Debt Validation Letter: How to Force Collectors to Prove You Owe (2026 Guide)

Ashley Rivera

Credit Repair Specialist

A debt collector just called you about a $3,200 medical bill from 2023. You don't remember it. Maybe it's real, maybe it's not — but here's what matters: they have to prove it before you pay a dime.

That's not wishful thinking. It's federal law. Under the Fair Debt Collection Practices Act (FDCPA), specifically Section 1692g, you have the right to demand that any debt collector validate the debt they're trying to collect. If they can't? They're legally required to stop contacting you about it.

The tool that makes this happen is called a debt validation letter. And if you're dealing with collectors — whether the debt is yours or not — sending one should be your very first move.

What Is a Debt Validation Letter?

A debt validation letter is a written request you send to a debt collector asking them to prove three things:

- That the debt exists and is legitimate

- That the amount they're claiming is accurate

- That they have the legal authority to collect it from you

This isn't the same as a 609 dispute letter, which goes to the credit bureaus under the FCRA. A debt validation letter goes directly to the debt collector under the FDCPA. Different law, different target, different purpose — but both are powerful tools in your credit repair arsenal.

Think of it this way: a 609 letter says "prove this belongs on my credit report." A debt validation letter says "prove I actually owe this money."

Why Debt Validation Matters More Than You Think

Here's a stat that should make you uncomfortable: the Federal Trade Commission found that one in five consumers has at least one error on their credit report. The Consumer Financial Protection Bureau (CFPB) received over 100,000 debt collection complaints in 2024 alone.

Debts get sold, resold, and sold again. Each time a portfolio changes hands, data gets corrupted. Account numbers get transposed. Balances get inflated with fees that were never part of the original agreement. Sometimes a debt that was already paid shows up under a new collector's name.

Without validation, you could end up paying:

- Someone else's debt — same name, wrong Social Security number

- A debt you already settled — the original creditor got paid, but a junk debt buyer purchased the old account anyway

- An inflated amount — the collector tacked on unauthorized fees, interest, or charges

- A time-barred debt — one that's past the statute of limitations in your state and legally unenforceable

Validation forces the collector to do their homework. And a surprising number of them can't.

Your Legal Rights Under the FDCPA

Section 1692g of the FDCPA lays out specific rules collectors must follow:

Within five days of first contacting you, a debt collector must send you a written "validation notice" that includes:

- The amount of the debt

- The name of the creditor

- A statement that you have 30 days to dispute the debt

- A statement that if you dispute in writing within 30 days, they'll provide verification

- A statement that they'll provide the original creditor's name and address upon written request

Here's the critical part: once you send a written dispute within that 30-day window, the collector must stop all collection activity until they provide verification. That means no more calls, no more letters, no reporting to credit bureaus — nothing until they prove the debt is valid.

If they continue collection efforts without validating? They're violating federal law, and you may have grounds for a lawsuit under the FDCPA with statutory damages up to $1,000 per violation, plus actual damages and attorney's fees.

Debt Validation vs. Debt Verification: What's the Difference?

People use these terms interchangeably, but they're technically different steps in the same process:

- Validation notice: The information the collector is required to send YOU within five days of first contact

- Validation request (your letter): Your written dispute asking the collector to prove the debt

- Verification: The proof the collector sends back (if they can) after receiving your request

In practice, most people call the whole process "debt validation." The important thing is that you're exercising your FDCPA rights — the terminology matters less than the action.

When to Send a Debt Validation Letter

Timing is everything. Here's when you should absolutely send one:

Within 30 Days of First Contact (Strongest Position)

The FDCPA gives you a 30-day validation period after receiving the collector's initial notice. Disputing within this window legally requires them to stop collection until they verify. Miss this window and they can continue collecting while they gather verification — you still have the right to request it, but it doesn't pause their efforts.

