Does Late Rent Affect Your Credit Score in 2026?

Ashley Rivera

Credit Repair Specialist

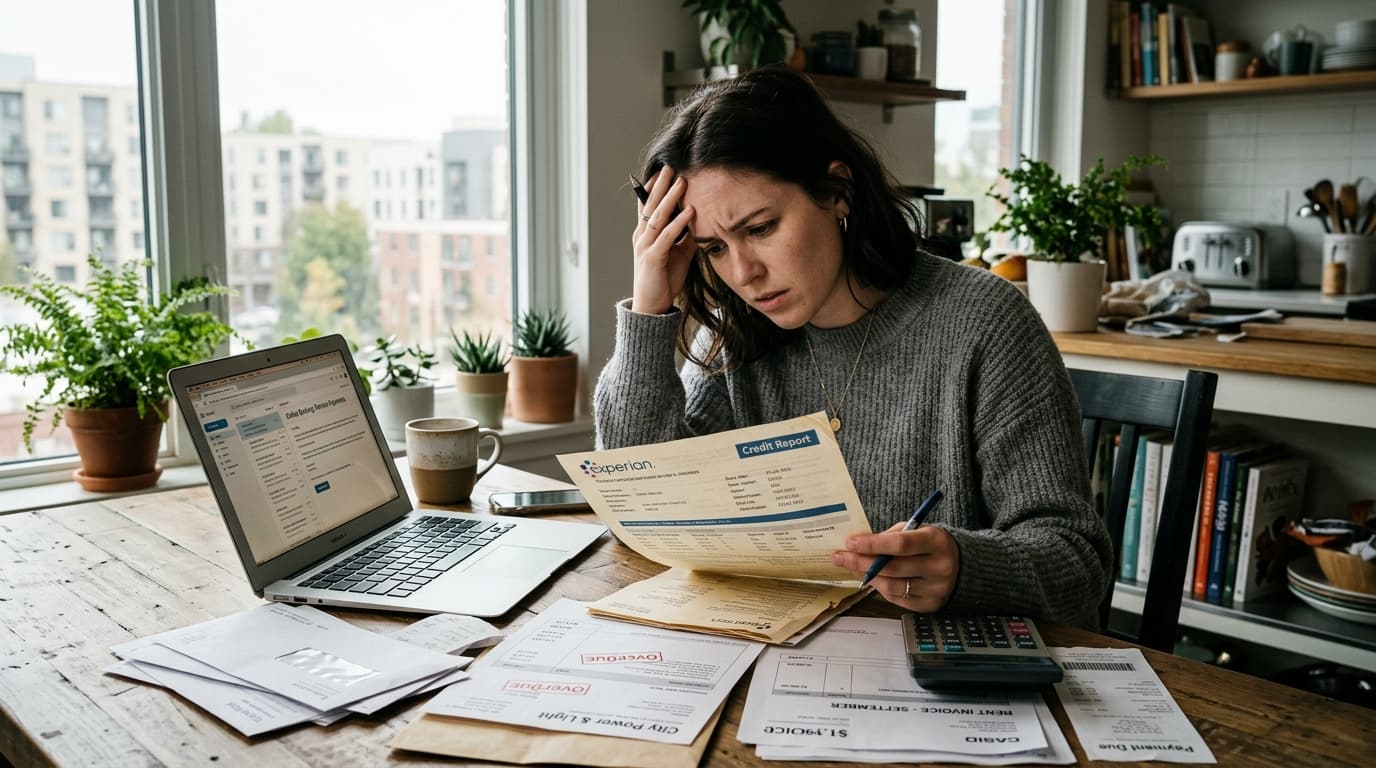

You can miss a credit card payment and know exactly what kind of trouble is coming. Rent feels different. A lot of people assume it stays between them and the landlord.

That assumption gets expensive.

Late rent can affect your credit score in 2026, but usually not in the simple way people think. Some landlords do not report monthly rent at all. Others use rent-reporting software. And even when late rent is not reported immediately, an unpaid balance can still end up in collections, which is where real damage often starts.

If you are behind right now, or worried an old apartment balance is about to hit your report, this guide will show you what actually happens, how long the damage can last, and what you can do about it. If your file already has multiple negative items stacked together, Crowned Credit can help you map out the next steps through a consultation.

