Enhanced Recovery Company (ERC) on Your Credit Report: How to Deal with Them and Remove It

Ashley Rivera

Credit Repair Specialist

You pull your credit report to prepare for a mortgage, a new car, or a business loan, and your score has unexpectedly plummeted. You spot a collections account from Enhanced Recovery Company (often listed as ERC, ERC Collections, or Enhanced Recovery Corp). If you have ever had a cell phone contract, cable TV, internet, or a utility account, this entry is almost certainly connected to one of those services.

Enhanced Recovery Company is one of the largest debt collection agencies in the United States. Hired by telecommunications, utility, and cable companies, they recover unpaid bills, unreturned equipment fees, and early termination penalties. Because a utility or telecom collection on your record can drag down your credit score and signal to future providers that you are high-risk, dealing with ERC is urgent. Fortunately, consumer credit laws give you powerful tools to challenge and remove Enhanced Recovery Company from your credit files. This guide walks you through how they operate and the steps to remove them in 2026.

Who Is Enhanced Recovery Company (ERC)?

Enhanced Recovery Company, LLC (ERC) is a third-party debt collection agency founded in 1999 and headquartered in Jacksonville, Florida. They are a massive operation with call centers globally. Their primary specialization is the collection of debt for the telecommunications and utility sectors.

If you see ERC on your credit report, they are likely collecting on behalf of major providers, which include:

- Telecommunications Giants: AT&T, Verizon, T-Mobile, and Sprint.

- Cable and Internet Providers: Comcast (Xfinity), Charter Communications (Spectrum), Cox, and CenturyLink.

- Utility Companies: Local electric, natural gas, water, and trash services.

When you cancel a service or move, these providers do not spend their own resources chasing unpaid balances. Instead, they hand the account over to ERC. ERC either acts as a collection agent on commission or buys the debt outright for pennies on the dollar, meaning they now own the debt and keep whatever they collect.

Why Is There an ERC Entry on My Report?

Many consumers are blindsided by an Enhanced Recovery Company collection because they believed their original accounts were in good standing. There are several common reasons why these accounts get sent to ERC without your knowledge:

1. Unreturned Equipment Fees

This is the most common source of ERC collections. When you cancel cable or internet, the provider requires you to return their modems, routers, and TV boxes. Even if you returned the equipment, the provider's warehouse often fails to log the return. They charge you hundreds of dollars for "unreturned equipment" and send that balance directly to ERC.

2. Billed After Cancellation

It is common for telecom companies to continue billing customers after a verbal cancellation. If you called to cancel your service, but the representative failed to process the request, the company will continue to charge you. When you refuse to pay for services you never used, those unpaid fees are packaged as a delinquent balance and sent to collections.

3. Moving and Missing the Final Bill

When you move, your final utility or internet bill is generated after you leave. If you did not set up paperless billing or mail forwarding, that final paper bill is sent to your old address. Because you never received it, you never paid it. Months later, the provider writes off the loss and transfers the account to ERC, who places a collection mark on your credit reports.

4. Early Termination Fees (ETFs)

Many cell phone and internet plans involve long-term contracts. If you break the contract early—even due to poor service or moving to an area where the provider does not operate—the company will levy an early termination fee. If you refuse to pay this penalty, it is handed over to ERC.

The Damage of an ERC Collection Account

Having an active collection account from Enhanced Recovery Company on your credit report causes immediate, severe damage in two major ways:

1. It Slashes Your Credit Scores

A collection account is classified as a "serious delinquency" by credit scoring models. A single ERC collection can drop your credit score by 50 to 110 points. If you started with good credit, the drop is even more severe because you have further to fall. This drop can push you out of prime lending tiers, forcing you to pay thousands of dollars in extra interest on future loans.

2. It Triggers Rejections from Service Providers

When you apply for a new cell phone plan, home internet, or utility service, those providers run a credit check. Seeing an unpaid collection from a competitor like ERC on your record is a major red flag. They may refuse to open an account for you entirely, or they will demand an upfront security deposit of several hundred dollars before activating your service.