When You Don't Recognize the Debt

Got a call about a $1,800 credit card balance from a company you've never heard of? That's a red flag. The original creditor may have sold the account to a debt buyer who then hired a collection agency. By the time it reaches you, the details might be completely garbled.

When the Amount Seems Wrong

You had a $600 medical bill that went to collections, but now they're saying you owe $1,400? That extra $800 needs to be accounted for — validation forces them to itemize every dollar.

When You've Already Paid

Zombie debt is real. You settled an account two years ago, and now a different collector is coming after the same balance. This happens more often than people realize, especially with medical debt that gets coded incorrectly.

When Collections Appear on Your Credit Report

If a collection account is dragging your credit score down, validation is your first move. If the collector can't validate, you have strong grounds to get it removed from your credit report entirely.

How to Write a Debt Validation Letter (Step by Step)

Your letter doesn't need to be complicated. In fact, shorter is better — you want it clear, direct, and legally sound. Here's exactly what to include:

1. Your Information

Full name and mailing address. Don't include your Social Security number, bank account details, or any financial information. The collector should already have your identifying information if the debt is legitimate.

2. The Collector's Information

The company name, address, and any reference or account number they provided in their initial notice.

3. A Clear Statement That You're Disputing the Debt

State plainly: "I am writing to dispute this debt and request validation pursuant to my rights under the FDCPA, 15 U.S.C. § 1692g."

4. What You're Requesting

Ask for specific documentation:

- The name and address of the original creditor

- The original account number with the original creditor

- Proof that you are the correct debtor (not just a name match)

- A copy of the original signed contract or agreement

- A complete payment history showing how the current balance was calculated

- Proof that the collector is licensed to collect in your state

- Proof that the debt is within the statute of limitations

5. A Statement About Ceasing Collection

Remind them: "Until this debt is validated, I request that you cease all collection activity, including reporting to any consumer reporting agency."

