What Happens to Your Credit When You Die? (2026 Guide)

Ashley Rivera

Credit Repair Specialist

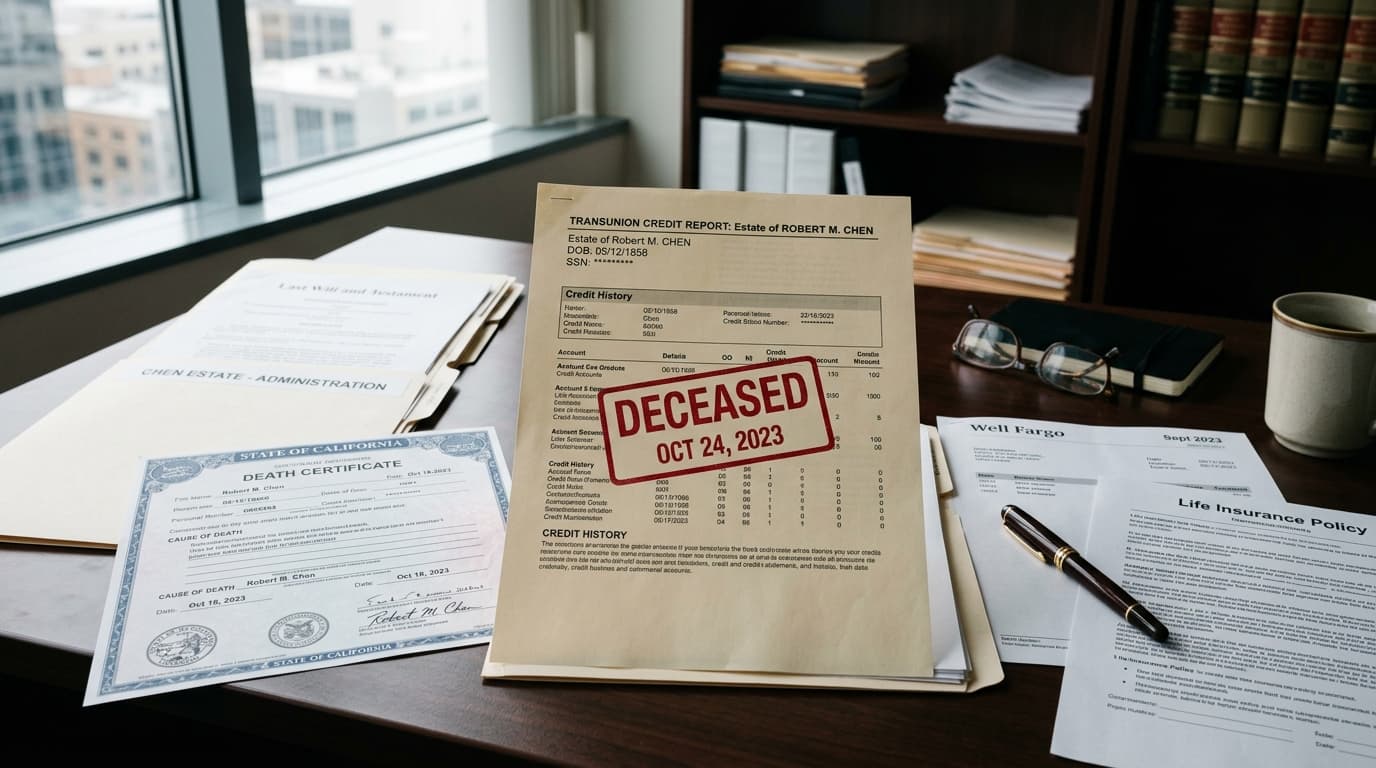

Your credit file doesn't follow you to the grave. Once you die, the three major credit bureaus (Equifax, Experian, and TransUnion) mark your report as "deceased" and eventually close it entirely. But your debt? That's a different story.

