Deleted Account Came Back on Your Credit Report? What Reinsertion Means in 2026

Ashley Rivera

Credit Repair Specialist

You win a dispute, watch an ugly account disappear, breathe for about two weeks, then pull your report again and see the same item staring back at you.

That will make anybody mad.

It also creates real confusion, because people assume a deleted account is gone for good. Sometimes it is. Sometimes it is not. Under the Fair Credit Reporting Act, a deleted item can come back in certain situations. That process is usually called reinsertion.

The key is this: an account coming back does not automatically mean the bureau or furnisher did something illegal, but it absolutely can mean you need to act fast and document everything.

If you are trying to qualify for a mortgage, auto loan, apartment, or even a better credit card, reinsertion can cost you points, create underwriting headaches, and wreck your timing. That is why this is one of those issues you do not want to handle casually.

If you want help reviewing the full file, book a consultation with Crowned Credit or compare options on our pricing page.

The Short Answer

Yes, a deleted account can come back on your credit report in 2026. If the furnisher later verifies the information as complete and accurate, a bureau may reinsert it. But the bureau is not supposed to just sneak it back in silently. Under federal law, the consumer reporting agency is generally required to notify you in writing within 5 business days after reinserting previously deleted information.

That means your next move is not guessing. It is checking:

- Whether the item is actually the same account

- Whether you received a reinsertion notice

- Whether the dates, balance, status, and ownership details are accurate

- Whether the account is being reported consistently across all three bureaus

If you need background first, read how credit disputes work, what the FCRA is, and our guide to re-aging and re-insertion.

What Reinsertion Actually Means

Reinsertion is when information that was deleted from your credit file after a dispute shows up again later.

That usually happens in one of three scenarios:

- The furnisher verifies the account after it was deleted. The bureau may have removed it during the dispute window, then added it back once the creditor or collector responded.

- The account was transferred or sold. A new collector or debt buyer may start reporting its own tradeline tied to the same underlying debt.

- The bureau file updates and the data comes back in. Sometimes the issue is messy system syncing rather than a clean, obvious dispute result.

That last point matters. People often say, “The bureau put the same account back on my report,” when the reality is more specific. It may be the same debt with a different furnisher. It may be the same tradeline with updated data. Or it may be a flat-out reporting problem.

Those are not the same fight, and if you treat them like they are, you can waste a month arguing the wrong point.

Why Deleted Items Sometimes Come Back

A lot of deletions are not permanent victories. Some are more like temporary removals while the bureau waits on verification.

Here is a simple example.

- You dispute a collection account on April 1

- The bureau contacts the collector

- The collector does not verify it inside the initial investigation window

- The bureau deletes the account

- Later, the collector provides information the bureau accepts as verification

- The account gets reinserted

That is why you never want to celebrate a deletion too early without keeping copies of your reports, letters, screenshots, and dispute results.

Experian has publicly noted that deleted items can reappear after the dispute process if the furnisher later verifies the information. The law does not say a bureau must block an item forever just because it was removed once. What the law does require is that the reinsertion process follow the rules.

What the FCRA Says About Reinserted Accounts

The Fair Credit Reporting Act gives consumers protections here. Under 15 U.S.C. § 1681i, if previously deleted information is reinserted, the credit bureau generally must:

- Certify the information as complete and accurate before reinserting it

- Notify you in writing within 5 business days after the reinsertion

- Provide details about the furnisher that verified the information if requested or included through the notice process

That does not mean every account that comes back is automatically removable again. It means the bureau has obligations. If those obligations were not met, that becomes part of your leverage.

And just so there is no confusion, reinsertion is different from re-aging. Re-aging is when the reporting dates are manipulated to make an old debt look newer than it really is. That is a separate problem, and it can be a much bigger violation.

How to Tell Whether It Is the Same Account or a New Tradeline

This is where people rush and get sloppy.

