How to Remove Old Addresses From Your Credit Report in 2026

Ashley Rivera

Credit Repair Specialist

You pull your credit report, ready to check a collection account or a late payment, and then you notice something weird. Three old apartments. An address where you never lived. A variation of your current address with the wrong unit number. Maybe even your parents’ house from ten years ago.

At first glance, old addresses can feel harmless. They are not always harmless.

Outdated or inaccurate personal information can create real problems. It can make your file look messy, increase the odds of a mixed credit file, and make disputes harder when the bureaus try to “verify” negative accounts using bad identifying information. In some cases, wrong addresses show up alongside accounts that do not belong to you at all.

That is why people search this question so often: how do you remove old addresses from your credit report?

The short answer is yes, you can often remove addresses that are wrong, incomplete, duplicated, or no longer relevant. But you need to do it the right way. If you send a lazy online dispute with no strategy, you may just get a generic response saying the address was “verified.”

This guide walks you through exactly how to remove old addresses from your credit report in 2026, when to leave an address alone, what documents help, and how this fits into a broader credit repair strategy.

Why old addresses matter more than most people think

Credit bureaus use personal identifying information, sometimes called PII, to match accounts to your file. That includes your name, date of birth, Social Security number, and address history. When the address section gets sloppy, a few things can happen:

- Mixed file risk goes up. If you have a common name, similar address data can help the bureau merge in someone else’s information by mistake.

- Disputes get harder. Negative accounts may be “verified” against outdated address information that should not be tied to you anymore.

- Fraud red flags get missed. A wrong address can be an early sign of identity theft, synthetic identity issues, or simple reporting errors.

- Manual underwriters may notice. Lenders reviewing your report by hand do look at inconsistent personal information, especially for mortgages.

An old address by itself does not usually drop your credit score. That part matters. The address section is not a scoring factor the way payment history or utilization is. But inaccurate address data can absolutely contribute to the bigger problems that do cost you approvals, better terms, and peace of mind.

If you have not already reviewed the rest of your report, start with our guides on how to read a credit report and common credit report errors. Removing a bad address is often step one, not the whole fix.

Which addresses should you remove, and which ones should you keep?

This is where people mess up. They assume every old address should come off immediately. That is not always the smart move.

Here is a better framework.

You should usually dispute an address if it is:

- Completely unfamiliar

- Misspelled or tied to the wrong unit number

- Associated with fraudulent or unrelated accounts on your report

- A duplicate or variation of the same address

- Reported in a way that clearly conflicts with your actual identity records

You may want to leave it alone for the moment if it is:

- A real former address tied to legitimate accounts that are still reporting accurately

- Being used to help prove account history you actually want to keep

- Part of an active mortgage or loan underwriting file where changing identity details mid-process could create extra document requests

Example: if you lived at 812 Park Avenue from 2019 to 2022 and two open credit cards still show that address in their internal records, removing it from the bureau file may not be urgent. But if your report shows 821 Park Avenue, or an address in another city where you never lived, that is a very different story.

If the bad address is linked to suspicious accounts, collections, or inquiries, clean up the address section before or alongside those disputes. That removes a piece of the bureau’s verification trail.

