Soft Pull vs Hard Pull: What's the Difference and Which One Hurts Your Credit Score?

Ashley Rivera

Credit Repair Specialist

You're checking your credit report and notice two sections: "soft inquiries" and "hard inquiries." Or maybe you're about to apply for a credit card and the website promises a "pre-approval with no impact to your credit score." What does that actually mean?

Here's what most people don't realize: not all credit checks are the same. Some can ding your score by several points. Others? They're completely invisible to lenders and won't affect your creditworthiness at all.

If you've ever been confused about soft pulls versus hard pulls—or worse, avoided checking your credit because you thought it would hurt your score—this guide will clear everything up.

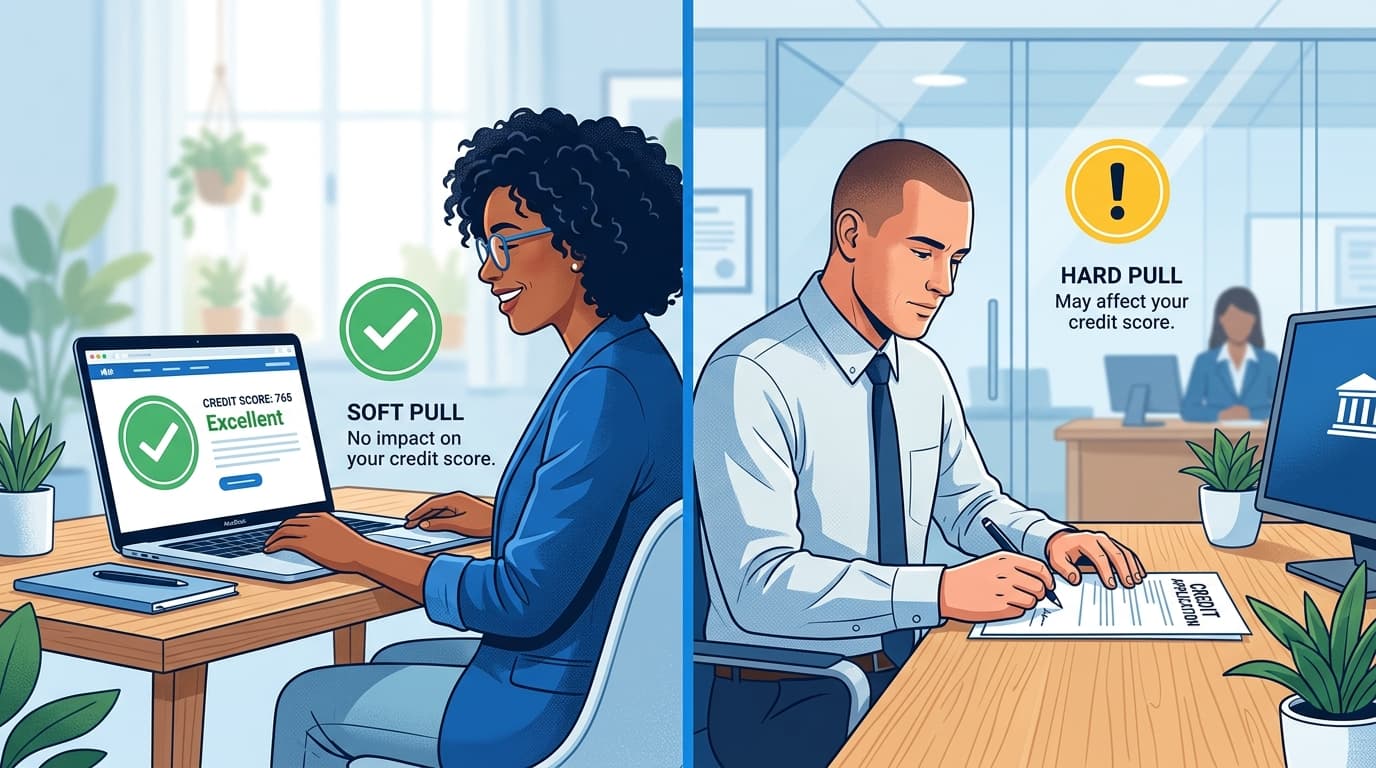

What Is a Soft Pull (Soft Inquiry)?

A soft pull, also called a soft inquiry or soft credit check, happens when someone reviews your credit report for non-lending purposes. The key thing to understand: soft pulls do not affect your credit score. Period.

