How Long Does an Eviction Stay on Your Record?

Ashley Rivera

Credit Repair Specialist

What Is an Eviction Record?

Eviction is the formal removal of a tenant from a rental property. It happens in most cases due to not paying rent or lease violations. This process involves a court order, which acts as a complete legal record of the event.

Eviction does not only result in a tenant losing their home — its impact can go beyond that. Most landlords run background checks before renting their property, and if an eviction shows on your record it could become a significant hurdle to finding new housing. It can also lower your credit score.

For many, an eviction can shake their stable life. So it is necessary to understand how long these eviction records remain visible. Credit bureaus keep these records for up to seven years, while courts can keep them for even longer.

Where Are Eviction Records Kept?

Eviction is documented in several official records. When the process is initiated, court filings and other legal documents are created and stored. If the reasons include unpaid rent or damages, those debts are also reported to credit bureaus and can ultimately appear on your credit report.

All of this data is stored in public court records, where it is easily accessible. Credit agencies also record financial liabilities for their credit reports. Together, these sources make eviction records visible across different platforms:

- Public court records — accessible to landlords and background check services

- Credit bureau reports — if unpaid debts were sent to collections

- Tenant screening databases — used by property management companies

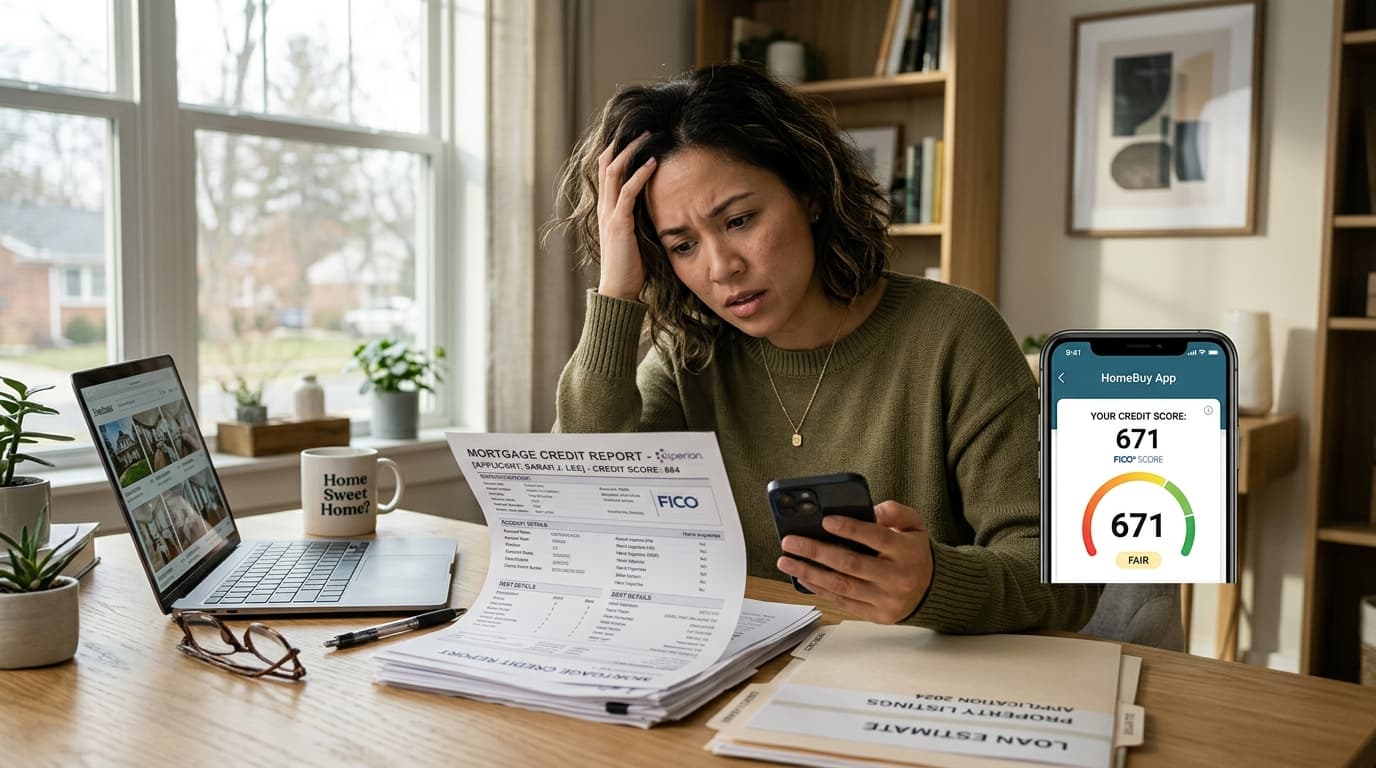

How Long Does an Eviction Stay on Your Credit Report?

The most common timeframe is seven years. An eviction-related collection or judgment can appear on your credit report for up to seven years from the date of first delinquency. However, the exact duration depends on jurisdiction.

- Some states allow eviction records to remain in public courts indefinitely

- Other states impose limits on how long records can be accessed

- Credit bureau reporting is generally capped at seven years under federal law

Being aware of your local laws is important when assessing your specific situation.

Can You Remove an Eviction From Your Record?

Dispute Errors in the Record

The first option is to dispute errors in eviction records, which can open up housing opportunities for tenants. Gather all relevant documentation to pinpoint inaccuracies. Credit bureaus are legally required to investigate disputes and correct mistakes within 30 days.

If the issue lies in court records, the tenant will need to file a correction request with the court. Acting quickly ensures your records accurately represent your rental history.

Negotiate With the Landlord or Debt Collectors

Tenants can also negotiate with landlords or debt collectors to address their credit reports. Start by explaining your situation honestly and offering reasonable proposals. If possible, request that the eviction record be removed or marked as resolved upon payment.

Showing good faith and willingness to cooperate can make negotiations more productive. Always get any agreements in writing before making any payment.

Steps to Rebuild After an Eviction

Improve Your Credit Score

Improving your credit score can minimize issues with future landlords and is a key step to recovering after an eviction. Prioritize paying your bills and debts on time to boost your score over time.

Avoid Legal Disputes

Avoid legal disputes with landlords going forward. Maintain clear communication, adhere strictly to your lease agreement, and document everything in writing.

Work With Reputable Agencies

Use reputable credit repair and financial guidance services to help restore your rental history and overall financial standing. A professional team can help identify errors, dispute inaccurate items, and build a stronger credit profile.

Conclusion

An eviction doesn’t mean the end of your housing prospects or your financial future — recovery is always possible. Take time to understand the process and all available paths forward. Improving your credit score and building positive relationships with landlords and debt collectors is the key.

With the right support, you can overcome these challenges and find stable housing again.

Disclaimer: Results vary by individual. Credit repair timelines depend on your unique credit history and the nature of the items being disputed. Crowned Credit cannot guarantee specific results or timeframes.