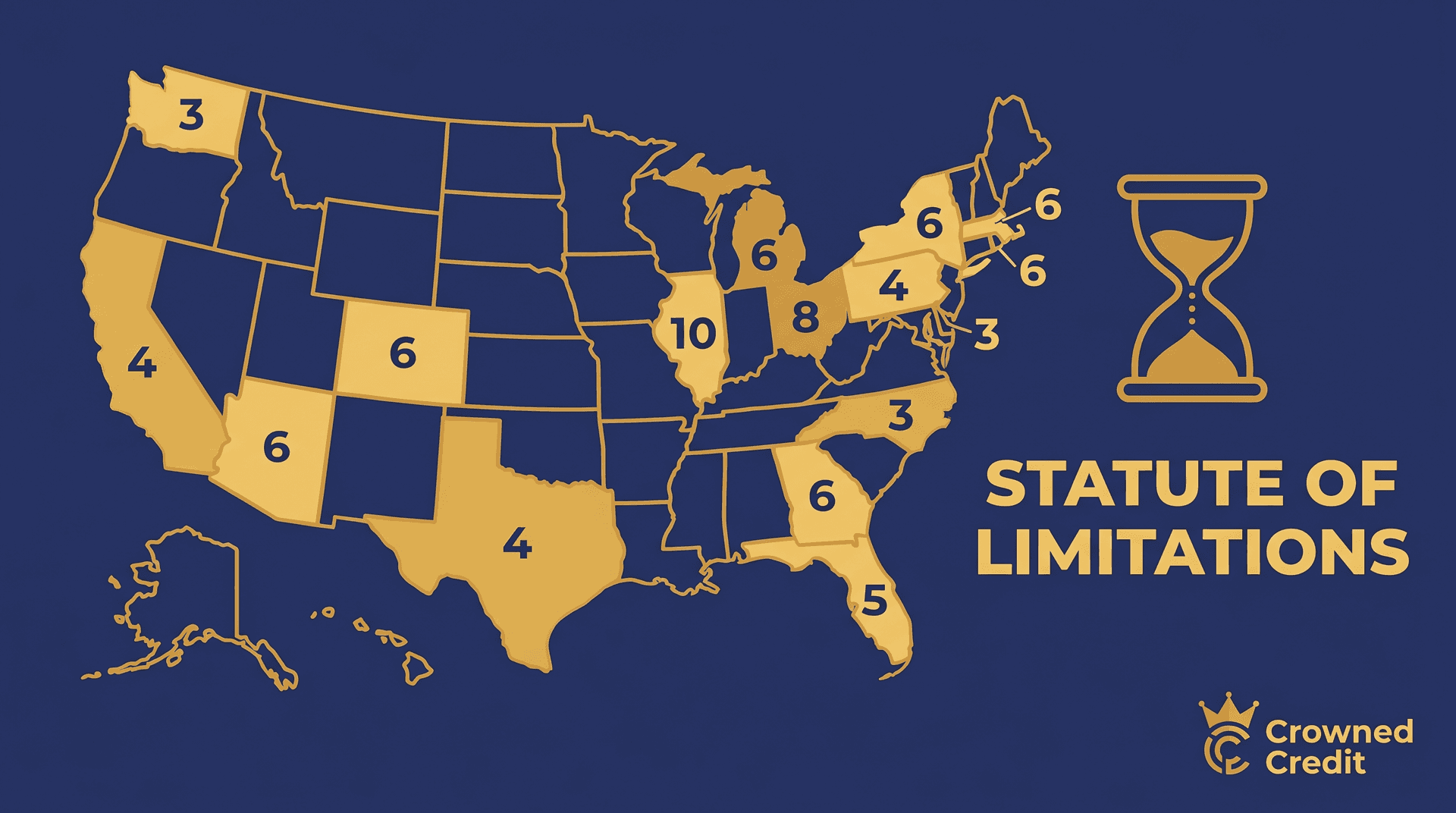

7. Get Errors Removed From Your Credit Report

Sometimes debts on your credit report aren't even yours. Duplicate accounts, debts past the statute of limitations, accounts from identity theft, or collections that were already paid — all of these can inflate your reported debt obligations.

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any item on your credit report. Creditors and bureaus must verify the accuracy and completeness of what they report. If they can't, the item must be removed.

This is exactly the kind of work a professional credit repair company handles. At Crowned Credit, we review your full credit profile, identify items that are unverifiable, inaccurate, or outdated, and dispute them strategically with all three bureaus. Removing even one collection or charge-off can eliminate a monthly payment from your DTI calculation entirely.