Why Telecom and Utility Collections Are Highly Vulnerable to Disputes

While discovering an ERC collection is stressful, there is a major silver lining: telecommunications and utility collections are among the easiest negative items to legally dispute and remove. This is because the billing practices of telecom companies are notoriously disorganized, and the chain of custody for third-party collections is frequently broken.

Under the Fair Credit Reporting Act (FCRA), credit bureaus and debt collectors are prohibited from reporting inaccurate, unverified, or incomplete information. If they are challenged and cannot verify every single dollar of that reported balance with actual, original documentation, they must delete the collection entry from your reports. ERC regularly fails to verify these accounts due to several recurring weaknesses:

1. The "Missing Contract" Problem

When ERC buys a debt, they usually receive nothing more than a digital spreadsheet containing your name, address, and a dollar amount. They rarely receive a copy of the actual, signed service agreement you entered into. If you dispute the debt and demand that ERC produce the original signed contract, and they cannot obtain it from the original creditor, they cannot legally verify the debt. Under the FCRA, unverified debt must be deleted.

2. The "Returned Equipment" Defense

If your ERC collection stems from an alleged unreturned modem or router, they must be able to prove that you actually kept the equipment. If you challenge them to produce the specific serial numbers and warehouse inventory records showing that the equipment was never received, ERC almost never has this information. If they cannot produce concrete proof, they cannot legally justify the charge, and the collection must be removed.

3. No Detailed Accounting Ledger

A debt collector cannot claim you owe a specific balance without being able to explain exactly how that number was calculated. Under federal law, you have the right to demand a complete itemization of the debt, including the original principal balance, late fees, and interest. Telecom bills are notorious for mysterious taxes and surcharges. If ERC cannot provide a day-by-day billing ledger showing exactly how the balance accumulated, the debt is legally unverified and must be deleted.

Step-by-Step Blueprint to Remove Enhanced Recovery Company

If you have an active collection from Enhanced Recovery Company on your credit file, do not panic. Do not pick up the phone to call them—phone collections reps are trained to use high-pressure tactics or get you to make a partial payment that restarts your state's statute of limitations. Always communicate in writing via certified mail to maintain a legal paper trail. Follow this step-by-step blueprint:

Step 1: Check the Dates and Identify the Account Details

Pull your credit reports from all three major bureaus and locate the Enhanced Recovery Company entry. Note the collection date, reporting balance, original creditor, and date of first delinquency.

Under the FCRA, a collection account can only remain on your credit report for seven years from the date of first delinquency. If the original incident occurred more than seven years ago, the debt is too old to be reported. If ERC has altered the dates to make the collection look newer, they are violating the FCRA by "re-aging" the debt, which is grounds for immediate deletion. You can learn more about how to spot and fight this in our guide on re-aging and re-insertion.

Step 2: Send a Formal Debt Validation Letter

If Enhanced Recovery Company has recently contacted you (within the last 30 days), you have the legal right under the Fair Debt Collection Practices Act (FDCPA) to demand formal debt validation. Send a Debt Validation Letter via Certified Mail with Return Receipt Requested.

In your letter, do not admit that you owe the money. State that you are disputing the validity of the debt and demand that they provide the following proof within 30 days:

- The original, signed service agreement with the provider.

- An itemized billing ledger showing a complete history of all charges, payments, and cancellations.

- A detailed breakdown of any alleged "unreturned equipment" fees, including specific serial numbers.

- Proof of their legal authority and debt collection license to collect debt in your state.

Because ERC is a third-party collection agency, they rarely possess this level of detailed documentation. When they request the files from your old provider, they often find that the files have been archived or lost. If ERC cannot produce these documents within the 30-day window, they cannot legally verify the debt and must delete the collection entry.

