How to Repair Your Credit After a Foreclosure in 2026

Ashley Rivera

Credit Repair Specialist

Losing a home to foreclosure is one of the most financially and emotionally painful experiences a person can go through. You already know that. What you might not know is that the path back to homeownership — and to a strong credit profile — is shorter and more actionable than most people realize.

This guide covers what actually happens to your credit after a foreclosure, the concrete steps to rebuild faster, the mortgage waiting periods you need to plan around, and where professional credit repair fits into that timeline.

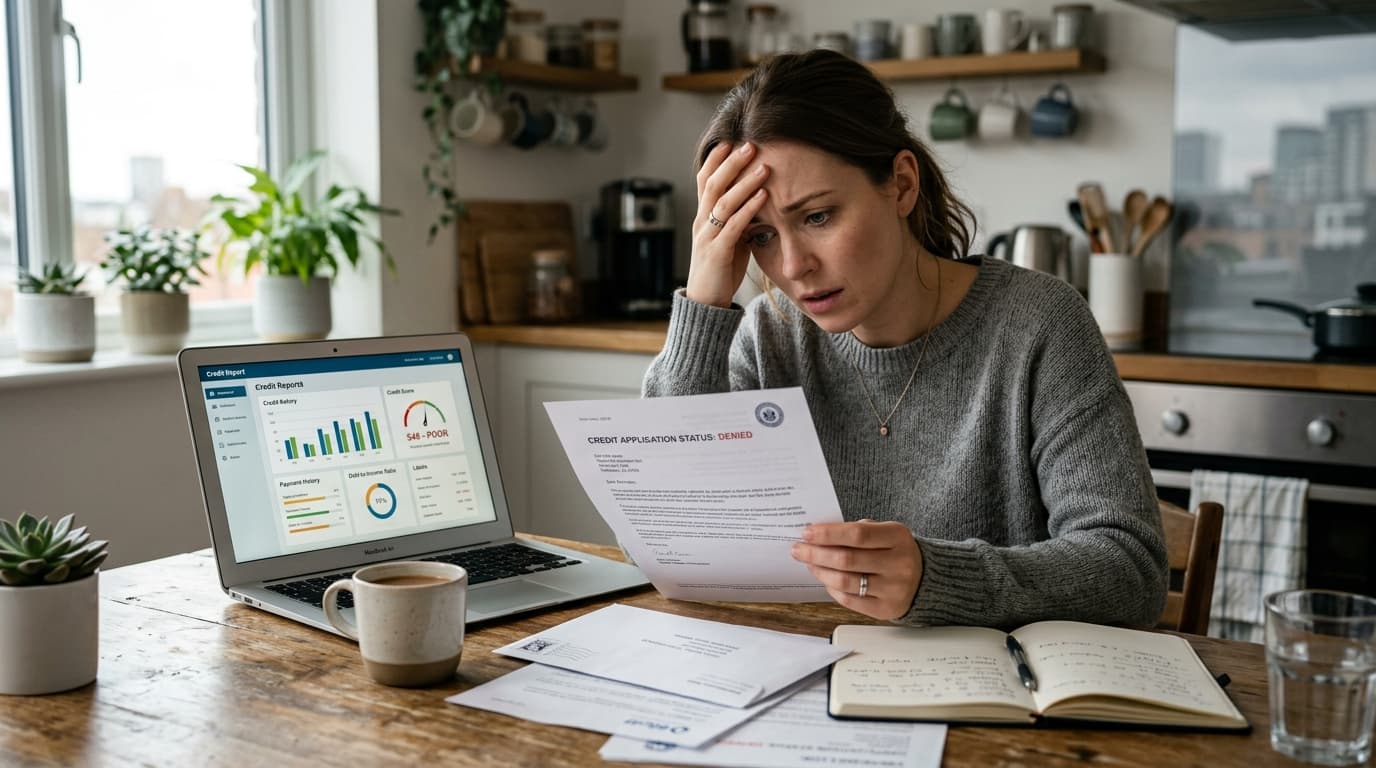

What Foreclosure Does to Your Credit Score

A foreclosure is one of the most damaging entries that can appear on a credit report. Depending on where your score was before, the impact typically looks like this:

- Credit score in the 780s: Expect a drop of 140–160 points

- Credit score in the 720s: Expect a drop of 120–140 points

- Credit score in the 680s: Expect a drop of 85–105 points

The reason the drop is so severe is twofold. First, the missed payments leading up to the foreclosure are each their own negative entry — every 30, 60, and 90-day late payment stacks up. Then the foreclosure itself is recorded as a separate major derogatory mark. So by the time a foreclosure finalizes, you may be looking at 6–12 individual negative entries, not just one.