Contrary to popular belief, death doesn't wipe the slate clean. Creditors still expect payment, and your estate—the legal term for everything you own at death—is typically responsible for settling outstanding balances before anything goes to your heirs.

If you're planning your estate or recently lost a loved one, understanding how credit and debt work after death can save your family thousands of dollars and prevent unnecessary legal headaches. Here's everything you need to know.

How Credit Bureaus Handle Death

When someone dies, credit bureaus don't automatically know. Someone has to tell them. Usually, that's the estate executor, a family member, or the Social Security Administration (which shares death data with the bureaus).

Once notified, the credit bureau adds a "deceased alert" to the credit file. This prevents identity thieves from opening new accounts in the deceased person's name—a real problem affecting thousands of families each year.

The credit file stays in the system temporarily to resolve existing accounts, but it stops updating. Creditors can still view it during estate settlement, but no new activity should appear.

After the estate is closed and all debts are resolved, the credit file is eventually deleted. Timeline varies by bureau, but most files disappear within two to three years after death.

What Happens to Credit Card Debt After Death?

Credit card debt doesn't disappear when you die. The credit card company becomes a creditor of your estate, and your estate executor must use available assets—bank accounts, property, investments—to pay it off.

Here's the order of priority: secured debts like mortgages come first, then unsecured debts like credit cards. If the estate doesn't have enough money to cover everything, creditors may receive partial payment or nothing at all.

Important: Your family members are NOT automatically responsible for your credit card debt just because they're related to you. Debt responsibility depends entirely on the legal relationship to the account.

Who Is Actually Responsible for a Deceased Person's Debt?

This is where things get specific. Debt responsibility after death falls into a few clear categories:

1. The Estate (Most Common)

The estate pays most debts. If you die with $10,000 in credit card debt and $30,000 in the bank, the executor withdraws $10,000 from your account and pays the credit card company. Your heirs get what's left.

If the estate has zero assets—no house, no savings, nothing—creditors can't collect. They can file claims with the estate, but if there's no money, there's no money. The debt dies with you.

2. Joint Account Holders

If you have a joint credit card (not just an authorized user—more on that below), the joint account holder owes 100% of the balance. Joint accounts mean both people own the debt equally.

Example: You and your spouse have a joint Chase credit card with a $5,000 balance. You die. Your spouse now owes the full $5,000, regardless of who made the charges.

3. Co-Signers

If you co-signed a loan for someone—a car loan, student loan, personal loan—you're legally responsible for the debt if the primary borrower dies. The lender will come after you for the full balance.

Co-signers get zero benefits from the loan but 100% of the liability. That's why financial experts warn against co-signing unless you're prepared to pay the loan yourself.

4. Community Property States

Nine states follow community property laws: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

In these states, spouses may be responsible for debts incurred during the marriage, even if only one spouse's name is on the account. The rules vary by state, so consult a local attorney if you're in one of these areas.

5. Authorized Users (Usually Not Responsible)

If you're an authorized user on someone else's credit card, you can use the card but you don't own the debt. When the primary cardholder dies, the estate owes the balance—not you.

The credit card company may freeze or close the account, and the authorized user's credit report might show the account closure, but authorized users can't be forced to pay the debt.

There's one exception: some issuers allow authorized users to convert the account into their own name, taking on the balance voluntarily. Never do this without understanding the full debt amount.

What Happens to Mortgages, Car Loans, and Student Loans?

Mortgages

If someone inherits a house with a mortgage, they also inherit the monthly payment obligation. Federal law (Garn-St. Germain Act) prevents lenders from demanding immediate full repayment when the borrower dies, as long as the heir keeps making payments.

If the heir can't afford the mortgage, options include:

- Selling the house and using proceeds to pay off the loan

- Refinancing the mortgage in their own name (requires qualifying)

- Letting the lender foreclose (damages the heir's credit if they formally assumed the loan)

If no one wants the house, the estate can let it go into foreclosure without affecting heirs' credit, assuming they never officially took ownership.