Do not look at the creditor name for two seconds and assume you know what happened. Slow down and compare the details:

- Creditor or collector name

- Partial account number

- Balance

- Status, such as collection, charged off, paid, settled, or disputed

- Date opened

- Date updated

- Estimated removal date

- Any remarks or comments attached to the tradeline

Example. If an old medical collection disappeared under one agency name and then returns under a different debt buyer with a different account number format, you may be looking at a newly reported collection tradeline, not a literal reinsertion of the exact same line. That still deserves scrutiny, but the way you challenge it may be different.

If you are not confident reading the file, keep our credit report guide open while you compare bureau entries line by line.

What to Do Right Away if an Account Came Back

Here is the smartest sequence.

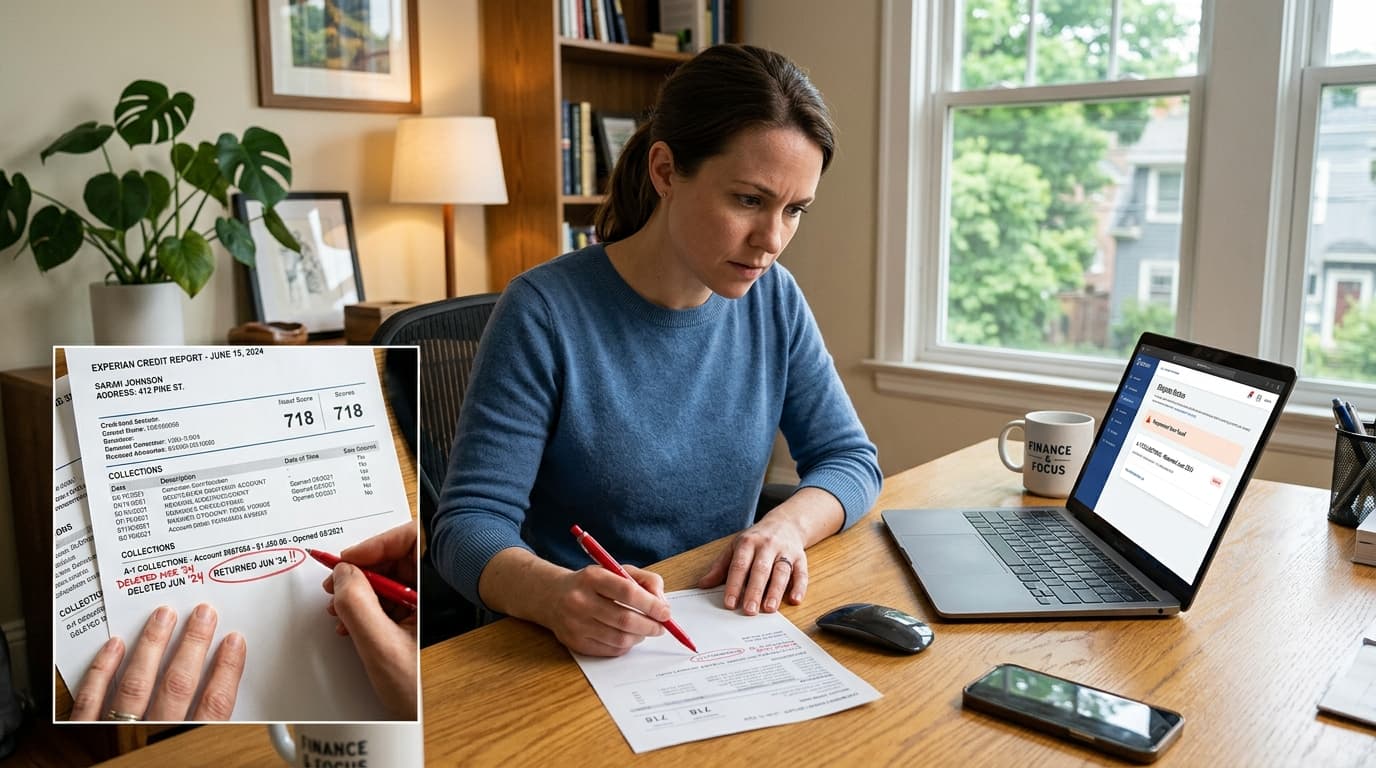

- Pull updated reports from all three bureaus. Do not rely on one credit app summary.