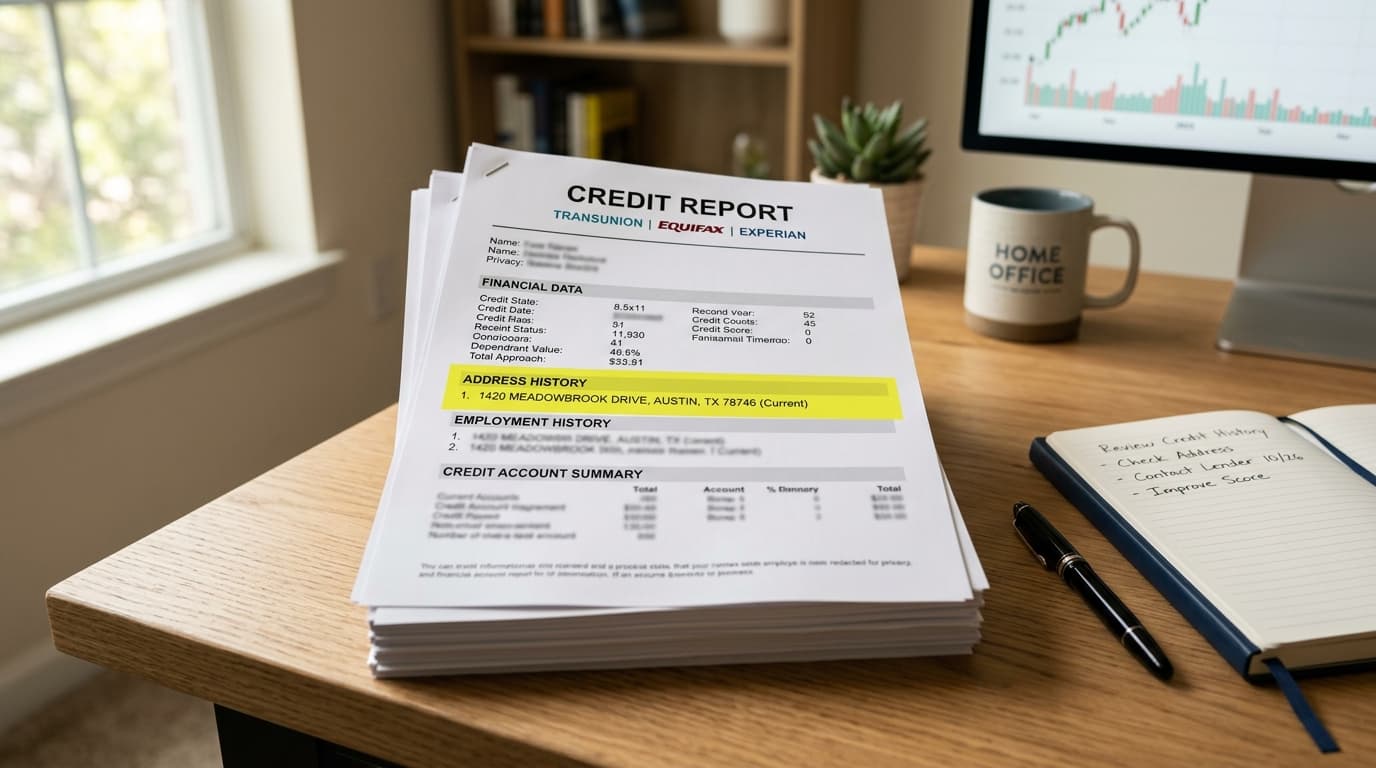

How to check all three credit reports for old addresses

Go to AnnualCreditReport.com and pull all three reports from Experian, Equifax, and TransUnion. Do not assume the address section matches across bureaus. It often does not.

Look under the personal information section for:

- Current address

- Previous addresses

- Name variations

- Employment information

Make a simple list with three columns:

- Bureau

- Address shown

- Keep, dispute, or review later

This takes ten minutes and saves a lot of confusion later. I also recommend highlighting any negative account, inquiry, or collection that appears to be tied to the wrong address. That connection matters.

Step-by-step: how to remove old addresses from your credit report

Step 1: gather proof of your current identity

Before you dispute anything, get your documents together. The credit bureaus are more likely to process a personal information update cleanly when you include proof.

Helpful documents include:

- Driver’s license or state ID

- Utility bill

- Bank statement

- Insurance statement

- Lease agreement or mortgage statement

Use copies, not originals. Make sure your current name and address are visible and consistent.

Step 2: dispute directly with each bureau showing the bad address

You need to dispute with the bureau that is reporting the incorrect address. If all three show it, dispute all three.

