Do Tax Liens Show Up on Your Credit Report in 2026? (The Truth)

Ashley Rivera

Credit Repair Specialist

If you owe back taxes and you're worried about your credit score tanking, I have good news: tax liens no longer appear on your credit reports.

In April 2018, the three major credit bureaus — Experian, TransUnion, and Equifax — removed all tax lien records from consumer credit files as part of a settlement with state attorneys general. That includes paid liens, unpaid liens, federal liens, and state liens. Gone.

But before you breathe too easy, understand this: just because a tax lien isn't hurting your credit score doesn't mean it's not hurting you. Lenders can still see it. The IRS can still take your assets. And if you're trying to buy a house or refinance a loan, that lien will show up when it counts.

Here's everything you need to know about tax liens, credit reports, and what actually happens in 2026 when you owe the government money.

Why Tax Liens Were Removed from Credit Reports

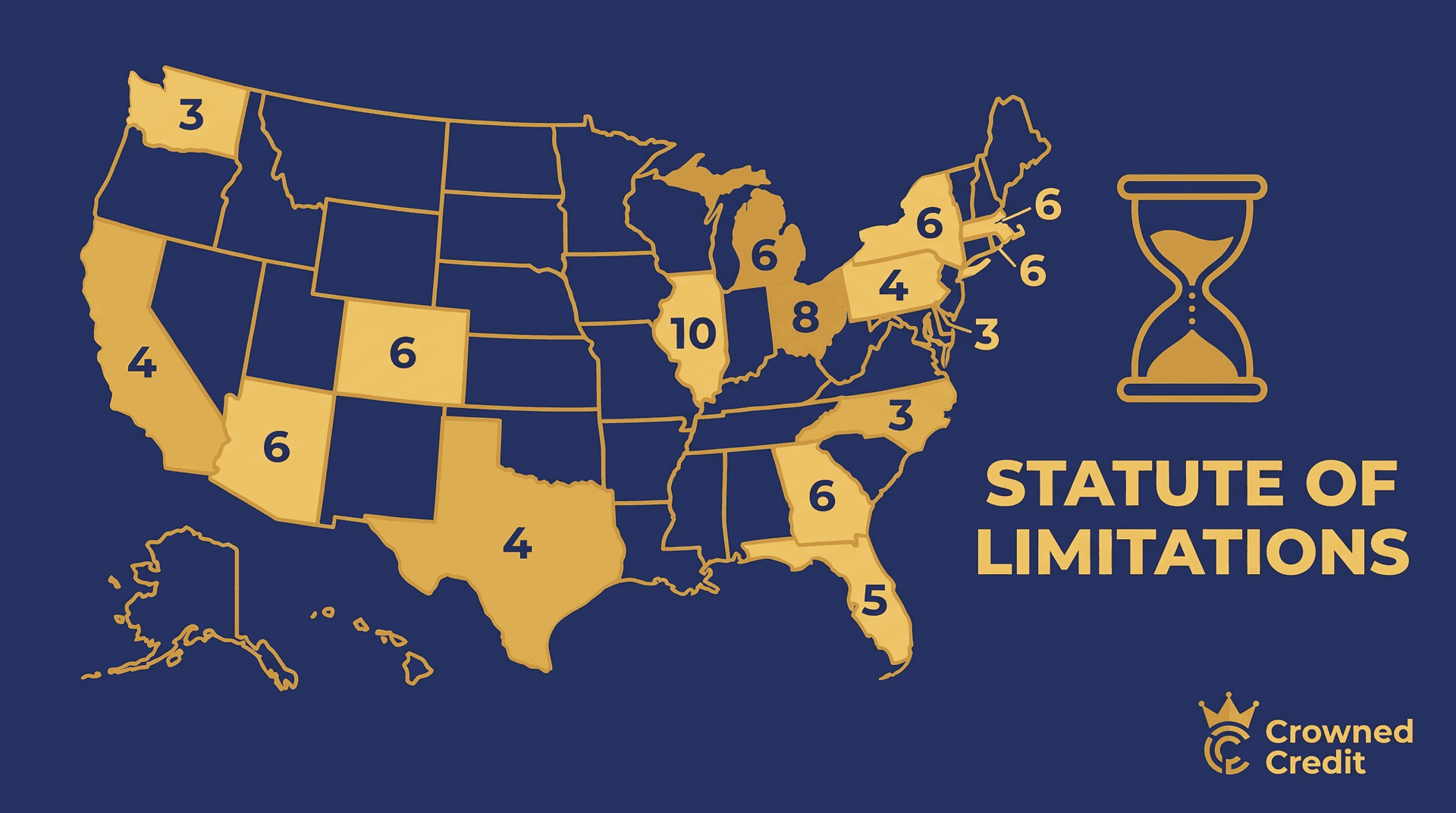

Tax liens used to be one of the most damaging items on a credit report. A single unpaid lien could drop your score by 100+ points and stay on your report for up to 15 years if unpaid, or 7 years after being satisfied.

