How to Remove a Bankruptcy From Your Credit Report in 2026

Ashley Rivera

Credit Repair Specialist

Seeing a bankruptcy on your credit report can feel like a dead end. A lender pulls your file, spots the public record, and suddenly the rates get worse, the approval gets harder, or the answer is just no.

Here’s the good news: a bankruptcy entry is not untouchable. It can be challenged. It can age off. And in some cases, it can come off sooner when the reporting cannot be properly verified, contains errors, or breaks the rules it’s supposed to follow.

The bad news is this: there’s a lot of nonsense online about “guaranteed” bankruptcy deletions. That’s where people get burned. If you want real results, you need to understand what can actually work, what usually does not, and how to approach the process strategically.

If you want help reviewing the full picture on your reports, Crowned Credit can do that with you. You can book a call here or compare options on our pricing page.

Important disclaimer: Credit results vary. No one can legally guarantee a specific score increase or exact timeline for removing negative items from a credit report. Any improvement depends on your full file, the accuracy and verifiability of the reporting, and how lenders score your profile.

How long does a bankruptcy stay on your credit report?

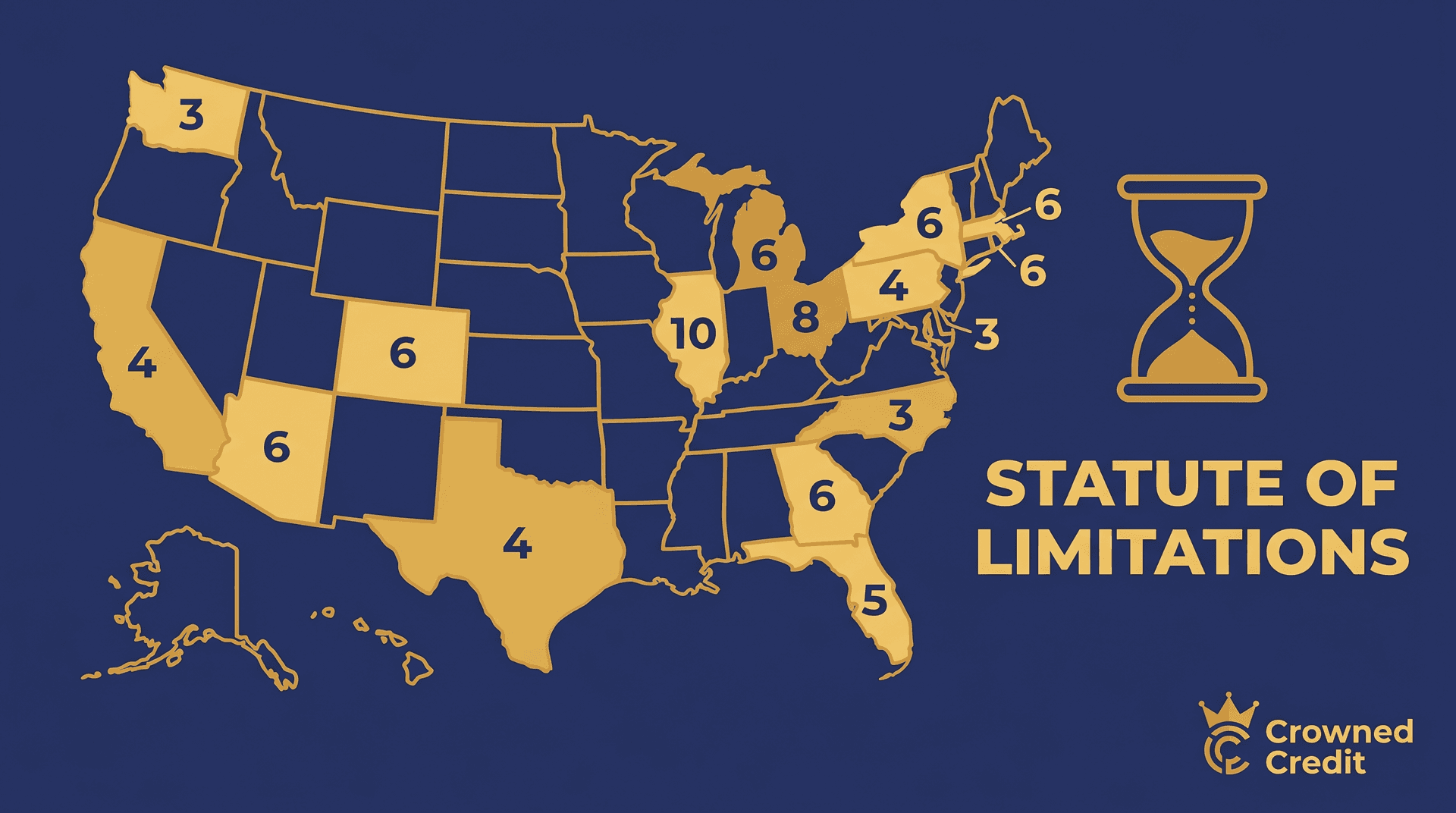

In most cases, a Chapter 7 bankruptcy can stay on your credit report for up to 10 years from the filing date. A Chapter 13 bankruptcy usually stays for up to 7 years from the filing date. That is why the first move is not guessing. It is checking exactly what type of bankruptcy is reporting, which bureaus are showing it, and what dates they are using.

If you have not pulled all three reports yet, start there. Review Equifax, Experian, and TransUnion line by line. You can also read our breakdown on how long bankruptcy stays on your credit report if you want the timing side in more detail.

Can a bankruptcy really be removed early?

Sometimes, yes. But not because somebody waved a magic wand.

What matters is whether the bankruptcy entry is being reported in a way that is complete, accurate, timely, and properly verifiable. Under the Fair Credit Reporting Act, consumer reporting agencies have legal duties when they report negative information and when they respond to disputes. If the bureaus or furnishers cannot support what they are reporting, the item can become vulnerable.