Under the Fair Credit Reporting Act (FCRA), a foreclosure stays on your credit report for seven years from the date of your first missed mortgage payment that triggered the process — not from the date the foreclosure was finalized. This distinction matters for your planning timeline.

The Good News: You Don't Have to Wait Seven Years

Here's what most people get wrong about foreclosure and credit: they assume their credit is wrecked for seven years and there's nothing to do until the foreclosure drops off. That's simply not true.

Credit scores are calculated based on your entire credit profile — not just the worst items on it. A foreclosure from four years ago matters far less to your score if you've spent those four years building positive history. Lenders look at your recent behavior. A 680 score with consistent, on-time payments over the past two years tells a very different story than a 680 score with no activity at all.

Rebuilding actively gets you to homeownership faster. Waiting passively does not.

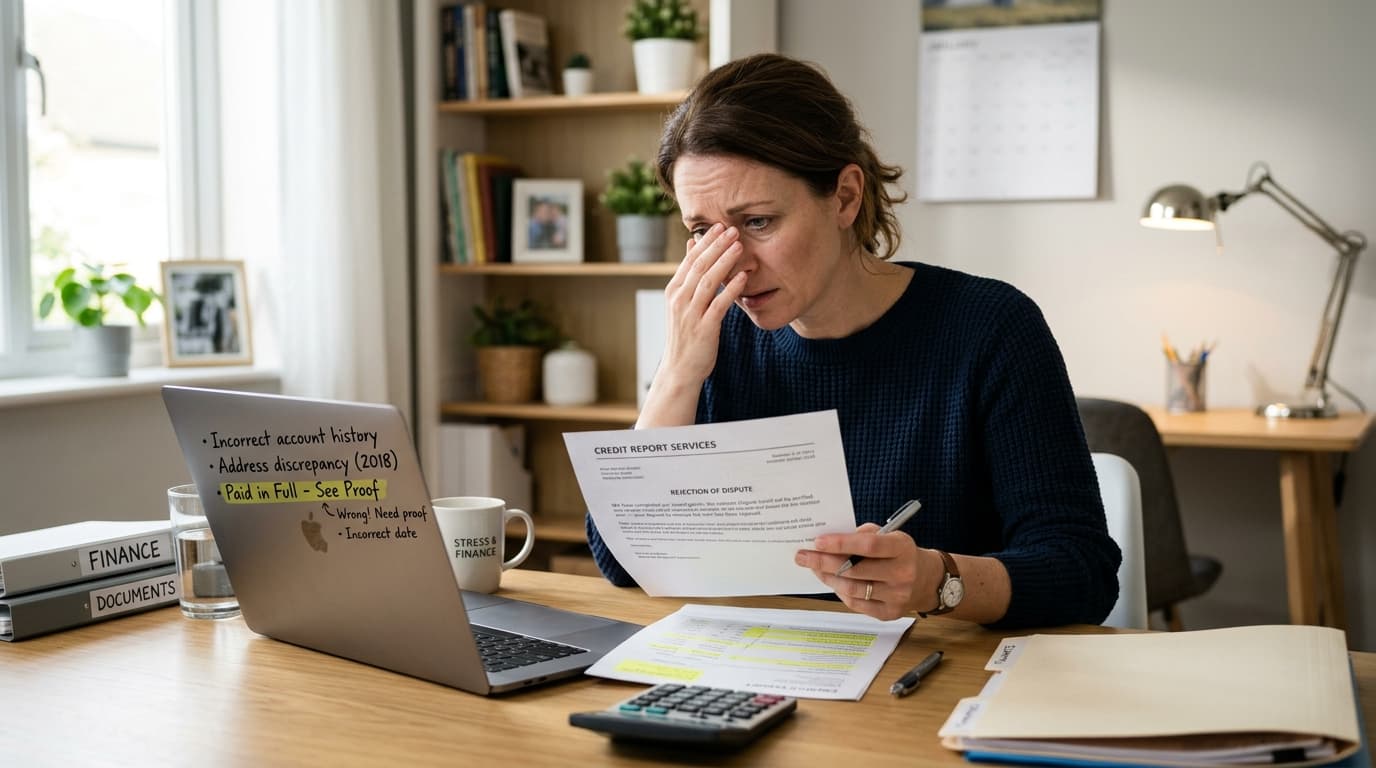

Step 1: Pull All Three Credit Reports and Audit Every Line

Before you can fix anything, you need to know exactly what you're working with. Get your free reports from AnnualCreditReport.com — Equifax, Experian, and TransUnion separately. Don't rely on one bureau. Foreclosure-related entries often appear differently across all three.