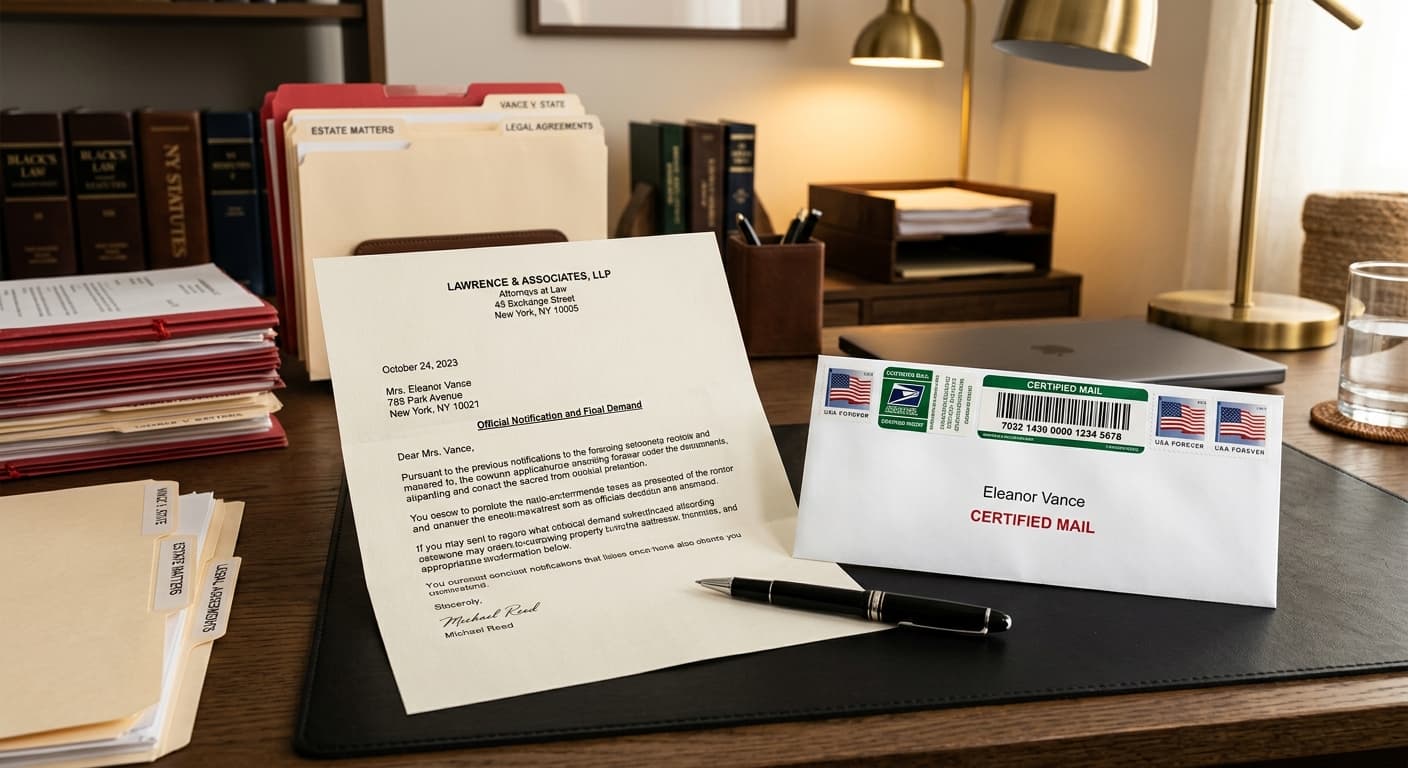

6. Send It Certified Mail With Return Receipt

This is non-negotiable. Always send your debt validation letter via USPS certified mail with return receipt requested. This creates a paper trail proving exactly when they received it. If they violate the FDCPA after receiving your letter, that green card is your evidence. The cost is about $4-5 — well worth it.

What Happens After You Send the Letter

Once the collector receives your validation request, one of four things typically happens:

Scenario 1: They Validate the Debt

The collector sends back documentation proving the debt is yours, the amount is correct, and they're authorized to collect. If the validation checks out, you know the debt is legitimate and can decide your next move — whether that's negotiating a pay-for-delete agreement, setting up a payment plan, or exploring other options.

Scenario 2: They Send a Weak Validation

This is common. The collector sends back a computer printout showing your name and a balance — but no signed contract, no payment history, no proof of assignment. This isn't adequate validation. A printout generated from the collector's own system doesn't prove anything. You can push back and request actual documentation from the original creditor.

Scenario 3: They Go Silent

Many collectors — especially junk debt buyers who purchased old accounts in bulk for pennies on the dollar — simply don't have the documentation. They bought a spreadsheet with names, addresses, and balances. When you ask for the original contract and payment history, they've got nothing. If they can't validate and continue trying to collect, they're breaking the law.

Scenario 4: The Account Disappears

Sometimes after receiving a validation request, the collector quietly removes the account from your credit report and moves on. They know the account won't hold up to scrutiny, and pursuing an unvalidated debt exposes them to FDCPA liability. This is the best-case scenario — the collection vanishes without you paying anything.

Common Mistakes That Weaken Your Letter

Debt validation is straightforward, but these mistakes can undermine your efforts:

- Calling instead of writing. Phone disputes don't trigger the same FDCPA protections. Always put it in writing, always send certified mail.

- Missing the 30-day window. You can still request validation after 30 days, but the collector isn't required to stop collection while they respond. Send your letter as soon as possible after first contact.

- Acknowledging the debt is yours. Don't write "I know I owe this but the amount is wrong." Simply dispute and request validation. Let them prove everything — the debt's existence, the amount, and your obligation.

- Including personal financial information. Never send bank statements, pay stubs, or your Social Security number. The collector is supposed to prove the debt to you, not the other way around.

- Sending to the wrong party. Debt validation letters go to the debt collector, not the original creditor and not the credit bureaus. If you want to dispute with the bureaus, that's a separate process under the FCRA.