Step 3: Check Your State's Statute of Limitations on Debt

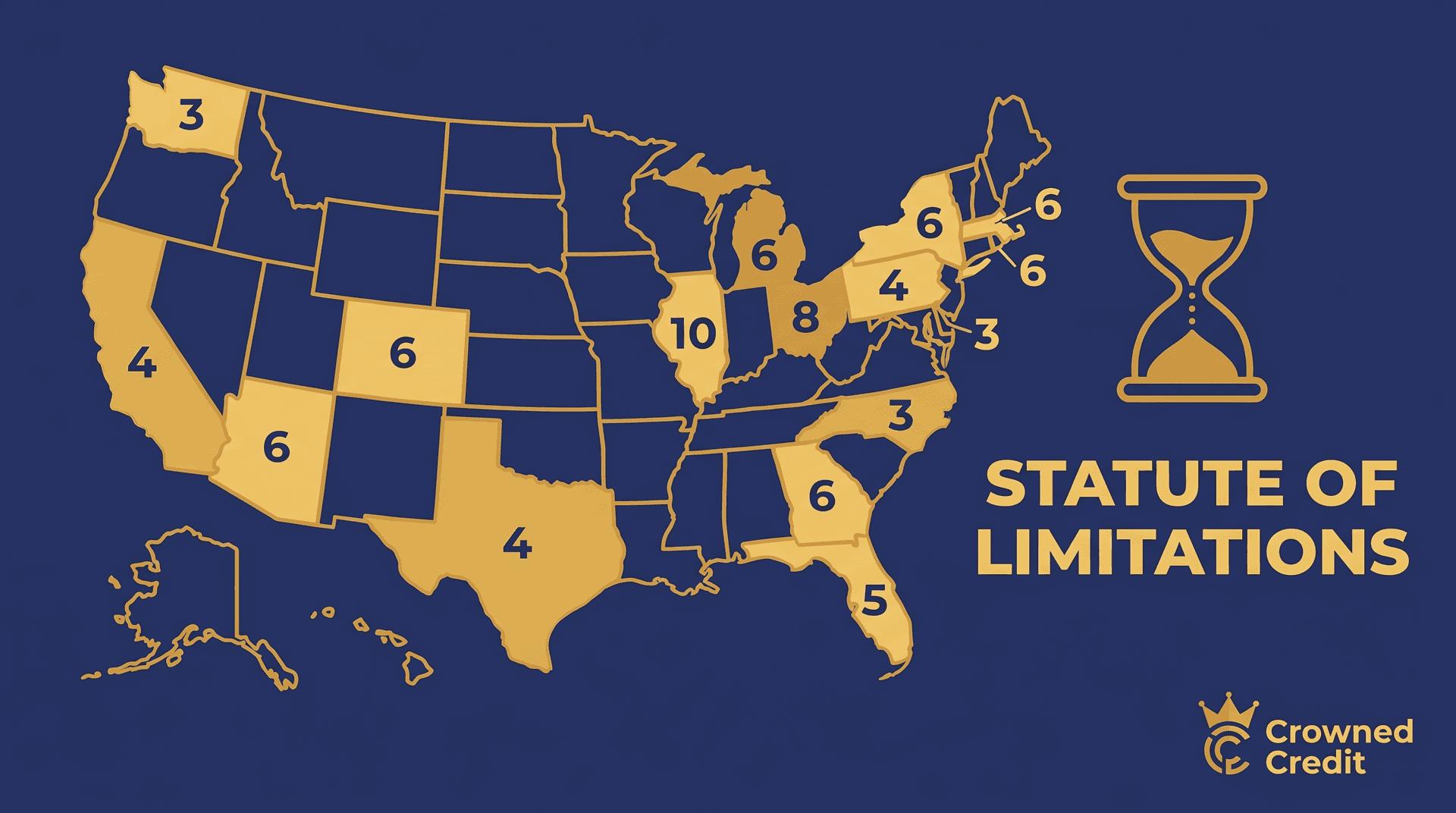

Every state has a statute of limitations (SOL) on how long a collector has the legal right to sue you in court to collect an unpaid debt. For utility and service bills, the SOL typically ranges from three to six years, depending on your state's laws.

If your state's SOL has expired, the debt is "time-barred." Enhanced Recovery Company can still write you letters or report the collection on your credit (up to the 7-year mark), but they cannot legally sue you in court. Knowing if the debt is time-barred gives you leverage. If they threaten to sue you over a time-barred debt, they are violating the FDCPA. Be careful: making even a tiny partial payment can restart the SOL clock from zero in many states. For a complete state-by-state list, review our resource on the statute of limitations on debt by state.

