Statute of Limitations on Debt by State (2026 Guide)

Ashley Rivera

Credit Repair Specialist

A debt collector just called about a credit card you stopped paying four years ago. They're threatening to sue. Should you panic?

Maybe not. Every state has a statute of limitations (SOL) on debt — a legal deadline after which creditors and collectors cannot sue you to collect what you owe. Once that deadline passes, the debt becomes "time-barred." The collector can still call you and send letters, but they can't drag you into court.

Here's the problem: most people don't know their state's SOL. Collectors count on that ignorance. They'll threaten lawsuits on debts they legally can't sue over, hoping you'll pay out of fear. And if you accidentally restart the clock — by making even a small payment — you could lose your protection entirely.

This guide breaks down the statute of limitations for all 50 states, explains what time-barred debt actually means, and covers the mistakes that cost people thousands of dollars.

What Is the Statute of Limitations on Debt?

The statute of limitations on debt is a state law that sets a time limit on how long a creditor or debt collector can file a lawsuit to force you to pay. Once the time limit expires, the debt is considered "time-barred."

A few critical things to understand upfront:

- The debt doesn't disappear. You still technically owe it. The SOL only removes the right to sue you over it.

- Collectors can still contact you. Phone calls, letters, and even negative credit reporting can continue after the SOL expires.

- The SOL is different from credit reporting limits. Under the Fair Credit Reporting Act (FCRA), most negative items stay on your credit report for 7 years from the date of first delinquency — regardless of your state's SOL.

- The clock starts on your last payment date. Not the date the account was opened, not the date it went to collections. The date you last made a payment (or in some states, the date of last activity).

So a debt can be past the statute of limitations (meaning they can't sue) but still sitting on your credit report dragging your score down. That distinction matters a lot.

