How Much Does a Voluntary Repossession Affect Your Credit?

Ashley Rivera

Credit Repair Specialist

How a Voluntary Repossession Affects Your Credit

Returning a car (or other financed item) to the lender because you can’t make payments is called a voluntary repossession. It feels like the responsible move — and in some ways it is. But make no mistake: it still hits your credit hard.

Here’s exactly what happens to your credit score, how long the damage lasts, and what you can do to recover.

What Is Voluntary Repossession?

Voluntary repossession means you proactively return the financed item (usually a vehicle) to the lender because you can no longer afford the payments. The lender sells it, and if the sale doesn’t cover what you owe, you’re responsible for the remaining balance — called a deficiency balance.

The main difference from involuntary repossession: you avoid the surprise of a tow truck showing up. That’s about it. From a credit reporting standpoint, both types carry similar weight.

Credit Score Impact

How Much Will Your Score Drop?

A voluntary repossession can drop your score by 100 to 150+ points, depending on where you started. Someone with a 750 score will feel a bigger point drop than someone already at 580.

How Long Does It Stay on Your Report?

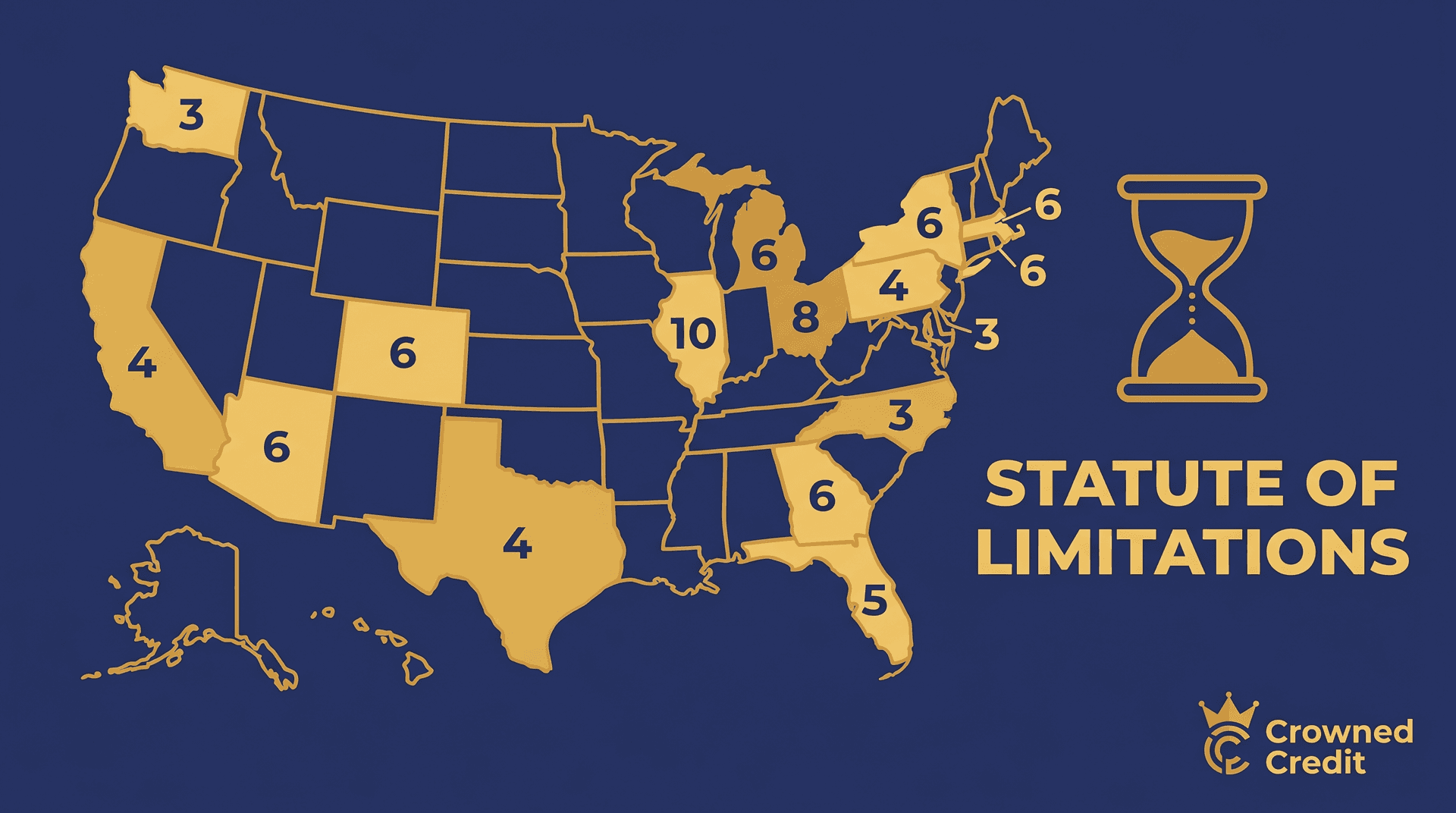

Seven years from the date of the first missed payment that led to the repossession. The impact is worst in the first two years and gradually fades after that.

The Double Hit Problem

If the lender sells your vehicle for less than you owe and sends the deficiency balance to collections, you end up with two negative items on your report — the repossession itself and a collection account. That compounds the damage significantly.

Voluntary vs. Involuntary: Does It Matter?

Lenders and credit bureaus treat both similarly. Some lenders may view voluntary repossession slightly more favorably in a manual review because it shows you took initiative. But on a credit report, both are recorded as repossessions and both damage your score.

Steps to Recover After a Voluntary Repossession

1. Check Your Credit Report for Errors

Pull your reports from all three bureaus at AnnualCreditReport.com. Look for incorrect dates, wrong balances, or accounts that don’t reflect the voluntary nature of the return. Errors are common — and disputable under the FCRA.

2. Handle the Deficiency Balance

If you owe a remaining balance, don’t ignore it. Contact the lender to negotiate a payment plan or settlement. If it goes to collections, try to negotiate a pay-for-delete agreement before paying.

3. Start Rebuilding Your Credit

- Open a secured credit card — use it for small purchases, pay in full each month

- Keep all other bills current — one missed payment can undo months of progress

- Keep utilization under 30% — ideally under 10%

- Consider a credit builder loan — adds positive installment history

4. Dispute Inaccurate Reporting

If anything about the repossession on your credit report is wrong — the date, the balance, the account status — dispute it. Under the FCRA, bureaus have 30 days to investigate, and anything they can’t verify must be removed.

Alternatives to Consider Before a Voluntary Repossession

- Talk to your lender first. Many offer hardship programs, payment deferrals, or loan modifications.

- Refinance. A lower monthly payment might make the loan manageable.

- Sell the vehicle privately. You’ll likely get more than the lender would at auction, potentially covering the full loan balance.

Need Help With a Repossession on Your Report?

If a voluntary repossession is dragging your credit score down, Crowned Credit can review your report, identify errors or disputable items, and work to get them removed.

Disclaimer: Results vary by individual. Credit repair timelines depend on your unique credit history and the nature of the items being disputed. Crowned Credit cannot guarantee specific results or timeframes.