Step 4: File Disputes with the Credit Bureaus

If ERC fails to validate the debt, or if you identify inaccuracies in how they are reporting the account, dispute the entry directly with the credit bureaus. Write a separate dispute letter to Equifax, Experian, and TransUnion. Point out the specific inaccuracies and demand that they investigate the entry. You can learn more about how the bureaus handle this in our article on the three credit bureaus.

For example, you can write: "Enhanced Recovery Company is reporting account number XXXXX with an unverified balance of $480. I canceled this service, and the provider continued to charge me monthly fees after the cancellation date. Please investigate and delete this unverified and inaccurate information from my credit report."

Attach any proof you have (such as your cancellation confirmation or your UPS return receipt). Once the bureaus receive your dispute, they have 30 days to contact ERC and verify the account. If ERC cannot verify the exact balance, the bureaus must delete the entry. Learn more about your legal protections in our guide on FCRA dispute rights.

Step 5: Negotiate a Pay-for-Delete Agreement

If the debt is legally valid and ERC has fully validated it, your best remaining option is to negotiate a Pay-for-Delete agreement. Offer to pay a portion of the balance (usually starting at 30% to 50%) in exchange for Enhanced Recovery Company completely removing the collection entry from all credit bureaus.

Paying a collection without getting a delete agreement does not help your credit score; standard scoring models still treat paid collections as negative marks. When negotiating a Pay-for-Delete, follow these strict rules:

- Always negotiate in writing or via secure email. Never give them verbal access to your bank account or credit card.

- Get the agreement in writing before you send a single penny. The letter must explicitly state: "Upon receipt of payment in the amount of $X, Enhanced Recovery Company agrees to completely delete account number XXXXX from Equifax, Experian, and TransUnion."

- Once you receive the written agreement, pay the agreed amount using a cashier's check or a prepaid card. Do not give them your personal check or bank routing numbers.

Why You Should Hire a Professional Credit Repair Service

While you can legally dispute Enhanced Recovery Company on your own, the process is exhausting, stressful, and time-consuming. Telecom and utility collections require a deep understanding of federal laws like the FCRA and FDCPA, combined with a precise knowledge of utility-billing regulations. For a closer look at the mechanisms behind this, see our resource on charge-offs explained.

Enhanced Recovery Company is a highly aggressive agency. They deal with thousands of disputes daily and have automated systems designed to reject or ignore basic dispute templates. If you make a single technical mistake in your dispute letters—or say something that accidentally admits you owe the debt—you can permanently ruin your chances of getting the collection deleted.

At Crowned Credit, we have years of experience dealing directly with major telecommunications and utility collection agencies like Enhanced Recovery Company. Our team of credit experts conducts a complete forensic audit of your credit reports, analyzes your old service records, and cross-references them with federal consumer laws to find the exact violations needed to force a deletion.

We handle all the stress, drafting, and certified mailing for you, holding ERC strictly accountable to every word of the law. We offer three transparent, high-value service plans tailored to your needs:

- Essential Plan: $150 enrollment fee, then $99/month. Perfect for individuals with standard collections, medical bills, or late payments who need ongoing, reliable dispute management and credit building. See details on our pricing page.

- Accelerated Plan: $249 enrollment fee, then $199/month. Designed for aggressive, fast-paced credit rebuilding. Includes advanced disputes, priority processing, and strategic intervention for complex issues like telecom collections, repos, or charge-offs.

- Momentum Plan: $1,095 one-time fee. Our premier, all-inclusive plan for individuals who want a complete, white-glove credit transformation without any ongoing monthly fees.

If you are tired of letting an old utility or cell phone collection hold you back from renting the home you want, buying the car you deserve, or qualifying for the financing you need, let the professionals handle it. Contact Crowned Credit today at 336-310-0090 or visit getcrownedcredit.com/book-now to schedule your free credit consultation. We will analyze your credit reports, find the errors, and build a customized strategy to help you rebuild your financial future.

Legal Disclaimer: Crowned Credit is a credit repair organization as defined by the Credit Repair Organizations Act (CROA). Results vary based on individual circumstances and credit history. We do not guarantee the removal of any specific item from your credit report or promise any specific improvement in your credit score. Nothing in this article constitutes legal or financial advice. Consult a licensed attorney or financial advisor for advice specific to your situation.

Share this article: