Credit Repair vs. Debt Consolidation: What's Right for Your Situation?

Ashley Rivera

Credit Repair Specialist

If you're dealing with debt, a low credit score, or both, you've probably come across two common solutions: credit repair and debt consolidation. They sound similar, and people often confuse them — but they solve very different problems.

Choosing the wrong one can cost you time and money. Choosing the right one (or combining both strategically) can put you on a faster path to financial stability.

Here's a straightforward breakdown of credit repair vs. debt consolidation so you can make the best decision for your situation in 2026.

What Is Credit Repair?

Credit repair is the process of identifying and disputing inaccurate, outdated, or unverifiable information on your credit reports. Under the Fair Credit Reporting Act (FCRA), you have the legal right to challenge errors with the three major credit bureaus — Equifax, Experian, and TransUnion.

Common items addressed through credit repair include:

- Late payments reported incorrectly

- Collections accounts that don't belong to you or contain errors

- Charge-offs with inaccurate balances or dates

- Hard inquiries you didn't authorize

- Outdated negative items that should have fallen off your report

Credit repair doesn't erase legitimate debts. It targets mistakes and discrepancies that are unfairly dragging your score down. When those errors are removed, your credit score can improve — sometimes significantly.

How Credit Repair Works

A credit repair company (or you, on your own) reviews your credit reports, identifies disputable items, and sends formal dispute letters to the bureaus and creditors. The bureaus are required by law to investigate within 30 days and remove anything they can't verify.

Professional credit repair services like Crowned Credit handle the entire dispute process for you — from pulling your reports and identifying errors to drafting dispute letters and following up with bureaus. It's a systematic, ongoing process that typically takes 3–6 months depending on the complexity of your file.

What Is Debt Consolidation?

Debt consolidation combines multiple debts — credit cards, medical bills, personal loans — into a single payment, usually at a lower interest rate. The goal is to simplify your payments and reduce how much you pay in interest over time.

Common forms of debt consolidation include:

- Personal consolidation loans from a bank or online lender

- Balance transfer credit cards with 0% introductory APR

- Home equity loans or HELOCs (using your home as collateral)

- Debt management plans through nonprofit credit counseling agencies

How Debt Consolidation Works

You take out a new loan or credit line to pay off your existing debts. Instead of managing five different payments with five different interest rates, you make one payment each month. If the new interest rate is lower than your existing rates, you save money over the life of the debt.

Debt consolidation doesn't remove anything from your credit report. Your original debts are paid off (which can actually help your credit), but the consolidation loan itself shows up as new debt.