The problem? The data was often wrong.

A 2011 Federal Trade Commission study found that 26% of consumers had errors on their credit reports. Public records like tax liens were particularly prone to mistakes — wrong names, wrong amounts, liens that had been paid but still showed as open, or liens that belonged to someone else entirely.

In 2015, the National Consumer Assistance Plan (NCAP) set new standards for reporting public records on credit reports. By 2018, the credit bureaus decided it was easier to stop reporting tax liens altogether than to verify them accurately.

So they disappeared. Overnight, millions of consumers saw their credit scores improve — some by 20-40 points — just from the removal of old tax lien records.

What Still Happens When You Have a Tax Lien

Here's what people get wrong: a tax lien not showing up on your credit report doesn't mean it doesn't exist. The lien is still a matter of public record. It's still filed with your county clerk or secretary of state. And it still gives the IRS or state tax authority a legal claim to your property.

Here's what still happens:

- It shows up in public records searches. Mortgage lenders, title companies, and some credit card issuers run separate public records checks that aren't part of your credit report. They'll see the lien.

- The IRS can seize your assets. A federal tax lien gives the IRS the right to take your bank accounts, wages, real estate, vehicles — basically anything you own.

- It blocks refinancing and home purchases. You can't get a clear title if there's a lien on your property. Most mortgage lenders won't approve you until the lien is satisfied or withdrawn.

- It stays on public record for 10+ years. Even after you pay it off, the lien filing remains in public records unless you request a withdrawal.

- It can trigger denials from other lenders. Some banks and credit unions check public records for liens and judgments as part of their underwriting process, even if those items don't appear on your credit report.

Bottom line: your credit score might be fine, but your ability to borrow money is not.

How to Check if You Have a Tax Lien

Since liens no longer show up on credit reports, you can't rely on your Experian or Credit Karma report to tell you if you have one. Here's how to check:

For Federal Tax Liens (IRS):

- Call the IRS Centralized Lien Unit at 800-913-6050

- Request a lien payoff amount or check lien status

- Check your IRS online account at irs.gov

For State Tax Liens:

- Contact your state's department of revenue or taxation

- Search your county clerk's office public records (often available online)

- Use a public records search service (though these may charge fees)