That does not mean every bankruptcy disappears early. It means you should not assume a bankruptcy is permanent just because it appears on a report today.

For a quick refresher on your rights, see our FCRA guide and your rights as a consumer.

What can make a bankruptcy entry removable?

These are the most common pressure points worth reviewing:

- Wrong dates: The filing date, dismissal date, discharge date, or expected removal date is incorrect.

- Mixed-file issues: Information from another consumer’s file got blended into yours.

- Identity problems: The name, address, Social Security number, or court details do not line up cleanly with you.

- Bureau verification failures: A bureau continues reporting the record after a dispute without adequate reinvestigation.

- Inconsistent reporting across bureaus: One bureau reports different court details, chapter type, or status than the others.

- Obsolete reporting: The item should have aged off already but is still showing.

Here is the practical way to think about it: you are not arguing with emotion. You are forcing the reporting system to prove what it is saying. If it cannot, that opens the door.

Step 1: Pull all three reports and mark every inconsistency

Do not rely on one app score or one bureau summary. Pull all three full reports and compare the bankruptcy section side by side.

Look for:

- Different court names or case numbers

- Different filing or discharge dates

- Different chapter type listed

- A bankruptcy showing on one bureau but not the other two

- Accounts included in bankruptcy that are reporting balances or statuses incorrectly afterward

Example: if Experian shows a Chapter 13 filed in June 2019, Equifax shows August 2019, and TransUnion shows it as dismissed when it was actually discharged, that is not “close enough.” Those inconsistencies matter.

Step 2: Dispute the bankruptcy strategically, not sloppily

A weak dispute usually gets a weak result. “Please remove this, it hurts my score” is not a real strategy.

A better approach is to challenge the entry with specifics. Identify the exact problem. Point to the inconsistency. Demand reinvestigation. Make the bureau verify the reporting, not just rubber-stamp it.

Your dispute can focus on things like inaccurate dates, inconsistent status, incomplete identifying information, or failure to properly substantiate the record after you challenged it. If the record is being reported broadly across your file, the connected accounts may need their own review too.

