Pay for Delete Letters: How to Negotiate Collections Off Your Credit Report in 2026

Ashley Rivera

Credit Repair Specialist

You owe $800 to a collection agency. You're willing to pay it — but only if they wipe it from your credit report. That's the whole idea behind a pay for delete letter, and it's one of the most searched credit repair strategies for good reason. A single collection account can drag your score down 50 to 100 points, and paying it off without negotiating removal often does almost nothing for your score under older scoring models.

But here's the catch: pay for delete doesn't always work. Some collectors agree. Many don't. The credit bureaus technically discourage the practice. And if you handle it wrong, you can end up paying the full balance with the collection still sitting on your report.

This guide breaks down exactly how pay for delete works in 2026, who it works with, how to write a letter that actually gets results, and what your other options are when a collector says no.

What Is a Pay for Delete Letter?

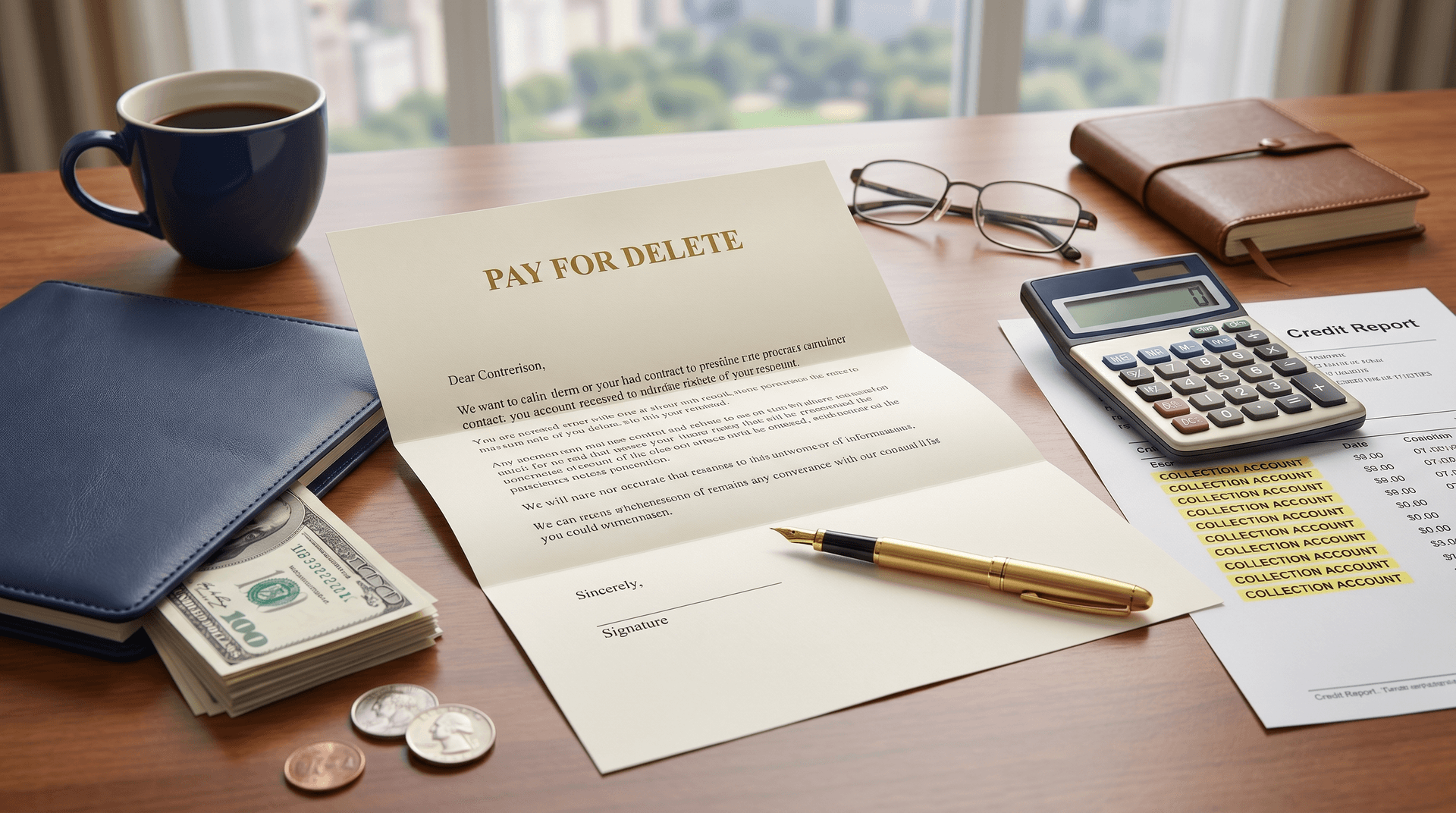

A pay for delete letter is a written offer you send to a collection agency proposing a deal: you'll pay some or all of the debt in exchange for them removing the account from your credit report entirely. Instead of the account showing as "paid collection" (which still looks bad), it disappears — like it was never there.

The strategy is built on a simple reality: collection agencies buy debt for pennies on the dollar. A medical bill that you owe $1,200 on might have been purchased by the collector for $60 to $120. They're playing a numbers game. If you offer them $600 and they get to close the file, many of them will take it — especially if removal is the only way you'll pay.

Pay for delete isn't a formal legal process. There's no section of the Fair Debt Collection Practices Act (FDCPA) or Fair Credit Reporting Act (FCRA) that specifically addresses it. It's a negotiation between you and the collector, and the terms are whatever you both agree to.

Is Pay for Delete Legal?

Yes. No federal law prohibits pay for delete agreements. The FCRA requires that information reported to credit bureaus be accurate, but there's no law that forces a collector to report an account at all. If they choose to stop reporting it after you've paid, that's their call.

That said, the credit bureaus — Equifax, Experian, and TransUnion — have policies discouraging data furnishers from removing accurate information as part of payment negotiations. Their contracts with collectors typically state that reported information should only be removed if it's inaccurate.