Does Late Rent Show Up on Your Credit Report?

Yes, it can.

The Consumer Financial Protection Bureau says the big three credit bureaus, Experian, Equifax, and TransUnion, use rental payment and related debt collection information in credit reports, though the way they handle it can vary. That means rent is no longer some invisible bill that never touches your profile.

There are a few common ways late rent reaches your credit file:

- Your landlord or property manager reports it directly through a rent-reporting service or payment platform

- Your unpaid balance gets sent to collections, and the collection agency reports the debt

- A specialty consumer reporting agency records the issue, which can affect future rental applications even if the major bureaus do not show the same data the same way

That last part matters more than people realize. Even if a missed rent payment does not immediately crush your FICO score, it can still make getting your next apartment harder.

Will One Late Rent Payment Hurt Your Score Right Away?

Not always.

If your landlord is an individual owner who takes checks and does not use any credit-reporting system, a rent payment that is a few days late may never hit your reports. You may still get charged a late fee, and you may still violate the lease, but that is different from formal credit reporting.

On the other hand, if your property manager uses a platform that reports rent activity, the risk changes fast. Experian notes that a landlord or rent payment service may report a delinquent payment once it is 30 or more days past due. If the debt sits longer and goes to collections, the damage can be even worse.

So the honest answer is this:

- A few days late: may cause lease problems and fees, but may not hit your credit

- 30 or more days late: has a much higher chance of being reported, depending on the landlord’s system

- Unpaid and sent to collections: very real risk of credit damage

If you are trying to keep your housing options open, do not wait around hoping the landlord is too busy to act. That is a weak plan.

How Unpaid Rent Usually Hurts Your Credit

The damage usually happens in one of two ways.

1. Direct rental reporting

Some landlords and property managers report rent payment history through third-party systems. That can work in your favor when you pay on time, but it can also work against you when you do not.

2. Collections

This is the more common problem. If you move out owing rent, break a lease, or stop paying and the balance remains unresolved, the landlord may place or sell the debt to a collection agency. Once a collection account lands on your reports, lenders and apartment screeners take notice.

That means late rent can turn into a double problem:

- You owe the apartment complex or landlord money

- Your credit profile now shows a serious negative item tied to unpaid housing debt

If your report already has other derogatory items, read what to do about collections on your credit report and how charge-offs are handled. The strategy depends on the full file, not just one account.

How Much Can Late Rent Drop Your Credit Score?

There is no honest universal number.

Anyone promising that late rent drops every score by 75 points or 110 points is guessing. Credit score impact depends on things like:

- Whether the rent was reported as a late payment or as a collection

- How recent the negative item is

- What your score looked like before the damage

- How many other derogatory marks are already on the report

For example, somebody with one clean credit card and no negatives may feel a fresh collection much harder than somebody whose report already has charge-offs, maxed-out cards, and old late payments.

The better question is not “exactly how many points will I lose?” The better question is “what will this do to approvals, rates, and my ability to rent again?” That is where the pain usually shows up first.

Can Late Rent Keep You From Renting Another Apartment?

Absolutely.

Even when a future landlord does not care much about your credit card balances, they care a lot about whether you paid your last landlord. That is why rental debt is so dangerous. It hits the exact issue the next property manager is screening for.

You could run into trouble with:

- Apartment applications

- Security deposit requirements

- Cosigner demands

- Higher scrutiny from leasing offices

- Flat denials from properties that screen for prior rental debt

If you are already apartment hunting, also read what credit score landlords often look for when renting and how long an eviction can stay on your record. Rent problems rarely travel alone.