This is one reason many people turn to professional help. Bankruptcy disputes can overlap with charge-offs, collections, included-in-bankruptcy accounts, and post-bankruptcy rebuilding errors. Crowned Credit’s team can review that full chain, not just the public record line by itself. If you want that done for you, book a consultation.

Step 3: Review the accounts tied to the bankruptcy

Even when the bankruptcy public record stays for now, the tradelines attached to it may still be challengeable.

This is where people miss opportunity. They focus only on the bankruptcy record and ignore the accounts around it. But you might also have:

- Accounts still showing past due after discharge

- Balances that should be zero but are still reporting

- Duplicate collection entries

- Charge-offs reporting in a way that does not match the bankruptcy outcome

Cleaning up those surrounding items can materially improve the file even before the bankruptcy itself ages off. If you are rebuilding after a filing, our guides on rebuilding credit after bankruptcy and how bankruptcy affects credit are worth reading next.

Step 4: Watch the timelines and follow up

Credit bureaus generally have timelines for handling disputes, but consumers lose leverage when they send one dispute and then disappear.

Track what you sent, when you sent it, what evidence you attached, and how each bureau responded. If the answer comes back vague, incomplete, or inconsistent with the documentation, that matters. A sloppy reinvestigation is not the same thing as a valid one.

Documentation wins here. Keep copies of:

- Your credit reports before and after each dispute

- Dispute letters and upload confirmations

- Court paperwork if you have it

- Any bureau response letters

- Screenshots of status changes

What usually does not work

Let’s save you time.

- Generic online templates with no facts behind them

- Paying somebody for a “guaranteed delete” promise

- Submitting five random disputes at once with no strategy

- Ignoring the attached tradelines and only fighting the public record

- Assuming the first rejection means the reporting is bulletproof

The people who get stuck are usually doing one of two things: either they do nothing, or they do a messy DIY process that gives the bureaus an easy excuse to verify everything and move on.

How to rebuild while the bankruptcy is still reporting

Waiting around is a mistake. Even if the bankruptcy remains for now, you can still improve the rest of your file.

Focus on the fundamentals:

- Perfect payment history from this point forward

- Low revolving utilization, ideally well below 30%

- Fresh positive accounts if your profile is thin

- Authorized user strategy where appropriate and structured correctly

- Ongoing review of inaccurate negative items beyond the bankruptcy itself

Example: somebody with a 540 score after bankruptcy might not need a miracle. They may need three things done well for six months: inaccurate negatives challenged, utilization brought down from 82% to under 10%, and two positive revolving accounts reporting cleanly. That can change the lending conversation a lot faster than most people expect, even before the bankruptcy ages off.

If you want to understand that side better, read what affects your credit score and how authorized user strategy works.

Important disclaimer: Examples are illustrative only. Results, score changes, and timing vary by file, bureau data, lender scoring model, and whether negative information can be updated or removed.

Should you hire a credit repair company for bankruptcy-related issues?

If your file is simple, you may choose to handle it yourself. But many bankruptcy files are not simple. They involve multiple bureaus, inconsistent post-bankruptcy tradelines, old collections, charge-offs, utilization problems, and time-sensitive borrowing goals like a mortgage or auto loan.

That is where professional help can make sense. A strong credit repair company should not promise fantasy results. It should help you identify what is vulnerable, challenge what should be challenged, and build a cleaner profile around the negative items that remain.

Crowned Credit offers three core options depending on how aggressive you want to be:

- Essential: $150 setup + $99/month

- Accelerated: $249 setup + $199/month

- Momentum: $1,095 one-time

If you want someone to review the bankruptcy, the attached accounts, and the fastest path to a stronger file, call 336-310-0090 or book a consultation here.

Bottom line

A bankruptcy on your credit report is serious, but it is not the end of the story.

The smartest move is to stop treating it like one big hopeless label. Break it down. Verify the chapter type. Check the dates. Compare all three bureaus. Challenge inconsistencies. Review the tradelines tied to the filing. Then rebuild the parts of the file you can control right now.

That is how progress usually happens: not with one magic letter, but with a disciplined strategy.

If you want Crowned Credit to review your reports and map out the next step, book your call or explore the pricing options that fit your situation.