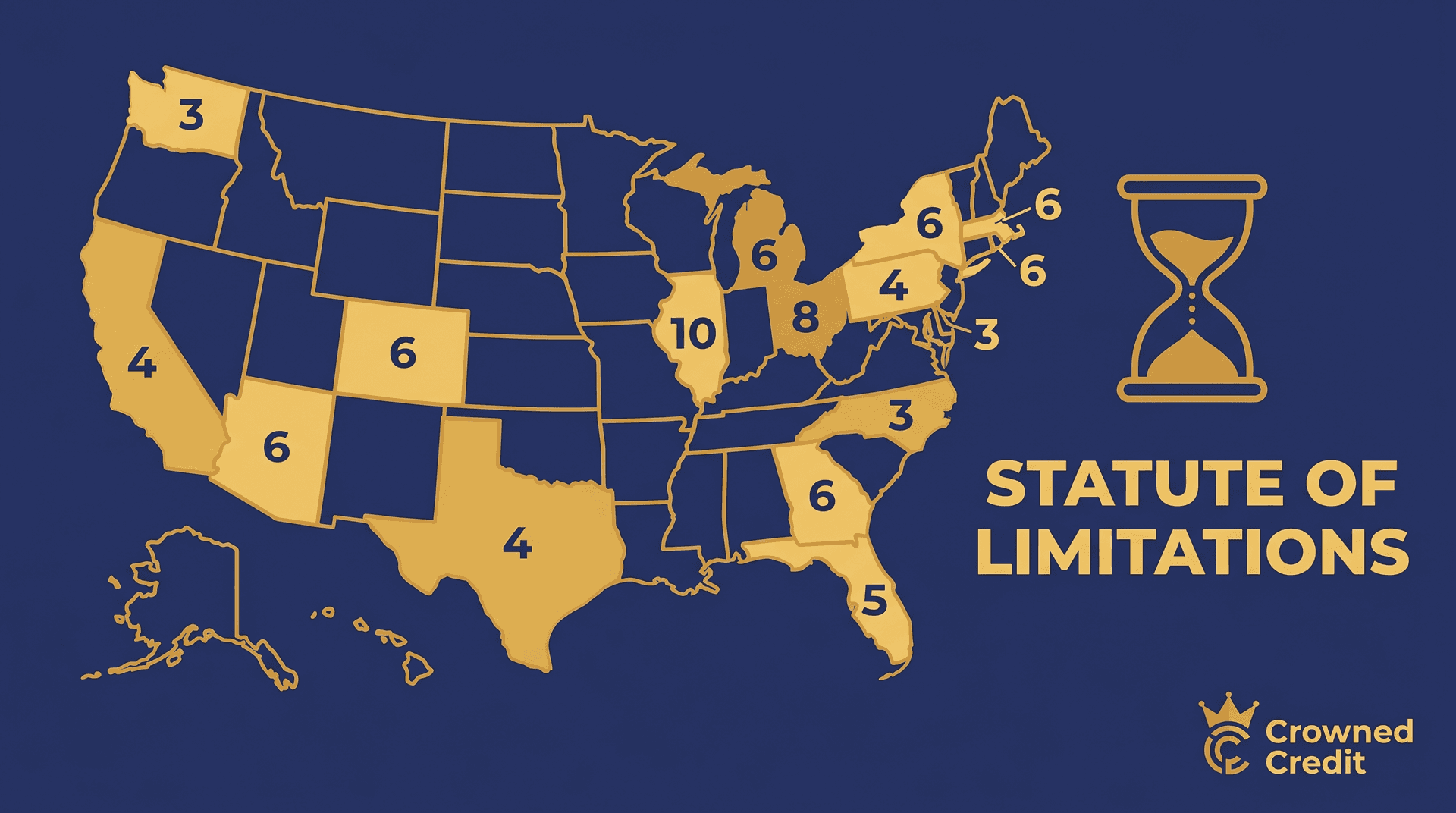

Statute of Limitations by State: 2026 Chart

Each state sets its own SOL, and the timeline depends on the type of debt. Here are the numbers for open-ended accounts (credit cards, lines of credit) and written contracts (personal loans, auto loans, medical debt with a signed agreement):

| State | Credit Cards / Open-Ended | Written Contracts |

|---|---|---|

| Alabama | 3 years | 6 years |

| Alaska | 3 years | 6 years |

| Arizona | 6 years | 6 years |

| Arkansas | 5 years | 5 years |

| California | 4 years | 4 years |

| Colorado | 6 years | 6 years |

| Connecticut | 6 years | 6 years |

| Delaware | 4 years | 3 years |

| D.C. | 3 years | 3 years |

| Florida | 5 years | 5 years |

| Georgia | 6 years | 6 years |

| Hawaii | 6 years | 6 years |

| Idaho | 4 years | 5 years |

| Illinois | 5 years | 10 years |

| Indiana | 6 years | 10 years |

| Iowa | 5 years | 10 years |

| Kansas | 3 years | 5 years |

| Kentucky | 10 years | 10 years |

| Louisiana | 3 years | 10 years |

| Maine | 6 years | 6 years |

| Maryland | 3 years | 3 years |

| Massachusetts | 6 years | 6 years |

| Michigan | 6 years | 6 years |

| Minnesota | 6 years | 6 years |

| Mississippi | 3 years | 3 years |

| Missouri | 5 years | 10 years |

| Montana | 5 years | 8 years |

| Nebraska | 4 years | 5 years |

| Nevada | 4 years | 6 years |

| New Hampshire | 3 years | 3 years |

| New Jersey | 6 years | 6 years |

| New Mexico | 4 years | 6 years |

| New York | 3 years | 3 years |

| North Carolina | 3 years | 3 years |

| North Dakota | 6 years | 6 years |

| Ohio | 6 years | 6 years |

| Oklahoma | 3 years | 5 years |

| Oregon | 6 years | 6 years |

| Pennsylvania | 4 years | 4 years |

| Rhode Island | 10 years | 4 years |

| South Carolina | 3 years | 3 years |

| South Dakota | 6 years | 6 years |

| Tennessee | 6 years | 6 years |

| Texas | 4 years | 4 years |

| Utah | 4 years | 6 years |

| Vermont | 6 years | 6 years |

| Virginia | 3 years | 5 years |

| Washington | 6 years | 6 years |

| West Virginia | 5 years | 10 years |

| Wisconsin | 6 years | 6 years |

| Wyoming | 8 years | 10 years |

Key takeaway: 13 states have a 3-year SOL for credit card debt. If you're in North Carolina, New York, Maryland, or Mississippi, your window is short — and that actually works in your favor when a collector comes knocking on an old debt.