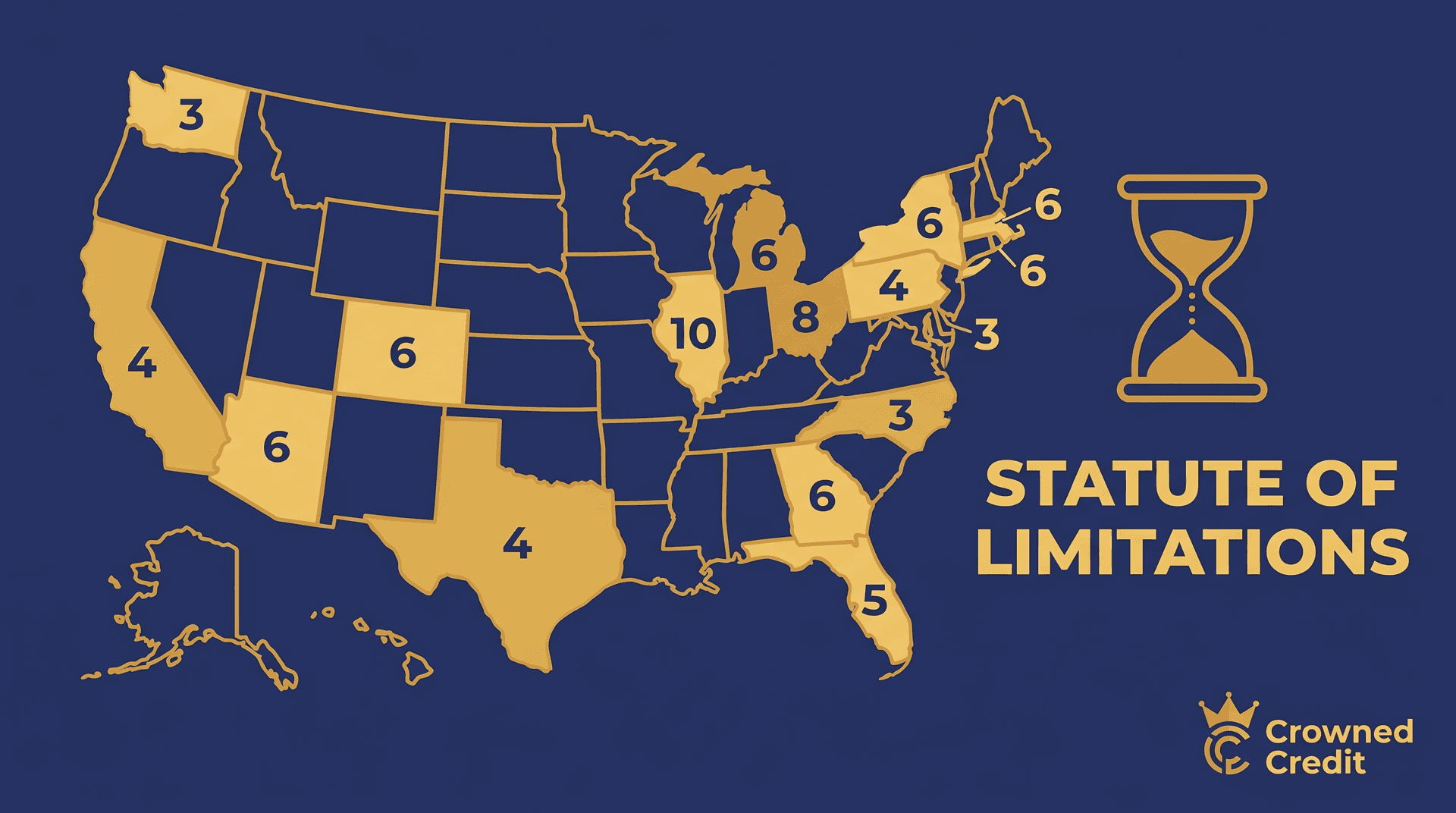

How Long Does Unpaid Rent Stay on Your Credit Report?

In many cases, a related negative item can stay on your credit report for up to seven years.

Experian explains that late payments and collection accounts tied to unpaid rent may remain for up to seven years. That timeline is why people get blindsided. They think, “I moved out, paid the balance later, so this should be over.” Sometimes the balance gets resolved, but the reporting history still has its own clock.

Paying the debt can still matter. It may:

- Stop the collection from getting worse

- Update the status of the account

- Look better to a manual underwriter than an unpaid balance

But it does not automatically mean the account disappears overnight.