- Save proof. Keep the earlier report showing the deletion and the new report showing the return.

- Look for the reinsertion notice. Check mail, email, and any bureau message center tied to your account.

- Compare the full tradeline details. Do not assume it is identical just because the debt sounds familiar.

- Identify the exact issue. Is the account inaccurate, incomplete, misleading, duplicated, or not properly verified?

That last step matters most. Crowned Credit does not approach these files with the weak idea that you should only shrug and accept whatever a bureau says. The real question is whether the information being reported is accurate, complete, consistent, and properly verified under your rights as a consumer.

When You Should Dispute the Reinserted Item Again

You should take a harder look if any of these are true:

- You never received the required reinsertion notice

- The balance changed in a way that does not make sense

- The dates now make the debt look newer than before

- The account is duplicated

- The wrong creditor or collector is attached

- The account had already been removed and the current reporting still cannot be properly verified

At that point, you may dispute with the bureau again, and in some cases directly with the furnisher. Keep the dispute tight and specific. “This account is wrong” is weak. “This account was previously deleted, reappeared without proper notice, and now shows an inconsistent balance and reporting date compared with my prior report” is much stronger.

If collections are involved, you should also understand the bigger context around what collections are, whether an old debt can be reported as new, and how pay-for-delete negotiations work.

Can a Reinserted Account Hurt Your Score?

Yes. If a negative item comes back, it can affect your credit profile again, especially if it is recent-looking, unpaid, or tied to a major derogatory event like a charge-off or collection.

How much damage it does depends on the rest of your file:

- A thin file usually feels the hit harder

- A person already carrying high utilization may feel it more

- A mortgage-ready file near a cutoff score can get knocked into a worse pricing tier

- An older derogatory item may still matter if timing is bad, even if the score impact is smaller than before

Here is the part people hate. The score drop is not the only problem. Underwriting friction can be worse than the score itself. A lender may ask questions, request letters, pause the file, or require updated documentation just because the report changed mid-process.

CROA Disclosure: No company can legally guarantee a specific credit score increase, account deletion, loan approval, or result within a specific timeframe. Outcomes depend on the information reported, whether it can be verified, how the bureaus and furnishers respond, and the overall condition of your credit profile.

Mistakes That Make This Worse

These are the common ones:

- Only checking one bureau. The account may have come back on one report but not the others.

- Failing to save old reports. If you cannot prove the deletion, you lose useful leverage.

- Confusing a new collector with the exact same tradeline. Similar problem, different strategy.

- Arguing from memory instead of documents. The paper trail wins, not your frustration.

- Applying for new credit in the middle of the mess. That can make a shaky file worse.

If you are close to applying for a home, also read credit score requirements for a mortgage and how dispute comments can complicate underwriting.

When Professional Help Makes Sense

You may be able to handle a clean, one-account reinsertion issue yourself.

Professional help makes more sense when:

- You have multiple negative items moving around at once

- You are preparing for a mortgage or auto approval

- The account keeps reappearing after prior disputes

- The dates, balances, and ownership details are inconsistent

- You need a strategy across collections, charge-offs, utilization, and dispute timing, not just one letter

That is where Crowned Credit can help. We review the full file, identify where the reporting is weak, and build a strategy around the accounts that are hurting you most. If you want us to look at it, call 336-310-0090 or book now.

Current pricing:

- Essential: $150 setup + $99/month

- Accelerated: $249 setup + $199/month

- Momentum: $1,095 one-time

Bottom Line

If a deleted account came back on your credit report, do not panic, but do not ignore it either. A reinsertion can be legal in some situations, but the bureau still has rules to follow, and the details on the account still need to be accurate, complete, and properly verified.

Your best move is to pull all three reports, compare the tradeline details, check for the required notice, and challenge anything that is inconsistent, misleading, incomplete, or unsupported. If you want a team to review it with you and map out the smartest next step, book a consultation with Crowned Credit.