7 Financial Habits You Didn't Realize Are Wrecking Your Credit Score in 2026

Ashley Rivera

Credit Repair Specialist

Beyond the Basics: The Hidden Habits Holding Your Score Hostage

You’ve heard the standard credit advice a thousand times. Pay your bills on time. Don't max out your credit cards. Keep old accounts open. You're doing all of that, or at least you’re trying to. So why isn’t your credit score budging? Why does it feel like you’re stuck in financial quicksand?

It’s because the most talked-about factors are only part of the story. Your credit score is a complex algorithm influenced by dozens of data points. And some of the most damaging factors are the everyday financial habits you might not give a second thought. These are the silent score killers—the small, seemingly innocent decisions that add up to significant damage over time.

If you're frustrated with your progress and ready to find the real culprits, you're in the right place. We're going to uncover seven of the most common—and most destructive—financial habits that could be wrecking your credit without you even realizing it. Let’s get started.

1. Co-signing a Loan or Credit Card (Even for Family)

It starts with a simple, heartfelt request. A family member or a close friend needs a car, an apartment, or a personal loan, but their credit isn't strong enough to get approved. They promise they’ll make every payment on time. As a co-signer, you’re just there as a backup, right?

Wrong.

When you co-sign, you are not a backup; you are a co-borrower. That debt is 100% your legal responsibility in the eyes of the lender and the credit bureaus. From the moment you sign, that new loan or credit card appears on your credit report. This immediately increases your debt-to-income ratio and can impact your ability to get new credit for yourself.

But the real danger comes from late payments. If the primary borrower is even one day late, that 30-day delinquency gets reported on your credit history. It doesn’t matter if you didn’t know about it. It doesn’t matter if they promised. A single late payment can drop your score by 50-100 points, and the damage can take years to repair.

The Fix: Make it a personal policy to never co-sign. If you feel compelled to help, it's better to gift them the money for a larger down payment or simply say no. Protecting your own financial health must be the priority.

2. Ignoring That "Small" Unpaid Bill

You switched internet providers and there was a final bill for $45 you forgot about. You visited an urgent care clinic and thought insurance covered everything, but there was a remaining co-pay of $75. It's a small amount, so what's the big deal?

These tiny, forgotten debts are a huge source of credit damage. The original creditor will make a few attempts to collect, but they'll quickly sell the debt to a third-party collection agency for pennies on the dollar. Once that happens, a new and damaging "collection" account is placed on your credit report.