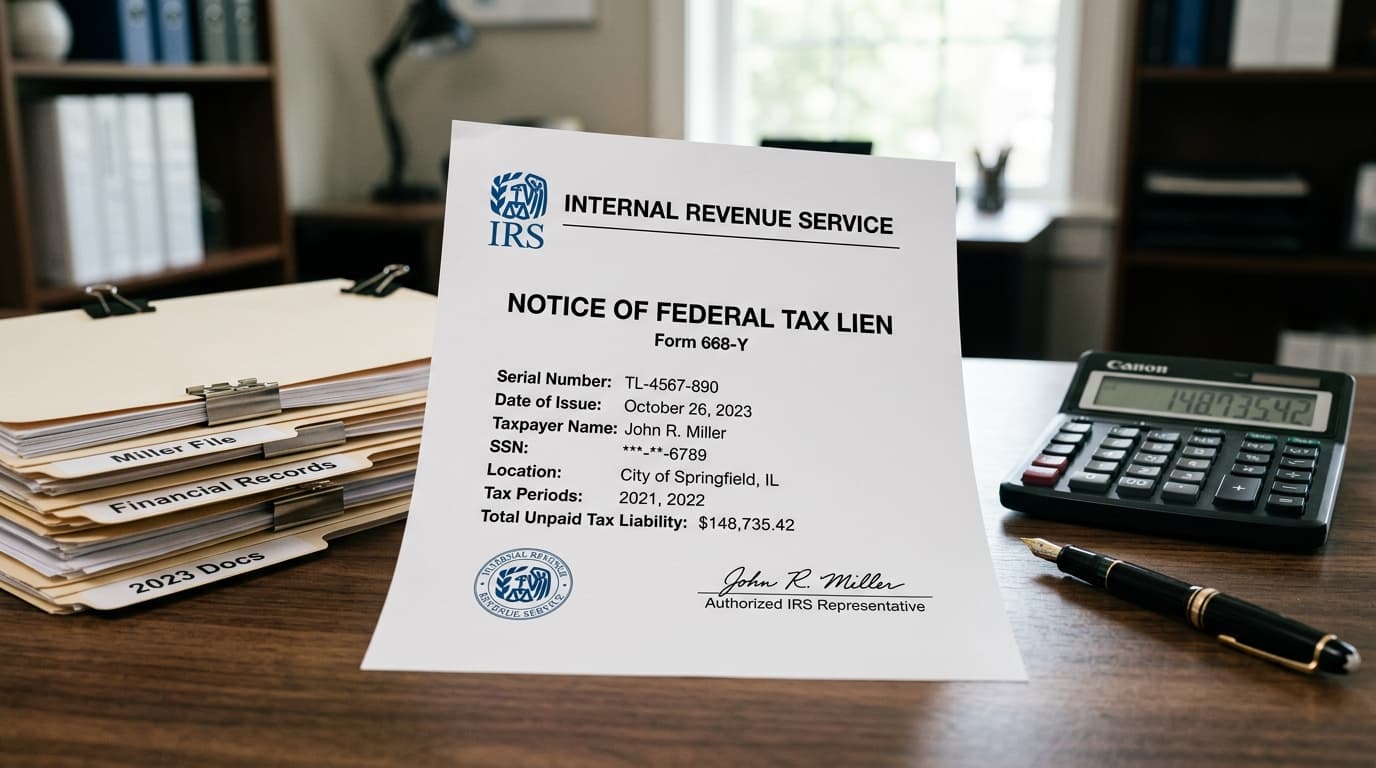

If you've received a "Notice of Federal Tax Lien" from the IRS, you definitely have one. The IRS only files a lien after you've ignored multiple notices about unpaid taxes.

How to Remove a Tax Lien (The Right Way)

Since liens don't appear on your credit report anymore, "removing" one isn't about disputing it with the credit bureaus. It's about getting the government to release or withdraw the lien from public records.

Here are your options:

1. Pay in Full and Request a Release

The simplest path. Pay your tax debt in full, and the IRS or state agency is required by law to release the lien within 30 days. The lien filing stays in public records but is marked "satisfied" or "released," which is much better than "active."

To speed this up, you can request a Certificate of Release of Federal Tax Lien (IRS Form 668(Z)).

2. Request a Withdrawal After Payment

This is better than a release. A withdrawal removes the public record of the lien entirely, as if it never existed. To qualify, you must:

- Pay your tax debt in full

- Be in compliance with all filing and payment requirements

- File IRS Form 12277 (Application for Withdrawal of Filed Form 668(Y))

The IRS reviews withdrawal requests on a case-by-case basis. They're more likely to approve if you've been cooperative, filed all your returns, and set up future withholding to avoid more tax debt.

3. Set Up a Direct Debit Installment Agreement

If you can't pay in full, the IRS offers a lien withdrawal for taxpayers who set up a direct debit installment agreement and meet certain criteria. You'll need to:

- Owe $25,000 or less in combined tax, penalties, and interest

- Set up automatic monthly payments via direct debit

- Make three consecutive on-time payments

- File Form 12277 to request withdrawal

This option gives you breathing room while still getting the lien off public records.

4. Apply for Discharge of Property

If you need to sell a specific piece of property (like a house) and there's a lien on it, you can request a discharge. This removes the lien from that one property, often in exchange for paying the IRS part of the sale proceeds.

Use IRS Form 14135 (Application for Certificate of Discharge of Property from Federal Tax Lien).

5. Offer in Compromise (OIC)

If you genuinely can't pay your tax debt and probably never will, you can apply to settle for less than you owe. This is called an Offer in Compromise. The IRS accepts about 25,000 OICs per year out of millions of delinquent taxpayers, so it's not easy — but it's worth trying if you're in real financial hardship.

If your OIC is accepted and you fulfill the terms, the lien is released.

What If the Lien Is Wrong?

Mistakes happen. You might have a lien filed against you that:

- Belongs to someone else with a similar name

- Was already paid but not released

- Lists the wrong amount

- Is for a tax year you never owed

If the lien is incorrect, you need to contact the IRS or state tax authority directly — not the credit bureaus, since the lien isn't on your credit report anyway. Provide documentation showing the error (payment receipts, tax transcripts, identity verification, etc.) and request that the lien be released or corrected.