- Using templates without customizing them. Generic templates pulled off the internet often include language that's outdated or doesn't apply to your situation. Tailor every letter to the specific debt and collector.

What If the Collector Violates Your Rights?

If a debt collector continues collection activity after receiving your validation request and before providing verification, they're violating the FDCPA. Here's what you can do:

- Document everything. Save every letter, record every phone call date and time, screenshot any credit report changes.

- File a complaint with the CFPB at consumerfinance.gov/complaint. The CFPB tracks these complaints and takes action against repeat offenders.

- File a complaint with your state attorney general. Many states have additional consumer protection laws beyond the FDCPA.

- Consult a consumer rights attorney. FDCPA cases are often taken on contingency because the law provides for attorney's fees — meaning it may not cost you anything upfront.

Under the FDCPA, you can recover up to $1,000 in statutory damages per lawsuit, plus actual damages (like credit score harm that cost you a higher interest rate), plus the collector's attorney's fees.

Debt Validation and Your Credit Report

Here's where validation connects directly to your credit score. If a collector can't validate a debt, they have no business reporting it to Equifax, Experian, or TransUnion. Under the FCRA, furnishers (including collectors) must report accurate information — and unvalidated information isn't accurate by definition.

After a failed validation, you can:

- Send a dispute to the credit bureaus citing the collector's failure to validate

- Include your certified mail receipt as evidence you requested validation

- Request removal of the collection account from your report

For collections that have been validated but are still hurting your score, strategies like pay-for-delete negotiations or working with a professional credit repair company can help you get them removed faster.

When Professional Help Makes Sense

Sending one debt validation letter is manageable on your own. But what about when you've got four collections, two charge-offs, a handful of late payments, and hard inquiries stacking up? Each item requires its own strategy, its own letters, its own follow-up timeline.

That's where professional credit repair comes in. At Crowned Credit, our team handles the entire dispute process — debt validation letters, bureau disputes, creditor negotiations, and follow-up — so you're not spending hours researching FDCPA timelines and tracking certified mail receipts.

We offer three plans depending on where you're at:

- Essential — $150 enrollment + $99/month for straightforward credit repair needs

- Accelerated — $249 enrollment + $199/month for more complex situations with multiple negative items

- Momentum — $1,095 one-time for a comprehensive, intensive credit overhaul

Every client gets a dedicated team that disputes strategically using your full rights under the FCRA and FDCPA. Book a free consultation to see which plan fits your situation, or call us at 336-310-0090.

Frequently Asked Questions

Can I send a debt validation letter after 30 days?

Yes. You can request validation at any time, but sending it within the initial 30-day window provides the strongest protection. After 30 days, the collector isn't required to pause collection while responding, though they should still provide verification if requested.

Does a debt validation letter work for medical debt?

Absolutely. Medical debt is one of the most common types to contain errors — incorrect billing codes, insurance payments not applied, duplicate charges. Validation is especially important for medical collections because the billing chains are so complex.

What if the debt is actually mine?

Even if you believe the debt is yours, validation protects you. The amount could be wrong, unauthorized fees may have been added, or the statute of limitations may have expired. You lose nothing by requesting validation, and you might discover the collector's claim doesn't hold up.

Can I send a debt validation letter by email?

Technically, the FDCPA doesn't prohibit electronic communication, but certified mail is the gold standard. It creates undeniable proof of delivery with a specific date, which matters if you end up in court. Email can be harder to prove was received.

Will sending a debt validation letter hurt my credit score?

No. Requesting validation is your legal right and has no direct impact on your credit score. The collection account may already be affecting your score, but the act of disputing it doesn't cause additional harm.

Disclaimer: This article is for educational purposes only and does not constitute legal advice. Under the Credit Repair Organizations Act (CROA), no company can guarantee specific credit score improvements or outcomes. Results vary based on individual credit situations. Crowned Credit helps clients exercise their legal rights under consumer protection laws, but we cannot promise specific score increases or removal of accurate information.