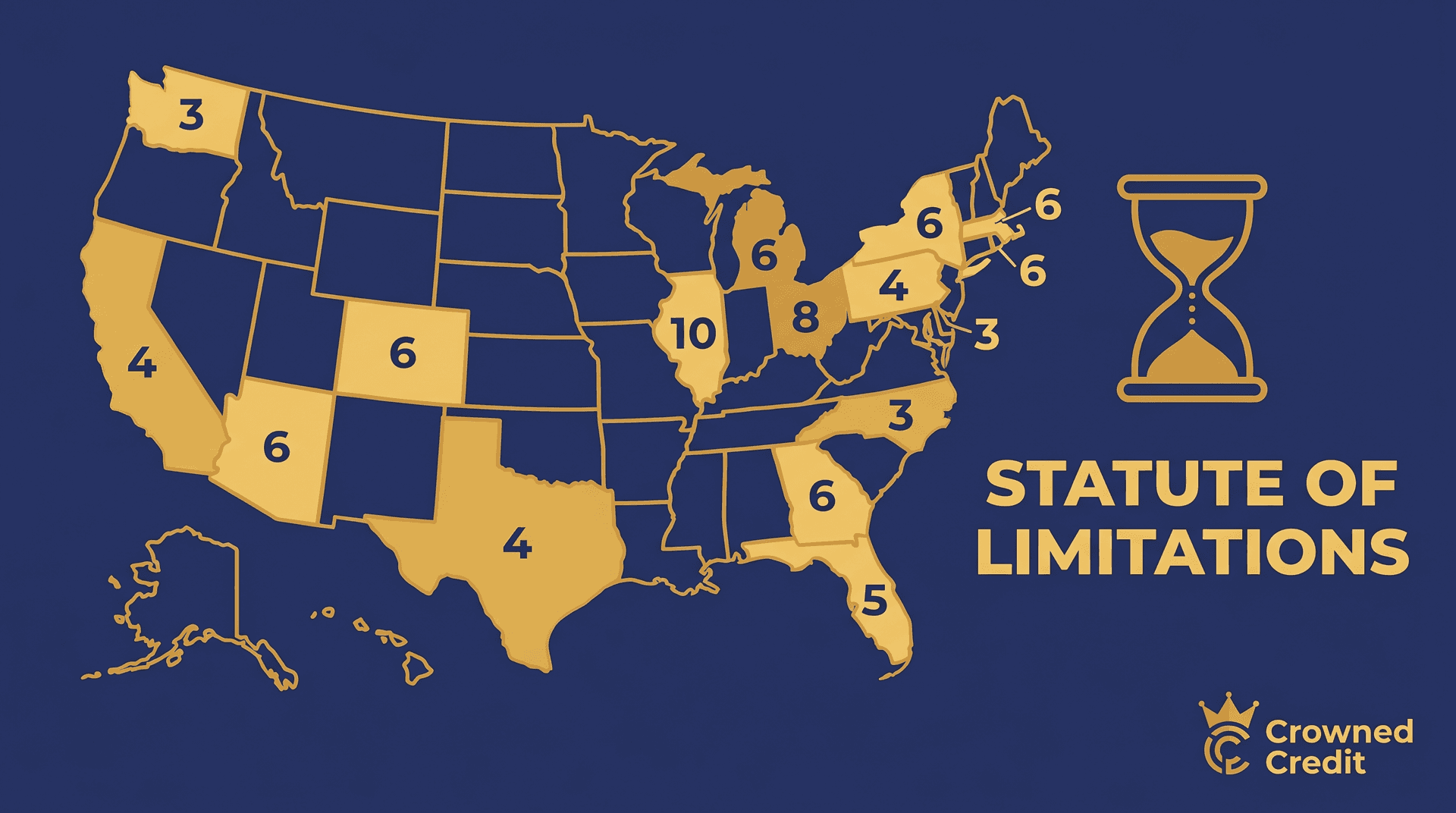

A single collection account, even for a small amount, can devastate your score. It signals to lenders that you are a high-risk borrower who doesn't meet their obligations. This can stay on your report for up to seven years, making it harder to get approved for everything from a mortgage to a simple cell phone plan.

The Fix: Keep meticulous records of any account you close or service you cancel. Always ask for a final bill with a zero balance in writing. And if you get a call from a collection agency, don't ignore it. Address it immediately, preferably by sending a debt validation letter to confirm the debt is legitimate before you pay anything.

3. Closing Your Oldest Credit Card

You opened a credit card in college. It has a low limit, no rewards, and you haven't used it in years. It seems like good financial hygiene to close it and simplify your life. Resist the urge.

Closing a credit card can harm your score in two significant ways:

- It reduces your average age of accounts. The length of your credit history makes up about 15% of your FICO score. If you close your oldest account, the average age of all your accounts drops, which can cause a sudden dip in your score.

- It increases your credit utilization ratio. This is the second most important factor in your score. Let's say you have two cards: the old one with a $5,000 limit and a new one with a $10,000 limit. Your total available credit is $15,000. If you have a $5,000 balance on the new card, your utilization is 33% ($5,000 / $15,000). If you close the old card, your available credit drops to $10,000, and your utilization instantly jumps to 50%—a range that lenders see as risky.

The Fix: Keep your oldest accounts open, especially if they don't have an annual fee. To prevent the issuer from closing it for inactivity, use it for a small, recurring purchase (like a streaming subscription) and set up automatic payments to pay it off in full each month.