Car Loans

Car loans work similarly. The estate owes the balance. If someone inherits the car, they inherit the loan. If they stop paying, the lender repossesses the vehicle.

Pro tip: If the car is worth less than the loan balance (upside down), the heir can surrender the car to the lender and walk away. The estate owes any deficiency balance, not the heir personally.

Federal Student Loans

Federal student loans are discharged upon death. If you die with $50,000 in federal student loans, the debt disappears. The estate doesn't owe it, and neither do your parents, spouse, or kids.

The executor must provide a death certificate to the loan servicer, who then cancels the debt.

Private Student Loans

Private student loans vary by lender. Some discharge the loan upon death. Others treat it like any other debt and demand payment from the estate.

If a parent co-signed a private student loan and the student dies, the parent still owes the full balance unless the lender offers death discharge as a policy (some do, most don't).

How Debt Collection Works After Death

Creditors have a limited time window to file claims against an estate, usually six months to a year depending on state law. This period is called the "statute of limitations for creditor claims."

If a creditor misses the deadline, they lose the right to collect. That's why estate executors should formally notify creditors and publish a notice of death in local newspapers—it starts the clock.

Debt collectors may contact family members trying to locate the executor or find estate assets. They're allowed to do that. But they're NOT allowed to mislead family members into thinking they personally owe the debt.

If a debt collector tells you "You have to pay your father's credit card bill" when you're not legally responsible, that's a violation of the Fair Debt Collection Practices Act (FDCPA). Report it to the Consumer Financial Protection Bureau immediately.

How to Notify Credit Bureaus of a Death

To protect the deceased's identity and prevent fraud, notify all three credit bureaus as soon as possible. You'll need:

- A certified copy of the death certificate

- Your identification (as executor or next of kin)

- Proof of authority (executor documents or probate paperwork)

Mail the documents to:

Equifax:

Equifax Information Services LLC

P.O. Box 740256

Atlanta, GA 30374

Experian:

Experian

P.O. Box 4500

Allen, TX 75013

TransUnion:

TransUnion LLC

P.O. Box 2000

Chester, PA 19016

Each bureau adds a deceased alert within a few weeks. This prevents new credit applications in the deceased's name, which is critical for stopping identity theft.

Can Debt Hurt Your Living Family's Credit?

Only if they're legally responsible for the debt. If you're not a joint account holder, co-signer, or spouse in a community property state, a deceased family member's debt cannot appear on your credit report or damage your credit score.

However, here are scenarios where confusion happens:

- Authorized user accounts: If you were an authorized user on a deceased person's credit card, the account may show "closed" on your credit report. That's normal. It doesn't hurt your score unless the account had a negative payment history before death.

- Jointly owned assets: If you jointly own a house or car and the deceased stopped making payments before death, late payments can hit your credit report because you're an owner.

- Mistakes by creditors: Sometimes creditors mistakenly try to collect from family members or report debts on the wrong person's credit report. Dispute these errors immediately with the credit bureaus.

What If the Estate Can't Pay All the Debts?

If debts exceed assets, the estate is "insolvent." In that case, state law determines the payment order. Secured creditors (mortgages, car loans) typically get paid first, followed by funeral expenses, taxes, and then unsecured creditors like credit card companies.

If there's not enough money, some creditors get nothing. They can't force heirs to pay from their own pockets (again, unless the heir is a joint account holder or co-signer).

Creditors may try to guilt family members into "doing the right thing" and paying voluntarily. Don't. If you're not legally responsible, paying a deceased person's debt uses your money to settle someone else's obligation—and it doesn't improve your credit score or theirs.

Planning Ahead: Protecting Your Family From Your Debt

The best way to protect your loved ones is to minimize debt before you die and ensure they understand what they're—and aren't—responsible for.

Steps You Can Take Now:

- Pay down debt aggressively. The less you owe, the less your estate has to settle. If you have collections, charge-offs, or high credit card balances, credit repair services can help you clean up your credit and reduce outstanding balances.

