How to Freeze the Secondary Credit Bureaus in 2026 (Step‑by‑Step Guide for Innovis, NCTUE, LexisNexis, ChexSystems, TeleCheck, and CoreLogic)

Ashley Rivera

Credit Repair Specialist

Short version: Freezing only Equifax, Experian, and TransUnion leaves gaps. Utilities, phone carriers, banks, check acceptance services, and risk databases often pull from secondary consumer reporting agencies you’ve never heard of—Innovis, NCTUE, LexisNexis (incl. SageStream), ChexSystems, TeleCheck, and CoreLogic Teletrack. This guide shows exactly how to place security freezes with each one in 2026, what to expect, and when to temporarily lift a freeze.

Who should freeze these “other” bureaus?

Three common scenarios:

- Identity theft or fraud risk: If someone has your SSN or you’ve had recent fraud attempts, these freezes close major loopholes.

- Applying for new services soon: If you’re about to start utilities, phone service, or open a bank account, you may want to wait to freeze or be ready to lift temporarily.

- You want a tighter security posture: Many lenders and telecom/utility providers check these databases. Closing them reduces unauthorized openings.

Freezes are free nationwide. Expect to verify identity (SSN, DOB, address, sometimes ID upload). Keep your confirmation numbers and PINs organized—you’ll need them to lift or remove freezes later.