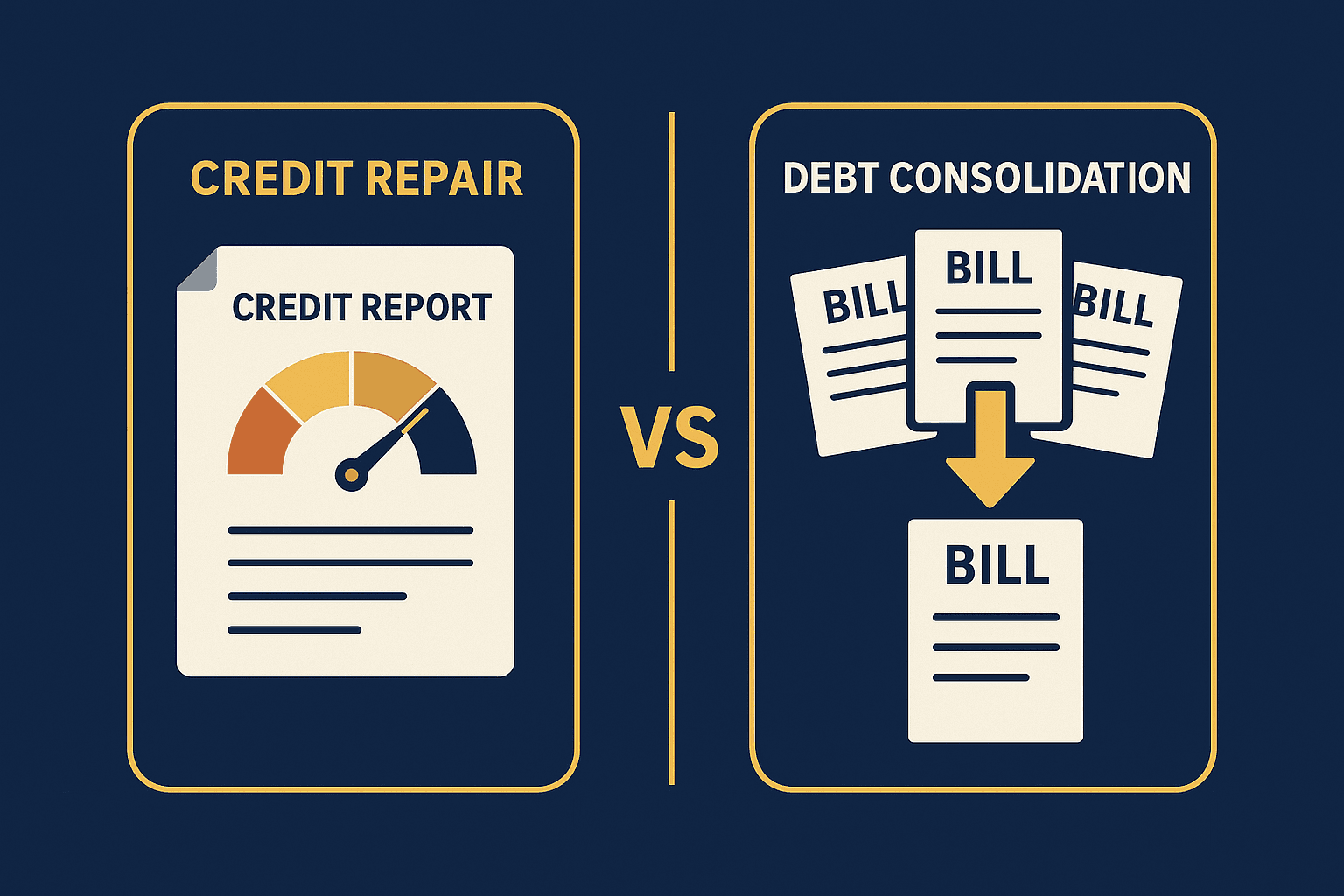

Key Differences Between Credit Repair and Debt Consolidation

Understanding the core differences helps you figure out which path makes sense:

- Primary goal: Credit repair fixes your credit report and raises your score. Debt consolidation simplifies debt payments and reduces interest.

- What it addresses: Credit repair targets inaccurate or unfair items on your credit report. Debt consolidation addresses outstanding debt balances.

- Impact on debt: Credit repair doesn't reduce what you owe. Debt consolidation restructures what you owe.

- Impact on credit score: Credit repair can improve your score by removing negative items. Debt consolidation may help your score long-term through consistent payments.

- Timeline: Credit repair typically takes 3–6 months. Debt consolidation loan terms run 2–7 years.

- Best for: Credit repair is best for people with credit report errors or unfair negatives. Debt consolidation is best for people with multiple high-interest debts.

Pros and Cons of Credit Repair

Pros

- Directly improves your credit score by removing inaccurate negative items

- Opens doors to better loan rates, housing, and employment opportunities

- You have legal rights backing the process (FCRA, FDCPA)

- Professional services handle the heavy lifting — you don't need to navigate bureau bureaucracy alone

Cons

- Only addresses inaccurate information — legitimate negative items may remain

- Takes time — results aren't overnight (expect 3–6 months)

- Monthly cost for professional services (though the ROI from a higher score usually pays for itself)

- Not a debt reduction strategy — your balances stay the same

Pros and Cons of Debt Consolidation

Pros

- Simplifies payments — one bill instead of many

- Can lower your interest rate, saving money long-term

- Reduces financial stress with a clear payoff timeline

- On-time payments build positive credit history

Cons

- Doesn't fix your credit report — errors and negative marks stay

- Requires decent credit to qualify for the best consolidation rates

- Risk of accumulating new debt if spending habits don't change

- Some options (like HELOCs) put assets at risk as collateral

- Balance transfer cards often charge 3–5% transfer fees and revert to high APR after the intro period

When to Choose Credit Repair

Credit repair is the right move if:

- Your credit report contains errors, outdated items, or accounts you don't recognize

- You've been denied credit, housing, or employment due to report inaccuracies

- Your score is lower than it should be based on your actual financial behavior

- You want to qualify for better rates before consolidating or taking on new credit

If you're not sure what's on your report or whether errors are hurting your score, a free consultation with a credit repair professional can clarify your options. The team at Crowned Credit specializes in identifying exactly what's holding your score back and building a personalized dispute strategy.

When to Choose Debt Consolidation

Debt consolidation makes sense if:

- You have multiple debts with high interest rates (especially credit card debt)

- Your credit report is mostly accurate — your score reflects real debt, not errors

- You can qualify for a consolidation loan with a lower rate than your current debts

- You need structure and simplicity to stay on top of payments

Just keep in mind: consolidation works best when paired with a commitment to not rack up new debt on the accounts you just paid off.

How Credit Repair and Debt Consolidation Work Together

Here's what most people miss: credit repair and debt consolidation aren't either/or. In many cases, the smartest move is using both — in the right order.

Step 1: Start with credit repair. Clean up your report first. Removing inaccurate negative items raises your score, which qualifies you for better consolidation terms.

Step 2: Consolidate with a stronger score. Once your credit is cleaner, you'll likely qualify for lower interest rates on a consolidation loan — saving you more money over time.

Step 3: Maintain both. Keep monitoring your credit reports for new errors while making consistent payments on your consolidated debt. This combination builds long-term financial health.

This two-step approach is especially powerful if your score is currently too low to qualify for favorable consolidation offers. Repairing your credit first gives you leverage.

The Bottom Line

Credit repair and debt consolidation solve different problems. Credit repair fixes your credit report — removing errors that unfairly lower your score. Debt consolidation restructures your debt — making it easier and cheaper to pay off.

If your credit report has inaccuracies dragging your score down, credit repair should be your first priority. If your report is accurate but you're drowning in high-interest payments, consolidation may be the better path. And if you're dealing with both issues, tackling credit repair first sets you up for better consolidation terms down the road.

Whatever your situation, the worst thing you can do is nothing. Every month you wait is another month of paying higher interest rates, getting denied for opportunities, or watching errors sit on your report unchallenged.

Ready to see what's on your credit report and start improving your score? Get started with Crowned Credit today and take the first step toward the financial future you deserve.

## Further reading - [Compare credit repair and bankruptcy](/blog/credit-repair-vs-bankruptcy) - [Get started with Crowned Credit](/get-started) - [See our pricing options](/pricing)