For federal liens, call the IRS at 800-913-6050. For state liens, contact your state's department of revenue.

Do Tax Liens Hurt Your Credit Score?

Not directly. Since liens aren't on your credit report, they can't impact your FICO or VantageScore.

But here's the catch: if you have a tax lien, you probably also have other credit problems. Unpaid taxes often go hand-in-hand with unpaid credit cards, medical bills, or other debts. Those will hurt your score.

Also, if the IRS levies your bank account or garnishes your wages to collect on the lien, that can cause missed payments on other obligations — and those show up on your credit report.

Can a Credit Repair Company Remove a Tax Lien?

Here's the truth: a legitimate credit repair company can't remove a tax lien from public records. Only the IRS or state tax authority can do that, and only if you meet specific criteria (usually paying the debt or qualifying for withdrawal).

What a credit repair company can do:

- Help you dispute inaccurate information on your credit report (though liens aren't on there anymore anyway)

- Guide you through the IRS lien withdrawal process

- Negotiate with creditors to remove other negative items that are dragging down your score

- Advise on rebuilding your credit after resolving tax debt

If you're dealing with both tax debt and credit issues, the best approach is to work with a tax professional (like an enrolled agent or tax attorney) on the lien itself, and a credit repair service on everything else.

At Crowned Credit, we focus on removing inaccurate negative items from your credit report — things like collections, charge-offs, late payments, and inquiries. We don't handle tax debt directly, but we can help clean up your credit report while you're working on resolving IRS issues. Book a free consultation to see if we can help.

Tax Liens vs. Tax Levies: What's the Difference?

A lot of people confuse these two terms. Here's the difference:

- Tax lien: A legal claim against your property. It's passive — it doesn't take your money, but it blocks you from selling or refinancing assets until you pay.

- Tax levy: The actual seizure of your property to satisfy the debt. The IRS takes money from your bank account, garnishes your paycheck, or even seizes your car or house.

A lien comes first. If you ignore it, the IRS escalates to a levy. Both are bad, but a levy is worse because it means you're actively losing money or property.

How Long Does a Tax Lien Last?

Federal tax liens last for 10 years from the date the tax is assessed, unless you pay it off or the IRS extends the collection period (which they can do if you file for bankruptcy, request an installment agreement, or submit an Offer in Compromise).

State tax liens vary by state but typically last 10-20 years.

Even after the lien expires, the public record of the lien filing can remain indefinitely unless you request a withdrawal.

What to Do If You Owe Back Taxes

If you owe back taxes and you're worried about a lien being filed (or one has already been filed), here's what to do:

- Don't ignore IRS notices. The longer you wait, the more penalties and interest you rack up — and the closer you get to a lien or levy.

- Check if a lien has been filed. Call the IRS at 800-913-6050 or search your county clerk's public records.

- Set up a payment plan. The IRS offers installment agreements for taxpayers who can't pay in full. If you owe less than $50,000, you can set one up online at irs.gov without talking to anyone.

- Request a lien withdrawal if you're eligible. If you've paid your debt or set up a direct debit installment agreement, file Form 12277.

- Work on your credit separately. While the lien itself won't hurt your credit score, other debts and missed payments will. Focus on paying down collections, catching up on late accounts, and disputing errors.

The worst thing you can do is nothing. The IRS has more collection power than any other creditor — they can take your money without a lawsuit. Deal with it as early as possible.

Final Thoughts

Tax liens no longer show up on credit reports, which is great news for millions of Americans who owe back taxes. Your credit score won't take a hit just because you have a lien filed against you.

But that doesn't mean the problem goes away. Lenders still check public records. The IRS can still seize your assets. And if you want to buy a house, refinance, or get approved for certain loans, that lien will block you.

The good news? Tax liens are fixable. Pay your debt, request a withdrawal, or negotiate a settlement — and you can move on. And while you're at it, clean up the rest of your credit report so you're in the best possible position when you need to borrow.

If you're dealing with collections, charge-offs, or other credit issues alongside tax debt, Crowned Credit can help. We specialize in disputing inaccurate negative items and helping people rebuild their credit while they get their finances back on track. Call us at 336-310-0090 or check out our pricing to see which plan fits your situation.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Results vary by individual circumstances. Crowned Credit cannot guarantee specific outcomes or timelines. For tax-specific guidance, consult a licensed tax professional or enrolled agent.