What you're looking for:

- The foreclosure entry itself — check that the date, balance, and status are accurate

- Associated missed payment entries — these should align with your actual history; wrong dates are disputable

- Any collection accounts spawned by the foreclosure (HOA fees, deficiency balances, etc.)

- Errors on unrelated accounts — foreclosure situations often involve financial chaos, and mistakes in other areas of your report are common

If the foreclosure itself is reported inaccurately — wrong dates, incorrect balances, wrong status code — you have the right to dispute that information under the FCRA. A legitimate foreclosure reported accurately cannot be removed before seven years. But an inaccurately reported foreclosure is a different story, and those disputes are winnable.

For a deeper walkthrough on reading your report, see our guide on how to read your credit report in 2026.

Step 2: Dispute Every Inaccuracy Aggressively

The foreclosure process rarely happens cleanly. Missed payments get reported on the wrong dates. Deficiency balances are duplicated. Servicer transfers create data errors. Collection accounts sometimes appear with wrong open dates, throwing off the seven-year clock entirely.

Every inaccuracy you find is an opportunity. Dispute it with the credit bureau in writing, citing the FCRA and providing documentation. The bureau has 30 days to investigate and respond. If the furnisher can't verify the information as reported, it must be corrected or removed.

This is where working with professionals makes a real difference. A solo dispute attempt against a large mortgage servicer is manageable — but if you have multiple inaccuracies across three bureaus, plus collections, plus the foreclosure entry itself, managing that systematically while rebuilding your financial life is a lot to carry.

Our team at Crowned Credit handles exactly this. We review your full credit profile, identify every disputable item, and pursue corrections through the proper FCRA channels. If you want to understand your options before committing to anything, book a free consultation here.

Step 3: Start Building Positive Credit Immediately

This is the part most people delay — and it's the biggest mistake. Don't wait until the foreclosure is "gone" to start rebuilding. Start the day after it's finalized. Here's why: FICO's scoring algorithm heavily weights recency. Negative items from 3–4 years ago hurt far less than they did the day they appeared. Positive items from the past 12–24 months carry significant weight.

The most effective rebuilding tools:

Secured Credit Cards

A secured card requires a cash deposit that becomes your credit limit — typically $200–$500. Used responsibly (keeping utilization under 10%, paying the full balance monthly), a secured card starts generating positive payment history from day one. Look for cards that report to all three bureaus and upgrade to unsecured after 12 months of on-time payments.

See our full breakdown of the best secured credit cards for rebuilding credit in 2026.

Credit-Builder Loans

Offered by credit unions and community banks, these loans are specifically designed for people rebuilding credit. You make monthly payments toward a locked savings account, and the lender reports those payments to the bureaus. At the end of the term (usually 12–24 months), you get the funds. You build credit and savings at the same time.

We covered these in detail in our guide on how credit-builder loans work.

Becoming an Authorized User

If you have a family member or close friend with a long-standing, low-utilization credit card account, ask to be added as an authorized user. Their positive history on that account appears on your credit report. This works best when the account is at least 3–5 years old and has never had a late payment.

Keeping Utilization Low

Credit utilization — the percentage of your available revolving credit that you're using — accounts for 30% of your FICO score. Keep it under 10% across all cards. If your only card has a $300 limit, that means carrying no more than $30 on it when your statement closes.