In practice, collectors ignore this policy all the time. Smaller collection agencies and debt buyers are far more likely to agree to pay for delete than large, well-known agencies. The bureaus rarely enforce the policy, and collectors know it.

Which Collection Agencies Accept Pay for Delete?

There's no official list, and agencies change their policies frequently. But here's what tends to hold true in 2026:

More likely to agree:

- Small, local collection agencies

- Medical collection agencies (especially since many medical debts under $500 no longer appear on credit reports as of 2023)

- Debt buyers who purchased your account for a fraction of the balance

- Agencies with older accounts (3+ years) they've struggled to collect on

Less likely to agree:

- Portfolio Recovery Associates (PRA) — generally refuses pay for delete

- Midland Credit Management — inconsistent, but trending toward refusal

- LVNV Funding — sometimes agrees, depends on the account

- Original creditors reporting directly (banks, credit card companies) — almost never agree

That said, even agencies that "don't do pay for delete" have individual reps who might agree on a case-by-case basis. Policies vary by office and by how old the debt is.

How to Write a Pay for Delete Letter That Works

Your letter needs to be direct, professional, and specific. Vague requests get ignored. Here's the structure that gets the best response rates:

1. Identify the account clearly

Include the collection agency name, your account number, the original creditor, and the balance they're reporting. Don't make them guess which account you're writing about.

2. Make a specific dollar offer

Don't say "I'd like to settle this." Say "I'm prepared to pay $450 to resolve this $800 balance." Start low — 40% to 60% of the balance is a reasonable opening offer for debts that are more than a year old. For newer debts, you might need to go higher.

3. State your condition clearly

The entire point of the letter is the condition: you'll pay only if they agree to delete the account from all three credit bureaus within 30 days of receiving payment. Be explicit. Write it out.

4. Request a written agreement

Ask them to respond in writing — on their letterhead — confirming they'll delete the account after payment. This is your protection. Without written confirmation, you have no proof of the deal.

5. Set a deadline

Give them 30 days to respond. This creates urgency and keeps you from waiting indefinitely.

