How to Repair Your Credit After Divorce in 2026: A Complete Recovery Guide

Ashley Rivera

Credit Repair Specialist

The divorce is final. The papers are signed. But when you pull your credit report, you realize the financial fallout is just getting started.

Maybe your ex stopped paying on a joint car loan three months ago and collections are calling you. Maybe a credit card you forgot about — one your spouse opened with you as a co-signer back in 2019 — is sitting at $14,000 with two missed payments. Maybe your score dropped 85 points and you can't even qualify for a decent apartment lease.

This is more common than you'd think. Credit industry surveys show that roughly 50 to 100 points of credit score damage is typical during and after a divorce. Not because the divorce itself hits your report — it doesn't — but because of all the financial chaos that comes with splitting a household.

The good news? Every single one of these problems has a solution. And if you move strategically, you can have your credit back on track within 6 to 12 months. Here's the playbook.

Why Divorce Damages Your Credit (Even When You Did Nothing Wrong)

First, a critical fact: divorce proceedings themselves don't appear on your credit report. Experian, Equifax, and TransUnion don't track marital status. The credit bureaus don't care whether you're married, separated, or single.

So why does your score tank?

Three reasons:

- Joint debts don't care about your divorce decree. A judge can order your ex to pay the mortgage or a credit card balance, but the original creditor doesn't have to honor that. If your name is on the account and your ex stops paying, you get the late payment on your report. The creditor signed a contract with both of you — the divorce court's ruling doesn't override that contract.

- Closed accounts reduce your available credit. When you close joint credit cards during the divorce — which you should — your total available credit drops. If you're still carrying balances on your individual cards, your credit utilization ratio spikes, and your score falls.

- Income drops while obligations stay the same. Going from a dual-income household to a single income makes it harder to keep up with payments. One missed payment on a mortgage or auto loan costs you 60 to 110 FICO points depending on where your score was before.

Step 1: Pull All Three Credit Reports and Know What You're Dealing With

Before you do anything else, go to AnnualCreditReport.com and pull your reports from Experian, Equifax, and TransUnion. You're entitled to free reports every 12 months under federal law — and through 2026, the bureaus are still offering free weekly access.

Print them out or save them as PDFs. Go through every single account and mark them in three categories:

- Individual accounts (yours only): These are your responsibility and nobody else's. Leave them alone unless there's an error.

- Joint accounts: Both names on the account. You're both legally responsible regardless of what the divorce decree says. Flag every one of these.

- Authorized user accounts: If you were added to your spouse's card as an authorized user, that card's history (good or bad) shows on your report. You can request removal at any time — the issuer will take you off the account, and the tradeline typically falls off your report within 30 days.

Pay special attention to late payments, collections, charge-offs, or any balances you don't recognize. Make a spreadsheet. You need to see the full picture before you start fixing things.

Step 2: Separate Joint Accounts Immediately

This is the single most important step, and it's the one most people delay too long.

Every joint account is a ticking time bomb. As long as your name is on a joint credit card or loan, your ex-spouse's financial behavior directly impacts your credit score. They max out the card? Your utilization goes up. They miss a payment? You get the ding. They file bankruptcy? The creditor comes after you for the full balance.

Here's how to handle each type:

Joint credit cards: Call the issuer and ask to close the account or remove one spouse. Most issuers won't remove a name from a joint account — they'll require you to close it and pay the balance. If you can't pay it off immediately, transfer the balance to an individual card if possible, then close the joint one.

Joint auto loans: Refinance into one person's name. If your ex is keeping the car but the loan is in both names, they need to refinance solo. If they can't qualify, this is a negotiation point — they may need to sell the car and pay off the loan.

Joint mortgage: Same concept. Refinance into one name, or sell the property. Until you do, both of you are on the hook. A divorce decree saying "he'll pay the mortgage" means nothing to your lender.

Authorized user accounts: Call the card issuer and request removal. This is straightforward — you don't need your ex's permission. If the account has negative history dragging your score down, removing yourself can give you an immediate score bump.

Step 3: Dispute Inaccurate Items From the Divorce Fallout

Here's where a lot of people leave money — and credit points — on the table.