What Doesn't Count in DTI (Common Misconceptions)

People frequently overcount their DTI by including expenses that lenders don't factor in:

- Utilities (electric, water, gas, internet) — not included

- Groceries and food — not included

- Health insurance premiums — not included (unless deducted pre-tax from gross income)

- Car insurance — not included

- Cell phone bills — not included

- Subscriptions (Netflix, gym, etc.) — not included

- Income taxes — not included (DTI uses gross income)

Only debts that show up on your credit report (or are disclosed on a loan application, like child support) count toward DTI. Your monthly spending on living expenses is separate.

DTI When You're Self-Employed: It Gets Complicated

If you're a W-2 employee, DTI calculation is simple — your pay stubs show your gross income clearly. Self-employed borrowers have it harder.

Lenders use your net income from tax returns (after business deductions), averaged over the last two years. That means all those deductions that save you money on taxes? They also make your income look lower to a lender, which inflates your DTI.

A self-employed borrower who grosses $150,000 but reports $85,000 after deductions will have their DTI calculated on the $85,000. If their monthly debts are $2,800, their DTI is 39.5% — which looks much worse than it would if the lender used gross revenue.

If you're self-employed and planning to buy a home, talk to a mortgage broker 12-18 months ahead. You may need to adjust your tax strategy to show higher qualifying income.

The Real-World Impact: What High DTI Costs You

Let's put real numbers on this. Say you're buying a $300,000 home with 5% down, so you're financing $285,000 on a 30-year fixed mortgage.

- With a DTI of 30% and a 720 credit score: You might qualify for a 6.5% rate → $1,801/month payment → $363,360 in total interest over the life of the loan.

- With a DTI of 47% and a 720 credit score: You might only qualify for a 7.25% rate (higher risk tier) → $1,944/month payment → $414,840 in total interest.

That's a $143/month difference — $51,480 more over 30 years — just because of a higher DTI. Same credit score. Same house. Different ratio.

And that's assuming you get approved at all. Many lenders would simply decline the 47% DTI application.

How to Prepare Your DTI Before a Major Application

If you're 6-12 months out from applying for a mortgage or major loan, here's a practical timeline:

Month 1-2: Pull your credit reports from all three bureaus at AnnualCreditReport.com. Calculate your current DTI. Identify which debts can be paid off or reduced fastest. If you spot errors, inaccuracies, or unverifiable items on your report, start the dispute process.

Month 3-4: Aggressively pay down small-balance debts. Avoid opening any new credit. If you have collections or charge-offs that shouldn't be there, this is where professional help pays off — working with a credit repair team can speed up the dispute process significantly.

Month 5-6: Recalculate your DTI. Get pre-qualified (not pre-approved — pre-qualification is a soft pull that won't affect your score). See where you stand and what loan amounts you qualify for.

Month 7-12: Fine-tune. If your DTI is still high, focus on increasing income or paying down the highest-payment debts. Don't make any major financial moves — no job changes, no large purchases, no co-signing.

When High DTI Is Actually a Credit Report Problem

Here's something most financial advice sites won't tell you: a significant chunk of high-DTI cases are actually credit report accuracy problems.

Duplicate collections for the same debt (reported by both the original creditor and the collector), accounts that should have fallen off after 7 years, debts from identity theft, and incorrect balance reporting all inflate the debt side of your ratio artificially.

The Federal Trade Commission found that 1 in 4 consumers has an error on their credit report that could affect their score. Some of those errors also create phantom debt payments that inflate DTI.

If you've calculated your DTI and it seems higher than your actual monthly obligations, pull your full credit reports and compare line by line. You might find debts listed that you don't owe, have already paid, or that belong to someone else.

Under the FCRA, you have every right to dispute these items. The bureaus — Equifax, Experian, and TransUnion — must investigate and correct or remove unverifiable information within 30 days.

Get Your Full Credit Picture Before You Apply

Your DTI and your credit score tell different parts of the same story. Lenders look at both. A strong score with a clean report and a healthy DTI is the combination that unlocks the best rates and the fastest approvals.

If your credit report has items dragging you down — whether that's inaccurate collections, outdated charge-offs, or errors you didn't put there — cleaning those up can improve both your score and your DTI at the same time.

That's exactly what we do at Crowned Credit. We don't just look at your score — we analyze your full credit profile, identify disputable items under FCRA, and work to get them removed or corrected. Our Accelerated plan ($249 enrollment + $199/month) is built for people who are preparing for a major purchase and need their credit cleaned up on a timeline.

Ready to see what's on your report and what can be done about it? Book a free consultation or call us at 336-310-0090.

Disclaimer: Credit repair results vary by individual. No company can guarantee specific score increases or the removal of accurate, verifiable information. Crowned Credit works within your rights under the Fair Credit Reporting Act to dispute inaccurate, unverifiable, and outdated items on your behalf.