Sample pay for delete letter

Here's a template you can adapt:

[Your Name]

[Your Address]

[Date]

[Collection Agency Name]

[Agency Address]

Re: Account #[Your Account Number]

Original Creditor: [Name]

Balance Reported: $[Amount]

To Whom It May Concern,

I am writing regarding the above-referenced account currently reported on my credit file. I am prepared to pay $[Your Offer Amount] as settlement in full for this account, contingent on your agreement to the following condition:

Upon receipt of my payment, you will request deletion of this account from my credit reports with Equifax, Experian, and TransUnion within 30 calendar days. This means the account will no longer appear on my credit reports in any status — not as "paid," "settled," or "closed," but fully removed.

If you agree to these terms, please respond in writing on company letterhead within 30 days of this letter. Upon receipt of your written agreement, I will submit payment via [certified check / money order].

I will not submit payment without a written agreement confirming deletion.

Sincerely,

[Your Name]

Critical Mistakes to Avoid

People mess this up more often than they get it right. Here are the traps:

Paying before getting a written agreement. This is the number one mistake. Once a collector has your money, their incentive to cooperate drops to zero. Never pay first, then hope they'll honor a verbal promise.

Calling instead of writing. Phone calls aren't documented. Even if a collector agrees on the phone, you have no proof. Always put your offer in writing and require a written response. If you do negotiate by phone, follow up with a letter confirming the terms discussed and ask for written confirmation before sending payment.

Paying with a personal check or debit card. A personal check gives the collector your bank account and routing number. A debit card gives them ongoing access to charge your account. Use a certified check or money order — something that can't be reversed or exploited.

Admitting the debt is yours. Your pay for delete letter should reference the account by number without explicitly stating "I owe this debt." Why? If the negotiation falls apart, you don't want a letter on file that could be used against you in court. Stick to neutral language like "the above-referenced account."

Resetting the statute of limitations. In many states, making a partial payment or even acknowledging a debt in writing can restart the clock on the statute of limitations. If your debt is close to the SOL expiration, a pay for delete letter might not be worth the risk. Check your state's statute of limitations before sending anything.

What to Do When a Collector Says No

Roughly half of pay for delete attempts get rejected. That's not the end of the road — it just means you need a different strategy.

Dispute the account under the FCRA

Under the Fair Credit Reporting Act, every item on your credit report must be verifiable. If a collector can't produce the original signed agreement, detailed account records, and proper chain of ownership documentation, the bureau must remove the account. This is the backbone of professional credit repair — and it's more effective than most people realize.

At Crowned Credit, this is core to what we do. Our team files strategic disputes with the bureaus and directly with creditors, leveraging your rights under the FCRA to challenge items that can't be properly verified. A lot of collection accounts — especially older ones and medical debts — have documentation gaps that force removal.

Send a debt validation letter

If the collection is new (within 30 days of their first contact), you have the right under the FDCPA to demand validation. The collector must provide proof that the debt is yours, the amount is correct, and they have the legal right to collect it. If they can't validate it within 30 days, they're required to stop collection activity — and you can dispute the account with the bureaus. Check out our guide on how to remove collections from your credit report for the full process.

Wait it out

Collections fall off your credit report after 7 years from the date of first delinquency on the original account. If the account is 5 or 6 years old, paying it might not make sense — especially under FICO 9 and VantageScore 3.0, which ignore paid collections entirely. Run the math before making any decisions.

Negotiate a "paid in full" status instead

If the collector won't delete, try negotiating payment in exchange for updating the account to "paid in full" rather than "settled for less than owed." Under newer scoring models (FICO 9, FICO 10, VantageScore 3.0+), paid collections have zero impact on your score. Many mortgage lenders now use these models.

Pay for Delete vs. Professional Credit Repair: What's the Difference?

A pay for delete letter targets one account at a time. You're negotiating directly with a single collector, and the outcome depends entirely on whether that collector feels like cooperating.

Professional credit repair takes a broader approach. A credit repair company reviews your entire credit profile, identifies every item that can potentially be challenged, and files disputes strategically across all three bureaus — often simultaneously. They know which creditors have weak documentation, which dispute reasons get the fastest results, and how to escalate when bureaus push back.

The advantage of professional help is scale and expertise. Instead of spending months writing individual letters and tracking responses, you have a team handling everything — including items you might not realize are disputable.

Crowned Credit's Accelerated plan ($249 + $199/month) covers disputes across all three bureaus, creditor interventions, and ongoing monitoring. For someone with multiple negative items — collections, charge-offs, late payments, inquiries — it's significantly more efficient than trying to negotiate each one individually.

If you're dealing with just one small collection and you want to try handling it yourself first, a pay for delete letter is worth the attempt. But if your credit report has multiple issues dragging your score down, working with a professional team will get you further, faster.

The FICO Score Impact: What Actually Happens After Deletion

Let's talk numbers, because this is where people get confused.

When a collection account is deleted from your credit report, the impact depends on what else is on your report. If that collection was your only negative item and the rest of your credit history is clean, you could see a score jump of 50 to 100+ points. If you have multiple negatives, removing one collection might bump your score 20 to 40 points.

Here's what's important to understand about scoring models in 2026:

- FICO 8 (still the most widely used): Counts all unpaid collections against you. Paid collections still hurt, though slightly less. This is where pay for delete matters most — because under FICO 8, even a paid collection damages your score.

- FICO 9 and FICO 10: Ignore paid collections entirely. If you pay a collection without getting it deleted, these models won't penalize you for it.

- VantageScore 3.0+: Also ignores paid collections. Growing in usage among fintech lenders and credit card issuers.

The problem: most mortgage lenders, auto lenders, and banks still use FICO 8 or similar older models for lending decisions. So "paid collection" still hurts you where it counts most — which is exactly why pay for delete remains relevant in 2026.

Timing Your Pay for Delete Letter

Timing matters more than most people think:

Best time to negotiate: When the debt is 6 months to 3 years old. The collector has had time to realize the account is difficult, but it's still worth their effort to negotiate.

Worst time to negotiate: Right after the account hits collections. At this point, the collector paid close to full price for the account and expects to collect the full amount. Your leverage is low.

End of month and end of quarter: Collection agents have quotas. If they're behind on their numbers heading into the last week of a month or quarter, they're more likely to accept a lower settlement and agree to deletion terms. This is a small edge, but it's real.

After a failed first attempt: If a collector rejects your initial letter, wait 60 to 90 days and try again. Personnel changes, policy updates, and the passage of time all work in your favor. The older the debt gets, the more willing they become.

What About Medical Collections?

Medical debt gets special treatment in 2026. Since 2023, the three major credit bureaus no longer report medical collections under $500. Any medical collection that's been paid should also be removed, regardless of the amount — this was a policy change by the bureaus, not a law.

If you have a medical collection over $500 that's still reporting, pay for delete is worth trying. Medical collection agencies tend to be more flexible than financial debt collectors, and many providers will work with you if you call the original billing office directly.

For a deeper look at how medical debt affects your report, read our medical debt and credit report guide.

Next Steps: Building a Plan

Here's the honest assessment: pay for delete works sometimes. It's a legitimate strategy, and if you have one or two collection accounts from smaller agencies, it's worth sending the letter. Budget 30 to 60 days per account for the negotiation process.

But most people dealing with collections also have other issues on their report — late payments, charge-offs, hard inquiries, high utilization. A single pay for delete letter won't fix all of that.

If you want to tackle everything at once, book a free consultation with Crowned Credit. We'll pull your reports, identify every item that's potentially removable under the FCRA, and build a dispute strategy that covers your entire credit profile — not just one collection at a time.

Call us at 336-310-0090 or schedule online.

Disclaimer: Credit repair is not guaranteed. Results vary based on individual credit profiles and the accuracy of reported information. Under the Credit Repair Organizations Act (CROA), no company can guarantee specific credit score improvements or the removal of accurate, verifiable information from your credit report. Crowned Credit disputes items on your behalf using your rights under the FCRA, and results depend on whether creditors and bureaus can verify the items in question.