After a divorce, it's extremely common for accounts to be reported inaccurately. Your ex may have paid a debt but the creditor still shows a balance on your report. A closed account might show as open. A joint account might be coded as individual. A collection agency might report a medical bill from your ex's hospital visit that was covered in the divorce.

Under the Fair Credit Reporting Act (FCRA), every item on your credit report must be verifiable by the furnisher. If you dispute an item and the creditor can't verify the information within 30 days, the bureau must remove it. This is a powerful tool — especially when original creditors have sold old debts to collectors who don't have the documentation to verify anything.

Common divorce-related items worth disputing:

- Late payments on accounts your ex was ordered to pay (if reporting is inaccurate)

- Accounts you were only an authorized user on that are still showing

- Balances that don't reflect payments made during the divorce

- Collections from debts assigned to your ex-spouse

- Accounts opened fraudulently by your ex using your information

- Incorrect account statuses (showing "open" when the account was closed)

For fraudulent accounts — credit cards your ex opened in your name without your knowledge — file an identity theft report at IdentityTheft.gov and dispute with all three bureaus. Under the FCRA, the bureaus must block fraudulent information from your report once you provide an identity theft report.

If the volume of disputed items feels overwhelming, or you're not sure how to write effective dispute letters, working with a professional credit repair company can save you months of back-and-forth with the bureaus. At Crowned Credit, we handle FCRA disputes strategically — challenging creditors to verify every negative item on your report and removing what they can't prove.

Step 4: Build Your Own Credit Identity

After a divorce, some people discover they barely have a credit history in their own name. Maybe everything was in their spouse's name. Maybe they were only authorized users, and once removed, their credit file is thin.

If that's you, here's how to build an individual credit profile quickly:

Open a secured credit card. Put down a $200 to $500 deposit, get a card with that limit, and use it for small purchases — gas, groceries, a streaming subscription. Pay the full statement balance every month. This builds payment history and establishes utilization in your own name. Cards from Discover and Capital One both report to all three bureaus.

Become an authorized user on a trusted person's account. If you have a parent or sibling with a long-standing credit card in good standing, ask them to add you as an authorized user. Their account history gets added to your report. You don't even need to use the card — just being on it helps your score.

Get a credit-builder loan. Companies like Self (formerly Self Lender) offer small loans specifically designed to build credit. You make monthly payments into a savings account, and they report your on-time payments to the bureaus. After 12 months, you get the money back minus a small fee. It adds a new tradeline and payment history to your report.

Ask your landlord to report rent payments. If you're renting after the divorce, services like Rental Kharma or Boom can report your rent payments to the credit bureaus. Rent is often the biggest bill you pay each month — you should get credit for paying it on time.

Step 5: Fix Your Utilization Ratio

After closing joint accounts, your available credit drops. If your individual cards carry any balance, your utilization ratio — the percentage of available credit you're using — shoots up.

FICO weighs utilization heavily. It accounts for roughly 30% of your score. The sweet spot is under 10% per card and under 30% overall.

Example: You had $30,000 in total available credit across joint and individual cards. After closing joint accounts, you're down to $5,000 in available credit with a $2,500 balance. That's 50% utilization — and your score is going to reflect it.

Quick fixes:

- Pay down balances aggressively. Even getting from 50% to 30% can swing your score 20 to 40 points.

- Request credit limit increases on your existing cards. If you've been a good customer, many issuers will bump your limit with a soft pull. More available credit with the same balance = lower utilization.

- Keep old individual accounts open. Even if you're not using a card, the available credit helps your ratio. Don't close it.

- Time your payments before statement close. Your credit card reports your balance to the bureaus on your statement closing date — not your due date. Pay down the balance before the statement closes to show a lower utilization.

Step 6: Handle Collections From the Divorce

Collections are one of the ugliest divorce credit problems. Your ex was supposed to pay the Verizon bill. They didn't. Now there's a $340 collection on your report tanking your score.

Here's how to handle collections strategically:

Send a debt validation letter within 30 days of first contact. Under the Fair Debt Collection Practices Act (FDCPA), the collector must prove the debt is valid, the amount is correct, and they have the right to collect it. If they can't validate, they must stop collection efforts.