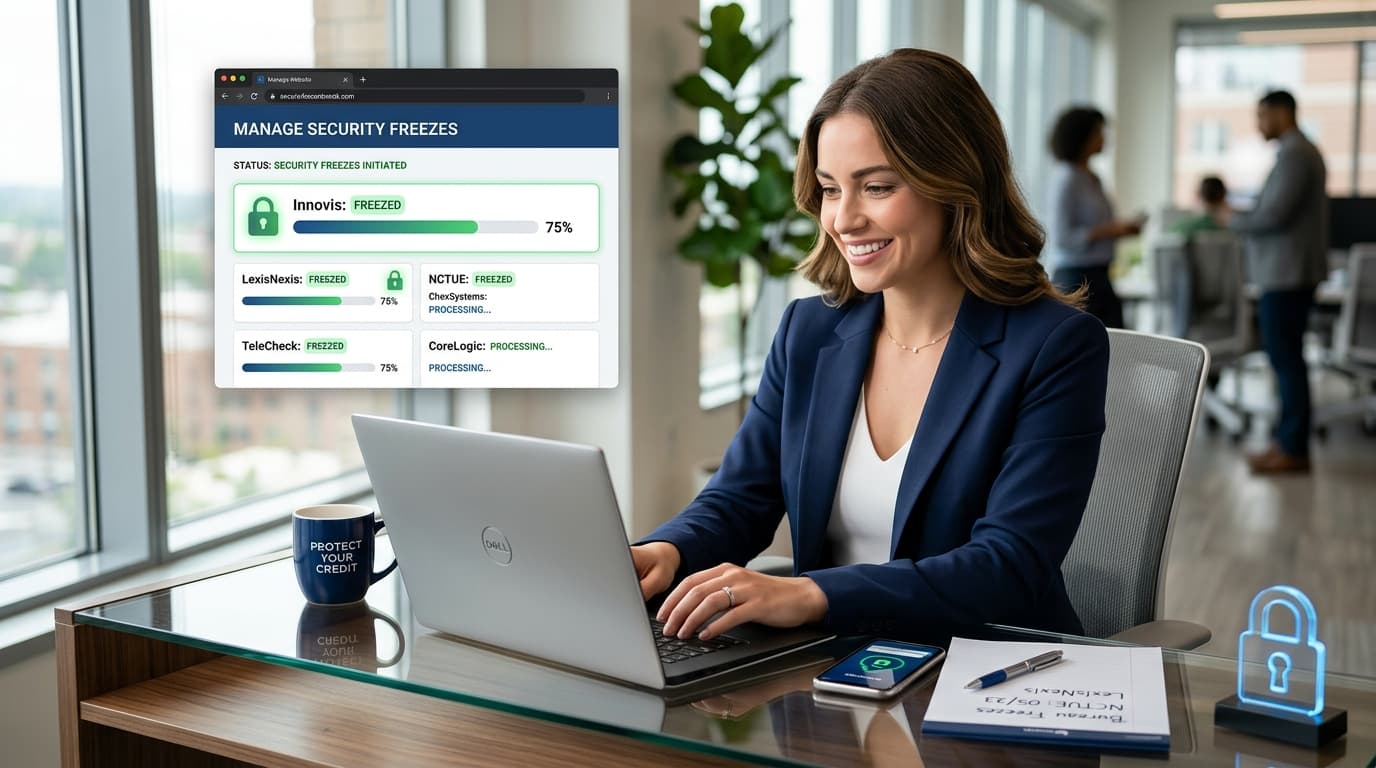

Quick links (official freeze portals)

- Innovis: innovis.com/personal/securityFreeze

- NCTUE (telecom & utilities): nctue.com/consumer (Exchange Service Center)

- LexisNexis (includes SageStream): consumer.risk.lexisnexis.com/freeze

- ChexSystems (bank account screening): chexsystems.com/security-freeze/place-freeze

- TeleCheck (check acceptance): getassistance.telecheck.com (support portal)

- CoreLogic Teletrack (subprime/alternative credit): consumers.teletrack.com/freeze

Note on SageStream: SageStream was integrated into LexisNexis Risk Solutions. A LexisNexis freeze typically covers SageStream consumer reports as well.

Step‑by‑step: Freeze each secondary bureau

1) Innovis — the “fourth bureau” many lenders check

Where to freeze: innovis.com/personal/securityFreeze or by phone at 800‑540‑2505.

What you’ll need: SSN, DOB, current address, and sometimes a copy of your ID or utility bill if Innovis can’t auto‑verify.

Pro tip: Innovis often issues a PIN or password for later lifts. Store it securely. If you’re shopping for a car or mortgage, ask the lender if they pull Innovis before you apply—lift only what’s required.

2) NCTUE — telecom and utilities data

Where to freeze: nctue.com/consumer. You can also call the Exchange Service Center at 866‑349‑5355 for automated freeze, lift, or removal options.

Why it matters: Phone carriers, internet providers, and utilities frequently check NCTUE. If someone tries to open a cell plan in your name, a freeze can stop it cold.

Timing tips: Planning a move? Start utilities first, then freeze. If you’re already frozen, request a temporary lift for the specific provider and date range.

3) LexisNexis (includes SageStream) — risk and identity data

Where to freeze: consumer.risk.lexisnexis.com/freeze. Phone support is typically 800‑456‑1244 for freeze assistance.

Why it matters: LexisNexis aggregates a huge amount of risk‑related data and powers many identity checks. Freezing can block certain approvals without your consent.

What to expect: You may receive a mailed confirmation. Keep the letter and any PIN in your records.

4) ChexSystems — bank account screening

Where to freeze: chexsystems.com/security-freeze/place-freeze. You can manage your freeze later via their consumer portal.

Heads up: If you freeze ChexSystems, some banks and credit unions may not be able to open a new checking/savings account for you until you lift it. Plan ahead and time your freeze around new account openings.

5) TeleCheck — check acceptance at retailers

Where to start: Use the TeleCheck Assistance portal to open a consumer support ticket or request guidance on freezing. Availability of an online self‑service freeze can vary; they may direct you to phone support or a mailed request.

Why it matters: If you still pay by check at some retailers, TeleCheck’s risk models can influence acceptance. A freeze can prevent misuse in your name.

6) CoreLogic Teletrack — alternative credit reporting

Where to freeze: consumers.teletrack.com/freeze.

Use cases: Teletrack is used in certain subprime or alternative‑credit decisions. If you’re improving your profile after past issues, a freeze can shut down unauthorized applications while you rebuild.