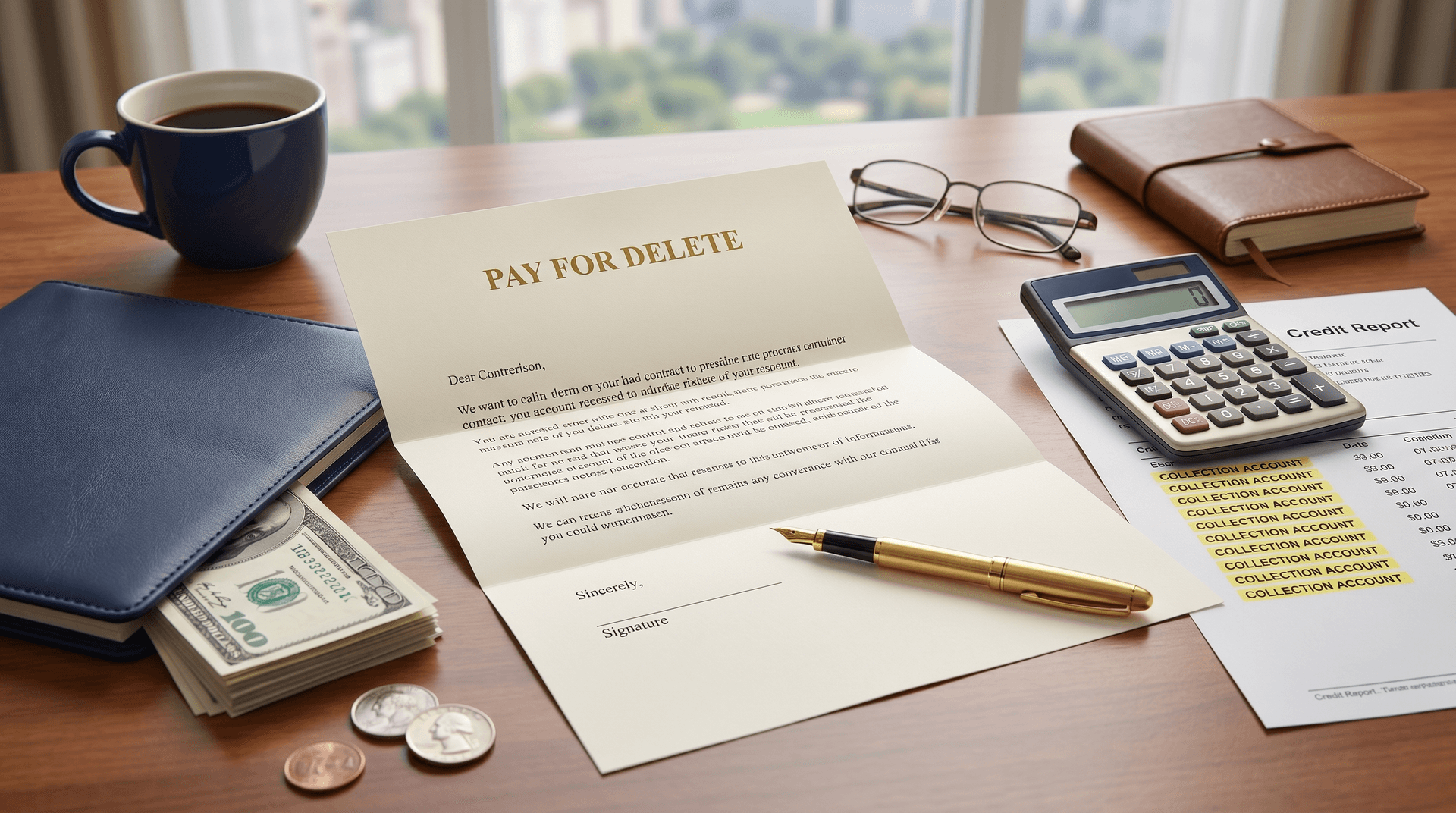

What If the Late Rent or Rental Collection Is Wrong?

Then you need to challenge it, and you need to do it with documents, not emotion.

Rental reporting can be wrong for the same reasons other accounts can be wrong. The amount may be off. The move-out charges may be inflated. The dates may be wrong. A debt may be duplicated. A landlord may claim you owed more than the lease or ledger supports.

