How to Remove Student Loans From Your Credit Report in 2026

Ashley Rivera

Credit Repair Specialist

Student loan debt in America has crossed $1.77 trillion. That's not just an abstract number — it shows up as tradelines on roughly 43 million credit reports, and for millions of borrowers, those tradelines are doing serious damage.

Maybe you defaulted during the pandemic chaos. Maybe your servicer reported a late payment that never actually happened. Maybe you finished rehabilitation but the default marker is still sitting there like a stain that won't wash out. Whatever the situation, you're here because you want those student loan entries gone — or at least corrected — and you want to know exactly how to make that happen.

Here's the reality: not every student loan tradeline can be removed. But a surprising number of them can be successfully disputed, corrected, or eliminated entirely under federal law. Let's break down every avenue available to you in 2026.

How Student Loans Show Up on Your Credit Report

Before you can fix the problem, you need to understand what you're looking at. Each individual student loan — not each lender, each loan — appears as a separate tradeline on your credit report. Someone who took out loans for four years of college might have 8, 10, even 15+ separate tradelines.

Each tradeline shows:

- Account status — current, delinquent, in default, closed, or paid in full

- Payment history — a month-by-month record going back up to 7 years

- Balance information — original amount, current balance, monthly payment

- Servicer information — who currently holds or services the loan

- Date of first delinquency — this is what triggers the 7-year clock

A single 90-day late payment on a student loan can drop your score by 60-110 points. A default? That can tank it by 150+ points and stay on your report for up to 7 years from the date of first delinquency.

The good news: student loan reporting is riddled with errors. Servicers have been transferred, merged, and reshuffled so many times — especially between 2020 and 2025 — that misreported balances, duplicate tradelines, and incorrect statuses are extremely common.

5 Legitimate Ways to Remove Student Loans From Your Credit Report

1. Dispute Inaccurate or Unverifiable Information Under the FCRA

This is the most powerful tool in your arsenal, and it applies to both federal and private student loans.

Under the Fair Credit Reporting Act (FCRA), every item on your credit report must be accurate, complete, and verifiable. If a student loan tradeline contains any error — wrong balance, incorrect payment history, misreported dates, wrong account status — you have the legal right to dispute it. The credit bureau then has 30 days to investigate, and if the furnisher (your servicer or lender) can't verify the information, it must be removed.

Here's what makes student loans especially vulnerable to disputes in 2026:

- Servicer transfers: Between the MOHELA transition, the end of the payment pause, and the Fresh Start rollout, millions of accounts were transferred between servicers. Every transfer is a chance for data to get mangled.

- Duplicate tradelines: It's common to see the same loan reported by both the old and new servicer simultaneously. That double-reporting inflates your debt-to-income ratio and suppresses your score.

- Incorrect default dates: If the date of first delinquency is wrong, the 7-year clock is wrong — and you may be carrying a negative mark longer than legally allowed.

- Phantom balances: Loans that were consolidated, forgiven, or discharged sometimes still show an active balance.

To dispute, you'll send a letter to each credit bureau (Equifax, Experian, TransUnion) identifying the specific tradeline and the specific error. Include your loan account numbers, any supporting documentation, and a clear statement of what needs to be corrected. For a step-by-step walkthrough of the dispute process, check out our complete guide to disputing credit report errors.

You can also send a Section 609 dispute letter demanding that the bureau produce the original documentation verifying the debt. If they can't produce it, the tradeline comes off.

2. Federal Student Loan Rehabilitation

If your federal student loans are in default, rehabilitation is one of the most effective ways to clean up your credit report — because it actually removes the default notation from your report once completed.