What about Early Warning Services (EWS)?

EWS is another bank‑account risk database used by many large banks. They don’t currently offer a standard online security freeze like the big three bureaus. If you’re dealing with identity theft tied to bank accounts, request your EWS consumer report and contact their consumer services for available protections and annotations.

How freezes interact with credit repair

Security freezes don’t stop you from disputing inaccurate, unverifiable, or incomplete information. Under the FCRA, furnishers and bureaus must verify what they report. At Crowned Credit, we use your consumer rights to challenge negative items across all relevant databases—professionally and with strategy.

- Freezes do help prevent new, unauthorized accounts while you clean up existing issues.

- If a lender or service provider needs access, you can temporarily lift a specific freeze for a date range—then re‑enable it.

- We’ll tell you exactly which freezes to lift for a mortgage/auto/utility start so your approvals aren’t delayed.

Step‑by‑step workflow you can follow today

- Download your current credit reports (all three) and review for accuracy. See: How to get your free credit report and How to read your credit report.

- Create a simple tracker (Notes/Spreadsheet) with columns: Bureau, Link/Phone, Date Frozen, Confirmation #/PIN, Notes.

- Freeze Innovis, NCTUE, LexisNexis, ChexSystems, TeleCheck, and Teletrack using the links above. Save confirmations immediately.

- Update your password manager with any portal logins or PINs (you’ll need them to lift a freeze later).

- Set reminders for any temporary lifts you create (date/time to re‑freeze).

Common questions we get

Will a freeze hurt my credit score?

No. A freeze restricts who can access your reports—it doesn’t change your score or your history.

Can I still apply for credit with freezes on?

Yes. You’ll just need to lift the relevant freezes temporarily so the lender can pull the data they use. Ask which bureaus they check.

Is freezing the big three (Equifax/Experian/TransUnion) enough?

It’s a strong start, but many telecom, utilities, and banks use secondary agencies. If you want a tighter lock, freeze those too.

How long does a freeze last?

Until you remove it. You can also set temporary lifts for a specific time window if you’re applying for something.

When to work with a professional

Freezes protect you from new fraud. They don’t fix existing negative items. If your reports have charge‑offs, collections, late payments, repos, or public record issues, a strategic dispute plan matters. Crowned Credit disputes all negative items using your FCRA rights and the furnisher’s duty to verify—not just “inaccurate items only.” We also advise when authorized user tradelines make sense as part of a broader rebuild plan.

Want a tailored plan? Book a free consultation or call 336‑310‑0090. We’ll review your goals, your reports, and map out the most efficient path forward.

Related resources

- How to Dispute Your LexisNexis Report (2026)

- Goodwill Letter (Remove Late Payments) — 2026 Guide

- Statute of Limitations on Debt by State (2026)

- Remove Hard Inquiries (2026)

- Your FCRA Dispute Rights

- Crowned Credit Pricing — Essential $150 + $99/mo, Accelerated $249 + $199/mo, Momentum $1,095 one‑time

What working with Crowned Credit looks like

- Strategic disputes across bureaus and furnishers using your consumer rights.

- Timeline coaching so you know which freezes to lift—and when—during home/auto/utility setups.

- Score‑building plan (utilization targets, mix, age, authorized users when appropriate).

Get a plan that fits your situation. Book now or call 336‑310‑0090.

Compliance notes and practical cautions

- Freezing is free and reversible. Keep confirmations and PINs safe.

- Plan ahead for applications—ask which bureaus a lender/provider uses and lift only what’s necessary.

- Disputes still work with freezes in place. Verification is required under the FCRA.

CROA & results disclaimer: We never guarantee specific outcomes or timelines. Credit improvement depends on your unique history, creditor responses, and ongoing credit behavior. Any score changes or removals mentioned in our materials are illustrative only.

Built by Crowned Credit for consumers who want real protection and a clear plan. If you want a professional team to handle the heavy lifting, book a call or see pricing.