If that happens, take these steps:

- Pull your reports from AnnualCreditReport.com

- Get your lease, ledger, payment receipts, move-out statement, and any emails with the landlord

- Compare the reported balance, dates, and account status against your records

- Dispute inaccurate reporting with the credit bureau showing it

- Challenge the furnisher or collection agency if their reporting is incomplete, inaccurate, or not properly verified

Under the Fair Credit Reporting Act, furnishers and bureaus have to handle consumer reporting with proper accuracy and verification standards. If you need a deeper breakdown, start with what the FCRA is, common credit report errors, and how credit disputes work.

And no, this does not mean you should only act when you are 100 percent sure the account is fake. Negative items still have to be properly verified and accurately reported. That is the whole point.

What Should You Do if You Cannot Pay Rent on Time?

Move early.

The worst move is silence. If you know rent is going to be late, talk to the landlord or property manager before the situation hardens into notices, fees, and collections placement.

Here is the practical order of operations:

- Contact the landlord quickly and ask what options exist

- Get every agreement in writing, including partial payment plans or extensions

- Ask whether they report rent to the credit bureaus or use a collections partner

- Track all payments so you can prove what was paid and when

- Check your credit reports if the account becomes seriously delinquent or gets transferred

If you wait until after you move out and a collector starts calling, your leverage is usually worse.

Can On-Time Rent Help Your Credit Too?

Sometimes, yes.

The CFPB notes that positive rental payments can help build credit when they are reported through a rent-reporting program. The key issue is that most renters do not get that benefit automatically. It depends on the landlord, the payment platform, and which bureau receives the data.

That means rent is unlike a credit card. With a credit card, on-time payments usually show up because the account is built for credit reporting. With rent, positive history often requires a specific reporting setup.

If building credit is your bigger goal, do not rely only on rent. Pair it with actual credit-building tools like secured credit cards, credit builder loans, and low utilization on revolving accounts. We also covered whether utility bills build credit if you are looking at other nontraditional ways to strengthen a thin file.

When Does Professional Help Make Sense?

If you have one small landlord dispute and clean paperwork, you may be able to handle it yourself.

But professional help makes more sense when:

- You have a rental collection plus other negative items

- You need to qualify for a mortgage, car loan, or apartment soon

- The balance, dates, or account status are being reported inconsistently

- You are not sure whether to negotiate, dispute, rebuild, or do all three

Crowned Credit works with people whose reports usually are not dealing with just one issue. It might be rental debt, plus late payments, plus collections, plus utilization problems. That is where a structured plan matters more than random internet advice.

You can review Crowned Credit’s options on the pricing page:

- Essential: $150 setup + $99/month

- Accelerated: $249 setup + $199/month

- Momentum: $1,095 one-time

If you want someone to review the full file with you, book a consultation or call 336-310-0090.

FAQ: Late Rent and Credit Scores

Does late rent always hurt your credit?

No. Some landlords do not report rent at all. But late rent can hurt your credit if it is reported directly or turned over to collections.

Can one missed month of rent go to collections?

It can, especially if the balance remains unpaid and the landlord decides to pursue it. The timeline depends on the landlord, lease, and collection practices.

Does paying rental debt remove it from your report?

Not automatically. Paying can update the status and stop the problem from getting worse, but negative reporting may still remain for its normal reporting period.

Can you dispute unpaid rent on your credit report?

Yes, if the account is inaccurate, duplicated, outdated, or not properly verified. The strength of the dispute depends on the records.

*Credit repair results vary by individual. Crowned Credit disputes negative items using consumer rights under federal law, including the Fair Credit Reporting Act. We do not guarantee specific credit score increases, timelines, or removal outcomes. The Credit Repair Organizations Act requires this disclosure.*

Final Answer

Yes, late rent can affect your credit score in 2026, especially when the account is reported by a landlord, payment platform, or collection agency. It may not show up the second you miss the due date, but unpaid rent is absolutely capable of damaging both your credit and your ability to rent again.

If this is happening to you, do not guess your way through it. Check the reports, gather the paperwork, figure out whether the reporting is accurate, and act before the damage spreads.

Book a consultation with Crowned Credit if you want help reviewing rental debt, challenging negative reporting strategically, and building a smarter recovery plan.