Here's how it works:

- Contact your loan holder (check StudentAid.gov to find them)

- Agree to make 9 "reasonable and affordable" monthly payments within a 10-month window

- Your payment amount is typically set at 15% of your discretionary income — for many borrowers, this can be as low as $5/month

- After completing 9 payments, the default status is removed from your credit report

Critical detail: Rehabilitation removes the default record, but the late payments that led up to the default will still appear. Those late payments will naturally age off your report after 7 years from the date they occurred. Still, removing the default itself can produce a significant score increase — some borrowers see 50-100+ point jumps after rehabilitation completes.

One major catch: you can only rehabilitate a specific loan once. If you default again after rehabilitation, your only option is consolidation (which doesn't remove the default record).

3. Federal Loan Consolidation

Direct Consolidation Loans let you combine multiple federal student loans into a single new loan. While consolidation doesn't remove the default history the way rehabilitation does, it accomplishes something important: it creates a brand new tradeline with a current, in-good-standing status.

Your old defaulted loan tradelines will still show their history, but the new consolidated loan starts fresh. Over time, as the old tradelines age and the new one builds positive payment history, your score recovers.

Consolidation is often the faster path — it can be completed in weeks rather than the 9-10 months rehabilitation requires. It's also the only option if you've already used your one rehabilitation chance.

After consolidation, make sure to check that your old loan tradelines are updated to reflect a $0 balance and "paid through consolidation" status. If they're not, dispute the inaccuracy.

4. Fresh Start Program Benefits (If You Enrolled Before It Ended)

The federal Fresh Start initiative, which ran from late 2023 through 2024, gave defaulted borrowers an automatic path back to good standing. If you enrolled in Fresh Start:

- Your loans were returned to "in repayment" status with a new servicer

- The default record was removed from your credit report

- Your eligibility for federal student aid was restored

- You preserved your future rehabilitation option (Fresh Start didn't count as your one-time rehabilitation)

If you enrolled but your credit report still shows default status, that's a clear FCRA violation you should dispute immediately. The bureaus and your servicer are required to update this information.

If you missed the Fresh Start window, rehabilitation and consolidation are still available. The important thing is that you have options — default doesn't have to be permanent.

5. Wait for the 7-Year Age-Off

Under the FCRA, negative student loan information — late payments, defaults, charge-offs — must be removed from your credit report 7 years after the date of first delinquency. Not 7 years from when you paid it off, not 7 years from the last collection attempt. Seven years from when you first went delinquent on that specific account.

This is a hard deadline. If a negative student loan entry is older than 7 years and still on your report, it's there illegally. Dispute it, and the bureau must remove it.

Pro tip: check the "date of first delinquency" field carefully. Some servicers report incorrect dates (intentionally or through sloppy recordkeeping), which pushes the 7-year window further out than it should be. If the date is wrong, dispute it.

Common Student Loan Reporting Errors to Look For

Pull your credit reports from all three bureaus at AnnualCreditReport.com (it's free) and look for these specific issues:

- Same loan, multiple tradelines: If the same loan shows up under both the old and new servicer, one of those is inaccurate.

- Wrong balance after payoff or forgiveness: If you paid off, consolidated, or received forgiveness but the balance still shows as active, that's an error.

- Incorrect account status: Loans showing "in default" after rehabilitation or Fresh Start completion are incorrectly reported.

- Late payments during the COVID forbearance period (March 2020 - September 2023): Federal student loan payments were paused. No late payments should appear during this window. If any do, dispute them immediately — this is one of the easiest disputes to win.

- Wrong monthly payment amount: If you're on an income-driven repayment plan but your report shows the standard payment amount, that inflates your debt-to-income ratio and can hurt loan approvals.

- Loans that don't belong to you: Mixed files happen more often than you'd think, especially with common names. If a student loan on your report isn't yours, dispute it.

Federal vs. Private Student Loans: Different Rules Apply

Everything above about rehabilitation, consolidation, and Fresh Start applies only to federal student loans (Direct Loans, FFEL loans, Perkins loans). Private student loans — from lenders like Sallie Mae, Discover, or your bank — play by different rules.