Think of a soft pull as a background check. It shows your credit history, but it's not tied to an actual credit application. Because you're not actively seeking new credit, scoring models ignore soft inquiries entirely.

Common Examples of Soft Pulls:

- Checking your own credit report — Yes, you can check your credit as often as you want without penalty. Services like Credit Karma, Credit Sesame, or pulling your free annual reports from AnnualCreditReport.com all use soft pulls.

- Pre-approval offers — When a credit card company sends you a "you're pre-approved" mailer, they did a soft pull to see if you qualify.

- Background checks by employers — If an employer checks your credit during the hiring process, it's a soft inquiry.

- Existing creditors reviewing your account — Your credit card company might periodically review your credit to decide whether to increase your limit or adjust your terms.

- Rental applications — Many landlords use soft pulls to screen tenants without impacting their credit scores.

- Insurance quotes — Insurers often check your credit-based insurance score using a soft inquiry.

Here's the bottom line: if you didn't apply for credit, it's almost always a soft pull.

What Is a Hard Pull (Hard Inquiry)?

A hard pull, also called a hard inquiry or hard credit check, happens when a lender reviews your credit report as part of their decision to lend you money. Hard pulls require your permission—either through a signed application or an online authorization—and they can temporarily lower your credit score by 5 to 10 points.

Hard inquiries signal to other lenders that you're actively seeking credit, which can be seen as a risk factor (especially if you have multiple hard pulls in a short period).

Common Examples of Hard Pulls:

- Applying for a credit card — When you submit a credit card application, the issuer does a hard pull to evaluate your creditworthiness.

- Mortgage applications — Lenders pull your credit to determine your interest rate and loan eligibility.

- Auto loans — Car dealerships and auto lenders run hard inquiries when you finance a vehicle.

- Personal loans — Whether it's through a bank, credit union, or online lender, applying for a personal loan triggers a hard pull.

- Student loans — Federal student loans don't require credit checks, but private student loans do—and that's a hard inquiry.

- Opening a new bank account (sometimes) — Some banks use ChexSystems or pull your credit to verify your identity or check for overdraft risk.

- Applying for a lease or financing agreement — Furniture financing, electronics payment plans, and similar credit-based purchases generate hard inquiries.

The key difference? You're asking to borrow money or open a credit account. That's when a hard pull happens.

How Much Does a Hard Pull Hurt Your Credit Score?

Let's get specific. According to FICO, a single hard inquiry typically drops your credit score by less than 5 points for most people. For those with shorter credit histories or fewer accounts, the impact can be closer to 10 points.

The good news? Hard inquiries only stay on your credit report for two years, and they stop affecting your score after 12 months. FICO Score 8 and newer models only count inquiries from the past 12 months in their calculations.

Multiple Hard Pulls: The Rate Shopping Exception

Here's where it gets interesting. Credit scoring models understand that smart borrowers shop around for the best rates. So when you're applying for a mortgage, auto loan, or student loan, multiple hard inquiries within a 14-45 day window are treated as a single inquiry.

This "rate shopping buffer" exists so you're not penalized for comparing lenders. FICO Score 8 uses a 45-day window; older FICO models use 14 days. VantageScore 3.0 and 4.0 use a 14-day window.

Important: This exception only applies to the same type of credit. If you apply for a mortgage, an auto loan, and three credit cards in the same month, those will count as separate hard pulls—and that can significantly hurt your score.

Side-by-Side Comparison: Soft Pull vs Hard Pull

| Factor | Soft Pull | Hard Pull |

|---|---|---|

| Requires Your Permission? | No | Yes |

| Impacts Credit Score? | No | Yes (5-10 points) |

| Visible to Other Lenders? | No | Yes |

| Stays on Credit Report? | May appear, but doesn't count | 2 years |

| Affects Score For How Long? | Never | Up to 12 months |

| Examples | Pre-approvals, checking your own credit, employer checks | Credit card apps, mortgage apps, auto loans |

Can You Remove Hard Inquiries From Your Credit Report?

Yes—but only if they're unauthorized or fraudulent.

If you didn't authorize a hard inquiry, or if you suspect identity theft, you have the right to dispute it with the credit bureaus. Each bureau (Equifax, Experian, and TransUnion) must investigate and remove the inquiry if it's invalid.

However, if you did authorize the inquiry—even if you didn't end up getting approved or completing the application—the inquiry is legitimate and will stay on your report for two years.

Some credit repair companies claim they can remove authorized hard inquiries, but be cautious. Under FCRA (Fair Credit Reporting Act), bureaus are only required to remove inaccurate or unverified information. If the inquiry is accurate, it's unlikely to be removed unless the creditor voluntarily agrees to delete it, which is rare.

Need help disputing unauthorized inquiries? Book a free consultation with Crowned Credit and we'll walk you through the process.

Myths About Credit Inquiries (Debunked)

Myth #1: "Checking your own credit hurts your score."

False. Checking your own credit is always a soft pull. You can check it daily if you want. In fact, we recommend checking it regularly to catch errors early.

Myth #2: "Pre-qualified and pre-approved mean the same thing."

Not quite. "Pre-qualified" usually means a soft pull was done to estimate whether you'd be approved. "Pre-approved" often means the lender has done a more thorough review and is confident you'll be approved—but you still need to submit a formal application (which triggers a hard pull) to finalize the offer.

Myth #3: "Multiple hard pulls don't matter if you're denied."

Wrong. Whether you're approved or denied, the hard inquiry still appears on your report and affects your score. The inquiry shows that you applied, not whether you were approved.

Myth #4: "Soft pulls don't show up on your credit report."

Partially true. Soft inquiries may appear on your credit report when you view it yourself, but they're not visible to lenders and they don't affect your score. Some credit monitoring services show soft inquiries to give you a complete picture of who's checking your credit.

How to Minimize Hard Inquiries

You can't avoid hard pulls entirely if you want to build credit or take out loans, but you can be strategic:

- Use pre-qualification tools — Many credit card issuers and lenders offer pre-qualification that only uses a soft pull. Check if you're likely to be approved before submitting a formal application.

- Limit credit applications — Only apply for credit when you actually need it. Avoid applying for multiple credit cards in a short period unless you're rate shopping for the same type of loan.

- Do your rate shopping within a short window — If you're applying for a mortgage or auto loan, submit all applications within 14-45 days so they count as one inquiry.

- Ask before applying — Some lenders will tell you upfront whether they'll do a hard or soft pull. If you're unsure, ask before you authorize a credit check.

- Dispute unauthorized inquiries immediately — If you see a hard inquiry you didn't authorize, dispute it right away.

What to Do If You Have Too Many Hard Inquiries

If you've applied for credit multiple times recently and your score has dropped, don't panic. Here's what you can do:

- Stop applying for new credit — Give your credit a break. Hard inquiries lose their scoring impact after 12 months, so time will help.

- Focus on positive payment history — Payment history is the biggest factor in your credit score (35% for FICO). Making on-time payments will outweigh the impact of inquiries.

- Keep credit utilization low — Use less than 30% of your available credit (ideally under 10%). This helps offset the negative impact of hard pulls.

- Dispute any unauthorized inquiries — Check your credit report for hard pulls you didn't authorize and dispute them with the bureaus.

- Work with a credit repair professional — If you're overwhelmed or unsure how to proceed, Crowned Credit can help you develop a personalized strategy to rebuild your score.

CROA Disclosure: Crowned Credit does not guarantee specific score increases or timeline results. Every credit situation is unique. While we have helped thousands of clients improve their credit through strategic dispute processes and credit-building strategies, individual results will vary based on your unique credit profile and the responsiveness of credit bureaus and creditors.

Final Thoughts: Know Before You Apply

Understanding the difference between soft pulls and hard pulls is one of the simplest ways to protect your credit score. The rule of thumb?

- Soft pulls = no harm. Check your credit as often as you want.

- Hard pulls = minor, temporary impact. Be strategic about when you apply for credit, but don't avoid applying altogether if you need it.

If you're working on building or repairing your credit, knowing when a credit check will affect your score can help you make smarter financial decisions. And if you have inaccurate hard inquiries dragging down your score, Crowned Credit can help you dispute them under the FCRA.

Book a free consultation today and let's create a plan to get your credit where it needs to be. Whether you're preparing to buy a home, finance a car, or simply want better credit options, we're here to help.

Questions? Call us at 336-310-0090. We're ready to help you take control of your credit.

View our pricing plans | Learn more about credit basics | How to remove hard inquiries