How the Clock Works (and How It Restarts)

The SOL clock starts on the date of your last payment or last account activity, depending on the state. Here's an example:

Say you live in Texas (4-year SOL for credit cards). Your last payment on a Discover card was March 2022. The statute of limitations would expire in March 2026. After that date, Discover — or whatever collection agency bought the debt — cannot legally sue you.

But here's where people get burned:

Actions That Can Restart the Clock

- Making any payment — even $5 — can reset the entire SOL in most states

- Signing a written agreement to pay or setting up a payment plan

- Acknowledging the debt in writing — some states interpret this as restarting the clock

Actions That Do NOT Restart the Clock

- Answering a collector's phone call

- Verbally saying "yes, I owe that" (in most states — but be careful)

- The debt being sold to a new collection agency

- A collector reporting the debt to a credit bureau

This is exactly why consumer attorneys tell people: never make a partial payment on old debt without understanding your state's SOL rules first. A well-meaning $25 payment on a $3,000 debt that was about to expire could give the collector another 3-6 years to sue you.

Time-Barred Debt vs. Credit Report Removal: They're Not the Same

This is the single biggest point of confusion, and collectors exploit it constantly.

The statute of limitations controls whether a collector can sue you. It varies by state — anywhere from 3 to 10 years.

The credit reporting period controls how long a negative item stays on your credit report. Under the FCRA, that's 7 years from the date of first delinquency for most items (10 years for bankruptcies).

These two clocks run independently. So you can have a debt that's:

- Past the SOL but still on your credit report — Collector can't sue, but the damage to your score continues

- Still within the SOL but falling off your report soon — Collector can still sue, but the credit damage is almost over

- Past both deadlines — Collector can't sue AND the item should be gone from your report

If a debt is time-barred but still showing on your credit report, you have options. Under the FCRA, every item on your report must be verifiable. If the original creditor can't produce documentation — which gets harder as years pass — the bureaus are required to remove it. That's where strategic credit report disputes come in.

What Debt Collectors Can and Can't Do With Old Debt

The Fair Debt Collection Practices Act (FDCPA) and its implementing regulation, Regulation F, set clear rules:

Collectors CANNOT:

- Sue you or threaten to sue you on time-barred debt (per the CFPB's 2023 advisory opinion under Regulation F)

- Misrepresent the legal status of a debt

- Imply legal consequences they can't actually pursue

Collectors CAN:

- Continue calling and sending letters requesting payment

- Report the debt to credit bureaus (within the 7-year FCRA window)

- Offer settlement deals

- Sell the debt to another collector

If a collector threatens to sue on a debt you know is time-barred, that's an FDCPA violation. You can report them to the CFPB and your state attorney general, and you may have grounds for a lawsuit of your own.

What Happens If You Get Sued on Time-Barred Debt?

It happens more often than it should. A collector files a lawsuit hoping you won't show up. And honestly? Most people don't. The FTC estimates that over 90% of debt collection lawsuits end in default judgments — meaning the consumer never responded.

If you get sued on a debt you believe is time-barred:

- Do NOT ignore the lawsuit. If you don't respond, the court enters a default judgment against you — even if the debt was time-barred. The judge doesn't check for you.

- Show up and raise the SOL defense. Bring documentation showing the date of your last payment. If the SOL has expired, the case should be dismissed.

- Consult a consumer attorney. Many FDCPA attorneys work on contingency (they get paid from the settlement if you win). Filing suit on time-barred debt is itself a violation of the FDCPA.

A judgment against you opens the door to wage garnishment, bank account levies, and property liens. These can last 10-20 years depending on your state and can be renewed. That's why showing up matters — even for old debt.

Medical Debt and the Statute of Limitations

Medical debt follows the same SOL rules as other debt types, but there have been major changes recently that work in consumers' favor:

- Medical debt under $500 no longer appears on credit reports as of 2023, per the three major bureaus' policy change

- Paid medical collections are removed from credit reports — they used to linger for years after payment

- Medical debt typically falls under "written contract" SOL timelines, which are often longer than credit card SOLs

If you have old medical debt on your credit report, check whether it's under the $500 threshold or already paid. If so, it shouldn't be there at all, and you can dispute it for removal.

Which State's Law Applies If You've Moved?