Negotiate a pay-for-delete. If the debt is legitimate and you need to pay it to move forward, offer to pay in full only if the collector agrees to delete the tradeline entirely from your credit report. Get this agreement in writing before sending a dime. Not every collector will agree, but it's worth asking — especially on smaller balances under $1,000. Check our pay-for-delete guide for templates.

Dispute the collection with the bureaus. File disputes directly with Experian, Equifax, and TransUnion. The collection agency has 30 days to verify the debt. If they bought the debt from the original creditor, they often lack the documentation to verify. Under the FCRA, unverifiable items must be removed.

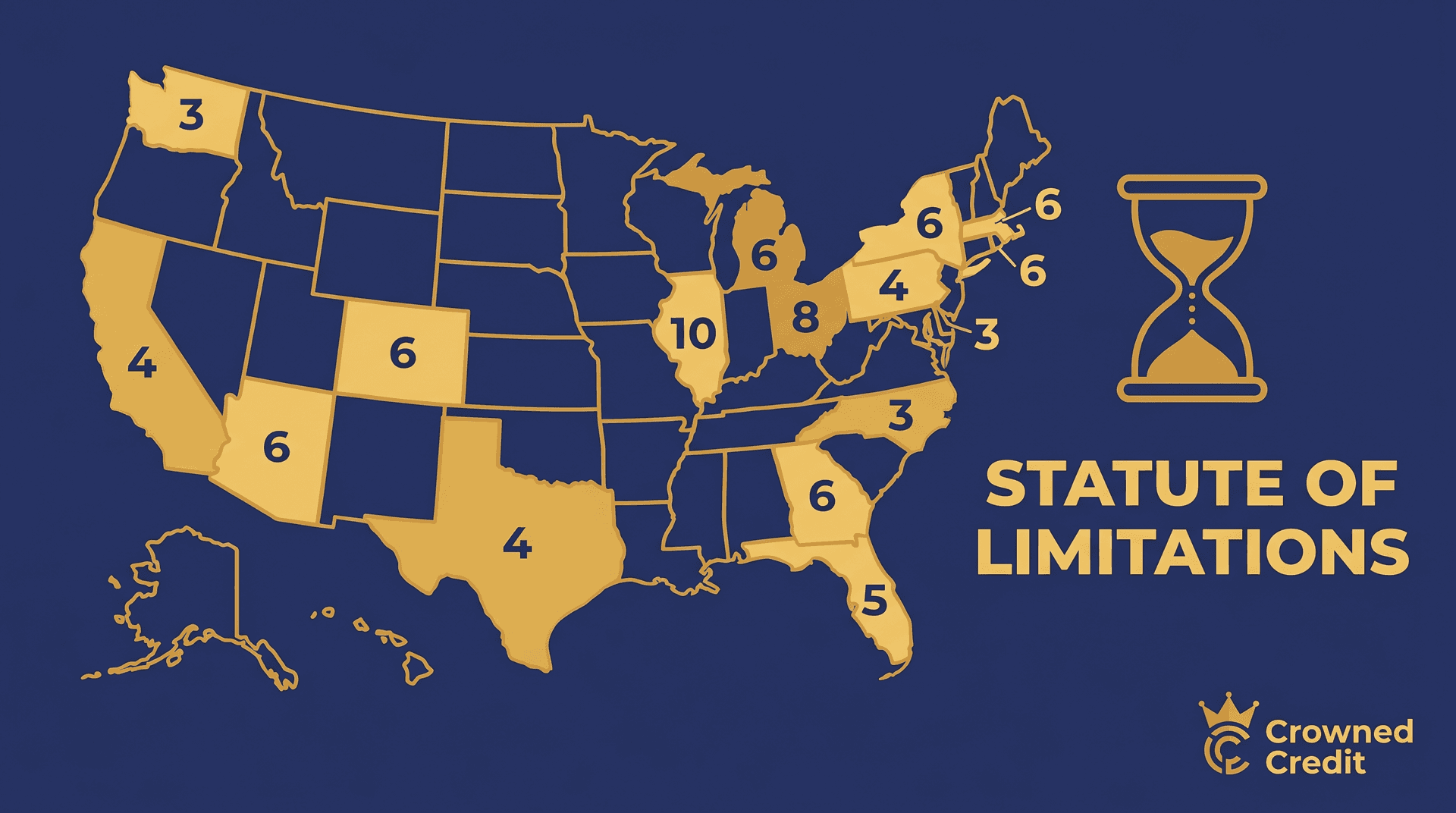

Check the statute of limitations. If the debt is old enough, it may be past the statute of limitations in your state. Time-barred debt can't be legally enforced through a lawsuit. Be careful though — making a payment or even acknowledging the debt can restart the clock in some states.

Step 7: Protect Yourself Going Forward

Rebuilding is only half the equation. You also need to make sure your ex can't damage your credit in the future.

- Freeze your credit with all three bureaus. A credit freeze prevents anyone — including your ex — from opening new accounts in your name. It's free and takes about 10 minutes per bureau. You can temporarily lift the freeze when you need to apply for credit. We wrote a full guide on freezing your credit bureaus.

- Set up fraud alerts. If you suspect your ex might try to open accounts in your name, place a fraud alert with one bureau (it propagates to all three). Creditors will be required to verify your identity before opening new accounts.

- Monitor your credit monthly. Use Credit Karma, Experian's free monitoring, or your bank's credit score tool. Set up alerts for new accounts, hard inquiries, and balance changes. Catch problems early before they escalate.

- Keep copies of your divorce decree handy. You'll need it when dealing with creditors on joint accounts. It doesn't override your legal obligation to the creditor, but it helps when negotiating and documenting your disputes.

Your Credit Recovery Timeline After Divorce

Everyone wants to know: how long will this take? Here's a realistic timeline based on what we see with clients at Crowned Credit:

Month 1-2: Pull all three reports. Identify every joint and disputed account. File disputes on inaccurate items. Separate or close joint accounts. Open a secured card if your profile is thin.