- Avoid joint accounts unless necessary. Joint accounts create shared liability. If you want to give someone access to your credit card, make them an authorized user instead—they get the convenience without the legal responsibility.

- Never co-sign loans. Co-signing puts you on the hook if the borrower dies or defaults. If you must help someone get a loan, consider gifting them the down payment instead.

- Buy life insurance. A term life insurance policy can pay off your debts and leave money for your family. Premiums are cheap if you're young and healthy. The payout goes directly to your beneficiaries, bypassing the estate and creditors.

- Create a will. A clear will speeds up the estate process and ensures debts are paid in the correct order. Without a will, state law decides, and it may not match your wishes.

- Tell someone where your accounts are. Your executor can't pay creditors if they don't know the accounts exist. Keep a list of all credit cards, loans, and accounts in a secure place and tell a trusted person where to find it.

What to Do If You're Dealing With a Loved One's Debt

If you're the executor or family member handling a deceased person's estate, here's your action plan:

- Get multiple copies of the death certificate. You'll need them for creditors, banks, and credit bureaus. Order at least 10 certified copies.

- Locate all accounts and debts. Check mail, email, and credit reports to find every creditor. You can request a credit report for the deceased by mailing the credit bureaus with proof of death and your authority.

- Notify creditors and credit bureaus. Send written notices with death certificates. This stops interest from accruing on some accounts and starts the creditor claim period.

- Don't pay debts from your own pocket. Use estate assets only. If the estate runs out of money, creditors are out of luck. Don't let them pressure you into paying personally.

- Consult an estate attorney if the estate is complicated. If there's significant debt, multiple creditors, or disputes over who owes what, hire a lawyer. It's worth the cost to avoid legal mistakes.

- Watch for identity theft. Monitor the deceased's credit report for six months after death. Fraudsters target deceased individuals because family members often don't check.

Common Myths About Credit and Death

Myth: All debt disappears when you die.

Reality: Only federal student loans are automatically discharged. Everything else goes to the estate.

Myth: Family members inherit your debt.

Reality: Only if they're joint account holders, co-signers, or in certain community property state situations.

Myth: Creditors can take your inheritance.

Reality: Only if the inheritance flows through the estate. Life insurance and retirement accounts with named beneficiaries bypass the estate and go directly to heirs, untouched by creditors.

Myth: You have to pay your parents' debt to honor their memory.

Reality: No moral or legal obligation exists unless you're legally liable. Creditors use guilt as a tactic. Don't fall for it.

The Bottom Line

Death changes your credit file status, but it doesn't erase financial obligations. Estates settle debts using available assets, and only people with legal liability—joint account holders, co-signers, and some spouses—pay from their own pockets.

If you're managing a loved one's estate, don't let creditors intimidate you into paying debts you don't legally owe. Get organized, notify the right parties, and follow the legal process. If you're planning your own estate, reduce debt now and protect your family with life insurance and clear documentation.

And if you're dealing with negative items on your own credit report—late payments, collections, charge-offs—cleaning up your credit before a major life event like estate planning ensures your family inherits financial clarity, not financial chaos.

Need help repairing your credit? Crowned Credit specializes in removing inaccurate, unfair, and unverifiable negative items from credit reports. Our team disputes errors with all three bureaus, helps you build positive credit history, and guides you toward financial goals like home ownership, better loans, and lower insurance rates. Schedule your free consultation or call us at 336-310-0090. We offer three flexible plans starting at $150 enrollment + $99/month for our Essential package.

Disclaimer: Results vary by individual. Crowned Credit cannot guarantee specific credit score increases or specific negative item removals. We dispute inaccurate, unfair, or unverifiable information under your rights provided by the Fair Credit Reporting Act (FCRA). This article is for informational purposes only and does not constitute legal, financial, or estate planning advice. Consult a licensed attorney or financial advisor for guidance specific to your situation.