This gets tricky. Three possibilities:

- The state where you lived when you opened the account — some credit agreements have a "choice of venue" clause specifying this

- The state where you currently live — some courts apply the debtor's current state of residence

- The state specified in the credit agreement — many credit card contracts specify a particular state (often one with a longer SOL, like Delaware or Virginia)

Credit card companies often write contracts with favorable-to-them venue clauses. Read the fine print on any old agreements. If you've moved from a state with a long SOL to one with a short SOL (or vice versa), the answer might not be straightforward — and a consumer lawyer can help you figure it out.

Expired Debt Still Hurting Your Credit? Here's What to Do

If a debt is past the statute of limitations but still sitting on your credit report, you're in a strong position. Here's the play:

- Pull your credit reports from all three bureaus at AnnualCreditReport.com

- Identify time-barred debts — check the "date of first delinquency" and your state's SOL

- Do NOT contact the collector directly — you don't want to accidentally restart the clock or acknowledge the debt

- File disputes with the credit bureaus under the FCRA — request verification of the debt. Old debts are harder for collectors to verify, and if they can't, the bureau must remove the item.

- If the debt is also past the 7-year FCRA reporting period, dispute it as obsolete. Bureaus are required to remove items that have exceeded the reporting timeline.

For debts that are time-barred but still within the 7-year reporting window, strategic disputes through the FCRA verification process can still get them removed. Under federal law, the creditor or collector must be able to verify every item they report. If the original creditor sold the debt years ago and records have changed hands multiple times, verification often fails.

This is exactly the kind of situation where working with a professional credit repair company makes sense. At Crowned Credit, we handle disputes strategically using your rights under the FCRA — and old, hard-to-verify debts are some of the easiest items to get removed. If you're dealing with time-barred debt dragging your score down, book a free consultation and we'll review your reports.

5 Mistakes People Make With Old Debt

- Making a small payment to "get them off your back." This can restart the SOL clock and give the collector years of new legal leverage. Never pay without understanding the consequences.

- Ignoring a lawsuit. Even if the debt is time-barred, failing to show up in court means an automatic judgment against you. You have to raise the defense yourself.

- Confusing SOL with credit reporting. Your debt can expire legally while still tanking your credit score. They're two different timelines.

- Believing collectors who say you "have to" pay. If the debt is time-barred, you have zero legal obligation to pay. They're counting on you not knowing that.

- Not checking old credit agreements. The venue clause in your original contract can determine which state's SOL applies — and that can change everything.

When Should You Actually Pay Old Debt?

Not every old debt should be ignored. Sometimes paying — or settling — makes strategic sense:

- You're applying for a mortgage. Mortgage underwriters often require collections to be paid or settled before approval, regardless of the SOL.

- The debt is within the SOL and the creditor is litigious. Some creditors (Capital One, Discover, and some medical systems) are known to sue aggressively. If you're within the SOL window, a settlement might be cheaper than a judgment.

- You can negotiate a pay-for-delete. Some collectors will agree to remove the item from your credit report in exchange for payment. Get that agreement in writing before paying. Our guide on pay-for-delete letters walks you through the process.

If you're unsure whether to pay, dispute, or wait it out, that's a judgment call that depends on your specific credit profile, your goals (buying a house? getting a car loan?), and the details of each account.

The Bottom Line

Knowing your state's statute of limitations gives you real leverage. Collectors make money from people who don't understand their rights — people who panic and send $50 on a 5-year-old credit card balance, accidentally resetting the legal clock. Don't be that person.

Check your state's SOL. Check the date of first delinquency on your credit report. And before you pay a dime on old debt, understand exactly what you're doing and what it could trigger.

If old debts are still sitting on your credit report and hurting your score, you don't have to wait for them to fall off on their own. Strategic disputes under the FCRA can often get them removed faster — especially when the debt is old and documentation is thin. Schedule a free credit consultation with Crowned Credit and let's figure out the fastest path to cleaning up your report.

Disclaimer: Crowned Credit is a credit repair organization. We do not guarantee specific credit score increases or timelines. Results vary based on individual credit history and the accuracy of information reported by creditors. Our services involve disputing items on your credit report using your rights under the Fair Credit Reporting Act (FCRA). This article is for educational purposes and is not legal advice. Consult an attorney for legal questions about debt collection in your state.