Month 3-4: First round of dispute results come back. Inaccurate items start dropping off. Secured card begins building payment history. Credit utilization improves as you pay down balances.

Month 5-8: Subsequent dispute rounds for stubborn items. Score starts climbing — 30 to 60 points of recovery is common at this stage. You may qualify for an unsecured credit card.

Month 9-12: Most divorce-related damage is repaired or significantly reduced. Score recovery of 80 to 120+ points is realistic if you've been consistent. Mortgage and auto loan qualification becomes possible again.

*Individual results vary based on the complexity of your credit situation, the number and types of negative items, and your specific financial circumstances. Credit repair results are not guaranteed — but strategic, consistent action produces real improvements for the vast majority of clients we work with.

When to Get Professional Help

You can absolutely dispute errors yourself. But if you're dealing with multiple joint accounts gone bad, several collections, fraudulent accounts, and a score that dropped 100+ points — it might make sense to bring in help.

A credit repair company that understands FCRA law can handle the dispute process strategically, challenge creditors and bureaus on your behalf, and often get results faster because they know what works and what doesn't.

At Crowned Credit, we've helped thousands of clients recover from divorce-related credit damage. Our team disputes every negative item using FCRA rights, challenges creditors to verify what they're reporting, and works to remove what they can't prove.

Three service levels to fit your situation:

- Essential: $150 enrollment + $99/month — covers dispute rounds with all three bureaus

- Accelerated: $249 enrollment + $199/month — priority disputes, more aggressive approach, additional strategies

- Momentum: $1,095 one-time — comprehensive, intensive credit restoration

If you want to talk through your situation, book a free consultation or call us at 336-310-0090. We'll review your reports, identify what's holding your score down, and map out a plan — whether you work with us or handle it yourself.

The Bottom Line

Divorce is one of life's most stressful events. The financial mess it leaves behind can feel paralyzing. But credit damage from divorce is temporary — as long as you actually do something about it.

Separate joint accounts. Dispute inaccurate reporting. Build credit in your own name. Protect yourself from future damage. Follow the steps in this guide consistently, and your credit will recover faster than you expect.

Your marriage ended. Your credit score doesn't have to stay broken too.