Mortgage Waiting Periods After Foreclosure: The Full Breakdown

Here's what you're actually working toward. These are the minimum waiting periods before you can qualify for a new mortgage after a foreclosure:

| Loan Type | Standard Wait | With Extenuating Circumstances |

|---|---|---|

| FHA Loan | 3 years | 1 year (job loss, medical crisis) |

| VA Loan | 2 years | Case-by-case |

| USDA Loan | 3 years | 1–3 years |

| Conventional (Fannie/Freddie) | 7 years | 3 years with documented hardship |

| Jumbo Loans | 7+ years | Varies by lender |

The FHA path is the most accessible for most people — a 3-year wait is manageable, and FHA loans accept credit scores down to 580 with 3.5% down. If your foreclosure was caused by a documented hardship like job loss or a serious medical event, that waiting period can drop to 12 months under FHA's "Back to Work" guidelines.

The key insight here: your goal during the waiting period isn't just to survive — it's to arrive at that 3-year mark with a credit score that qualifies you for the best possible rate. A 620 FICO gets you in the door. A 700+ FICO gets you a meaningfully lower interest rate over 30 years. On a $280,000 loan, the difference between a 7.5% and a 6.5% rate is roughly $170/month — $61,200 over 30 years.

What About the Other Debts?

Foreclosure doesn't always mean the debt is fully gone. Depending on your state's deficiency laws, your lender may be able to pursue a deficiency judgment for the difference between what you owed and what the property sold for at auction. In non-recourse states (like California and Arizona), this isn't allowed. In recourse states (like Florida and Ohio), it is.

If a deficiency balance ends up in collections, it will appear on your credit report separately. This is disputable if reported inaccurately. If it's accurate, you may want to negotiate a settlement — and we've written a detailed guide on how to negotiate debt settlements that walks through that process.

Additionally, any collection accounts tied to HOA fees, utilities, or other property-related costs from the foreclosure should be audited carefully. These are often reported with errors and are some of the most successfully disputed entries in a post-foreclosure credit profile.

How Long Does the Rebuilding Actually Take?

Realistic benchmarks — these assume active rebuilding, not passive waiting:

- 6 months: 30–50 point improvement if you've added 1–2 positive accounts and kept utilization low

- 12 months: 50–80 point improvement with consistent behavior; score often crosses 600

- 24 months: Many people are in the 640–680 range, approaching FHA qualification territory

- 36 months: With clean recent history, scores of 680–720+ are achievable, which opens up significantly better mortgage rates

These aren't guarantees — your starting point, the number of negative items, and how aggressively you build positive history all affect the pace. But they're grounded in how FICO scoring actually works. The algorithm rewards consistent, recent positive behavior at scale.

⚠️ CROA Compliance Disclosure: Results vary by individual. Credit repair organizations are regulated by the Credit Repair Organizations Act (CROA). No company, including Crowned Credit, can guarantee specific score improvements or outcomes. The timelines and improvements referenced in this article are illustrative ranges based on general credit behavior patterns, not guarantees for any specific client.

Should You Work With a Credit Repair Company?

Depends on your situation. Here's when it makes sense, and when it doesn't:

DIY is reasonable if: Your foreclosure is recent (under 2 years), your other accounts are clean, you have time to research and write dispute letters, and you're comfortable managing three bureau relationships simultaneously.

Professional repair makes sense if: You have multiple negative items across all three bureaus, you have collections or deficiency balances in addition to the foreclosure itself, you've tried disputing on your own without results, or you want to maximize your score before a specific mortgage application date.

At Crowned Credit, we specialize in complex credit profiles — exactly the kind that emerges from a foreclosure. We don't just dispute the obvious stuff. We audit every line of every report, identify errors in dates, balances, and account statuses that most people miss, and pursue corrections methodically using your full FCRA rights.

Our plans start at $150 enrollment + $99/month for the Essential plan. The Accelerated plan is $249 enrollment + $199/month for faster, more comprehensive dispute coverage. We also offer a one-time Momentum option at $1,095 for clients who want full-service work without a monthly commitment.

If you're serious about buying a home again and want to know exactly where your credit stands and what's fixable, book a free consultation with our team. No pressure, no pitch — just a real look at your credit profile and an honest assessment of what's possible.

The Bottom Line

A foreclosure is a setback, not a sentence. Seven years sounds like a long time, but the mortgage waiting period — especially for FHA loans — is only 3 years. And the credit rebuilding that makes those 3 years count starts the day you decide to start it.

The people who come out of a foreclosure strongest are the ones who don't wait. They pull their reports, dispute what's wrong, open a secured card, make every payment on time, and show up at that 36-month mark with a credit profile that tells a story of recovery and responsibility.

That story is worth telling. And Crowned Credit can help you write it.