For private student loans, your options are:

- FCRA disputes: You have the same right to dispute inaccurate information on private loans. The bureau and the lender must investigate within 30 days.

- Negotiated settlements: Some private lenders will agree to update your credit report as part of a settlement. This is more art than science — it depends on the lender, the age of the debt, and your negotiation leverage. Our guide on pay-for-delete negotiations covers the strategy in detail.

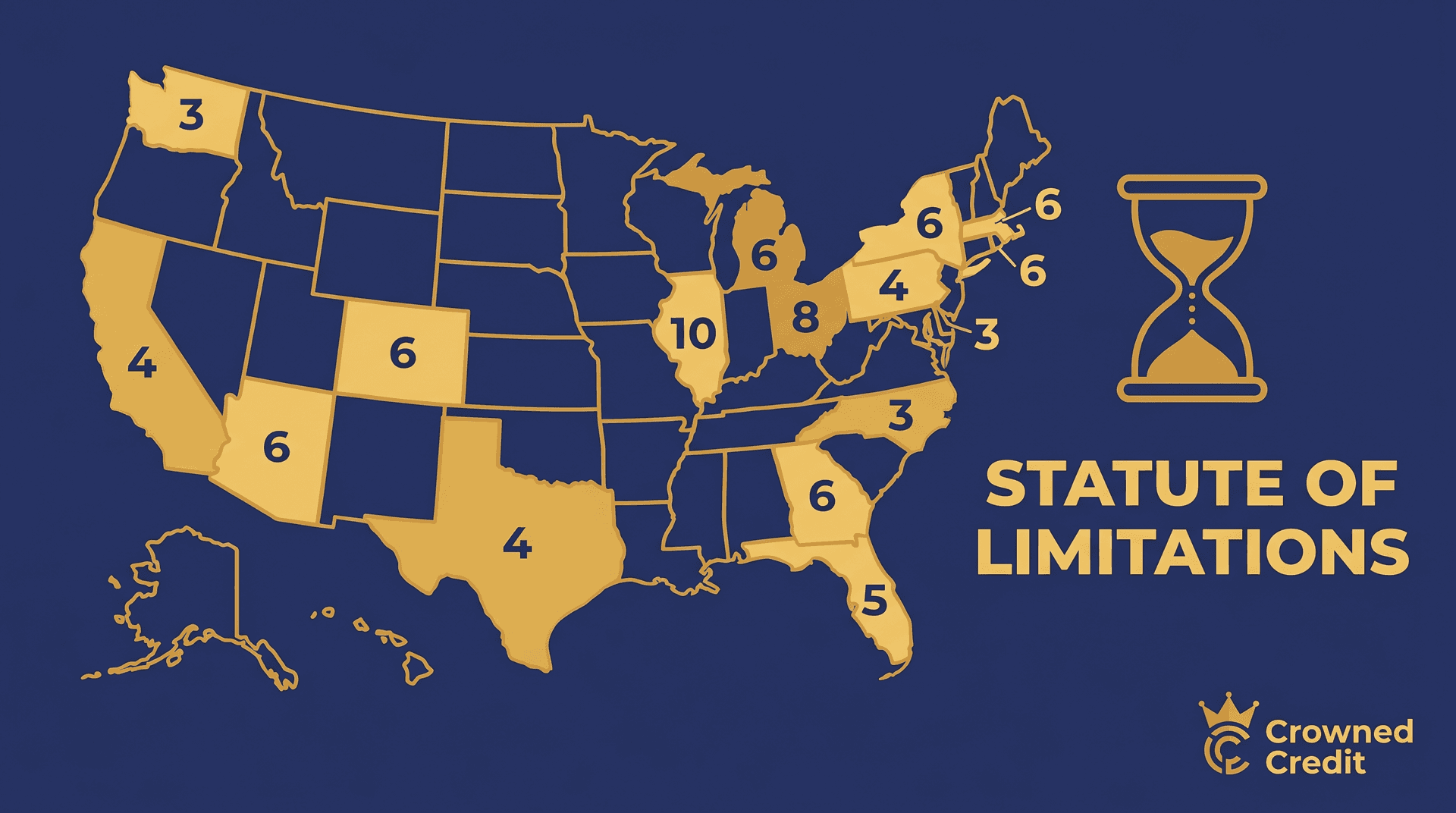

- Statute of limitations: Private student loans are subject to state statutes of limitations (unlike federal loans, which have no statute of limitations on collections). If your state's SOL has passed, the lender can't sue you — though the tradeline can still appear on your report until the 7-year FCRA limit. Check our state-by-state statute of limitations guide.

- Debt validation: If a private student loan has been sent to collections, you can send a debt validation letter requiring the collector to prove the debt is yours and the amount is correct. If they can't validate it within 30 days, they must stop collection efforts and the tradeline should be removed.

How Student Loan Removal Affects Your Credit Score

The impact of removing student loan negative marks depends on your overall credit profile, but here are some real-world ranges:

- Removing a default: 50-150+ point increase, depending on how many other negatives exist on your report

- Removing late payment history: 20-75 point increase per tradeline, with more recent late payments having a bigger impact when removed

- Removing duplicate tradelines: Variable, but reducing your reported debt-to-income ratio always helps, especially for mortgage and auto loan approvals

- Correcting wrong balance to $0: Can significantly improve utilization metrics and qualification for new credit

If student loans are your primary negative item, getting them corrected or removed can be the difference between a 580 and a 720 — between subprime rates and prime rates, between a $1,800/month mortgage payment and a $1,400 one on the same house.

When to Get Professional Help

Disputing student loan errors yourself is absolutely possible. But there are situations where professional credit repair makes the difference:

- You have multiple student loan tradelines with different issues across all three bureaus

- Your disputes keep coming back "verified" even though you know there are errors

- You're dealing with a servicer that was transferred or shut down, making verification difficult