4. The "All Debt is Bad" Mindset

Being debt-free is a fantastic goal. However, avoiding credit entirely can leave you with a "thin file"—meaning you have too little credit history for the bureaus to assign you a score. Without a credit score, lenders have no way to assess your risk, making it nearly impossible to get approved for major life purchases like a car or a home.

Similarly, having only one type of credit (like credit cards) and no installment loans (like a car loan, mortgage, or personal loan) can also hold your score back. "Credit Mix" accounts for 10% of your FICO score. Lenders want to see that you can responsibly manage different types of debt.

The Fix: You don't need to go into major debt to build a credit history. You can start with a secured credit card or become an authorized user on a family member's card. Small credit-builder loans are another excellent tool. The goal is to show a consistent history of responsible borrowing and on-time payments across a mix of account types.

5. Paying Off Installment Loans Too Quickly

This is one of the most counter-intuitive habits. You get a bonus at work and decide to pay off your car loan a year early. You feel proud and responsible. Then you check your credit score, and it's dropped 15 points. What happened?

As mentioned above, credit mix is important. When you pay off an installment loan, you close an open, active tradeline. This can slightly reduce the diversity of your credit profile. More importantly, that account stops reporting positive payment history each month. An open, active loan with a history of on-time payments is a powerful positive factor for your score. Once it's closed, its positive influence begins to fade.

Disclaimer: This doesn't mean you should keep debt around just for a credit score. The interest you save by paying off a loan early often outweighs the small, temporary dip in your credit score. However, it's a financial habit that has a surprising, and often alarming, effect on your credit that you need to be aware of.

The Fix: Don't panic. If paying off a loan makes financial sense, do it. Just be prepared for a potential short-term score drop and ensure you have other open, active accounts (like credit cards) that are reporting positive history to balance it out.

6. Only Checking Credit Karma

Free credit monitoring apps like Credit Karma are great tools for tracking your overall credit health. They can alert you to new accounts, changes in balances, and potential fraud. However, they have one major drawback: they typically show you a VantageScore, not a FICO score.

What's the difference? While both are credit scores, they use different models and can have wildly different results. The problem is that over 90% of top lenders use a version of the FICO score to make their lending decisions. You might see a 720 on Credit Karma and feel confident, only to be denied for a mortgage because the lender's FICO model shows a 650.

The Fix: Use free apps for monitoring, but find a source for your FICO score before any major application. Many credit card companies offer a free FICO score as a cardholder benefit. You can also purchase your reports directly from myFICO.com to see the exact scores lenders are using.

7. Not Having a System for Your Finances

This is the habit that enables all the others. Do you have bills on auto-pay? Do you have a budget? Do you know your account login information? If you're managing your finances "when you think about it," you're setting yourself up for failure.

Forgetting a due date, miscalculating a payoff amount, or losing a paper bill can all lead to late payments and collections. A lack of organization is a lack of control. And when you're not in control, your credit score pays the price.

The Fix: Create a simple system. Use a budgeting app, set up calendar reminders for due dates, and enable auto-pay for at least the minimum payment on all your bills. Keep a secure file with all your account numbers, due dates, and login information. A few hours of organization can save you years of credit-related headaches.

Ready to Break the Cycle?

Recognizing these habits is the first step. But if the damage is already done, fixing it can feel overwhelming. Negative items like collections, charge-offs, and late payments can hold your score down for years, costing you thousands in high interest rates.

You don't have to do it alone. At Crowned Credit, we help people understand their credit reports, challenge inaccurate or unfair negative items, and build a strategy for a stronger financial future. Our process is transparent and effective, designed to help you leverage your consumer rights under the Fair Credit Reporting Act (FCRA).

If you're tired of being stuck and ready to take control, we're here to help. Book a free, no-obligation credit consultation with our team today. We'll review your report, identify the specific issues holding you back, and create a personalized action plan.

Don't let silent habits dictate your financial future. Call us at 336-310-0090 or visit our pricing page to learn more about our programs, including our popular Accelerated plan for $249 + $199/mo. It's time to build the credit you deserve.