- You have both federal and private student loans with overlapping issues

- You need your credit cleaned up on a specific timeline — for a home purchase, car loan, or apartment application

At Crowned Credit, we deal with student loan disputes regularly. Our team knows exactly which documentation to request, which FCRA provisions to cite, and how to escalate when servicers or bureaus don't respond properly. We dispute negative items strategically using your rights under the FCRA — the same rights that require bureaus and furnishers to verify every item they report.

Our plans start at $150 enrollment + $99/month for the Essential plan, or $249 + $199/month for the Accelerated plan if you want faster, more aggressive disputes. We also offer a Momentum package at $1,095 one-time for borrowers who want everything handled upfront. You can book a free consultation to see which option fits your situation, or check out our full pricing breakdown.

CROA Disclosure: Under the Credit Repair Organizations Act, we are required to inform you that: (1) You have the right to dispute inaccurate information on your credit report at no cost by contacting the credit bureaus directly. (2) No one can guarantee specific results or a specific credit score increase. (3) You have three business days to cancel any credit repair contract without penalty. Results vary based on individual credit profiles and the accuracy of information being disputed.

Your Action Plan: What to Do This Week

- Pull all three credit reports from AnnualCreditReport.com — it's free

- List every student loan tradeline and note the servicer, balance, status, and payment history for each one

- Flag any errors using the checklist above — wrong balances, duplicate entries, incorrect statuses, late payments during the COVID pause

- Check your federal loan status on StudentAid.gov — confirm whether your loans are in good standing, default, or qualified for rehabilitation

- Start your disputes — either DIY with our dispute guide, or schedule a consultation with our team to build a dispute strategy for your specific situation

Student loan entries don't have to permanently wreck your credit. Between FCRA disputes, rehabilitation, consolidation, and simple age-off rules, there are real, legal paths to getting your report cleaned up. The key is knowing which strategy matches your specific situation — and then actually following through.

Questions about your student loans and credit report? Book a free consultation or call us at 336-310-0090.