You can do this online, by mail, or by phone, but for address issues tied to bigger credit repair problems, written disputes are usually stronger because you control the wording and create a paper trail.

Experian: experian.com/disputes

Equifax: equifax.com

TransUnion: transunion.com

Your dispute should be short and specific. Something like this works:

Sample language:

“I am requesting the removal of the following inaccurate address from my credit file: [address]. I have never lived at this address, or this address is inaccurately reported. Please update my file to reflect only my correct address listed in the attached identification documents.”

If the address is simply outdated rather than completely wrong, you can say:

Sample language:

“This address is no longer current and should not remain as identifying information on my file. Please update my personal information to reflect my correct current address and remove the outdated address listed below.”

Be precise. List the exact address exactly as it appears on the report.

Step 3: contact the furnishers if needed

Sometimes the bureau keeps re-adding an address because a creditor or collector is still furnishing that address on active reporting. In that case, go upstream.

Call or write the creditor, debt collector, or lender that is reporting the wrong address and tell them to update your records. If they keep reporting stale data to the bureaus, the address issue may keep coming back.

This is especially common with:

- Collection agencies that bought old debt files

- Auto lenders with outdated application data

- Banks that still have an old mailing address on profile

If a collection account is tied to an address where you never lived, that is a bigger problem than just personal information. Read our guide on debt validation letters and consider disputing the account itself.

Step 4: follow up in 30 days

Under the Fair Credit Reporting Act, the bureaus generally have 30 days to investigate and respond to disputes. Check your updated reports after that window closes.

You are looking for one of three outcomes:

- Best case: the bad address is gone

- Partial win: duplicate or misspelled versions are removed, but one old address remains

- No change: the bureau says the address was verified

If nothing changes, do not just give up. Review whether the address is being tied to an active furnisher, and then send a follow-up dispute with stronger documentation or escalate through the CFPB if appropriate.

Can removing old addresses help credit repair?

Yes, but probably not in the way social media claims.

Removing old addresses is not a magic trick that adds 80 points overnight. Anyone promising that is selling nonsense. The real value is strategic:

- It can reduce mixed file issues

- It can weaken verification pathways for inaccurate negative items

- It can clean up identity data before disputing collections, charge-offs, or late payments

- It can help you spot fraud earlier

Think of it like cleaning the windshield before a long drive. It does not move the car by itself, but it makes the rest of the process clearer and safer.

At Crowned Credit, address cleanup is often part of the first pass when a client’s report shows obvious identity inconsistencies. We do not treat it as a gimmick. We treat it as file hygiene that supports the bigger dispute strategy under the FCRA.

What if the address is tied to identity theft?

If you see an address you do not recognize and it appears alongside accounts or inquiries you did not authorize, move fast.

- Freeze your credit with all three bureaus

- File an identity theft report at IdentityTheft.gov

- Dispute the fraudulent accounts and inquiries

- Request removal of the fraudulent address

- Consider adding a fraud alert

This is not just an address cleanup issue anymore. It is a fraud case.

If you need help thinking through inquiries too, our post on removing hard inquiries is worth reading next.

Common mistakes people make when disputing old addresses

- Disputing every prior address with no strategy. Some old addresses are legitimate and not worth fighting first.

- Using inconsistent documents. If your ID says one thing and your utility bill says another, expect delays.

- Ignoring the furnisher. If a creditor keeps supplying the bad address, the bureau may keep it.

- Only checking one bureau. Experian, Equifax, and TransUnion can all show different address histories.

- Expecting instant score jumps. Address cleanup supports credit repair, but it is rarely the entire solution.

If your report also shows collections, repossessions, charge-offs, or late payments, you need a full game plan. Start with our pricing page if you want to see how Crowned Credit structures help, or go straight to book a consultation if you want a human to review the file with you.

When professional help makes sense

You can absolutely dispute inaccurate addresses yourself. For a simple typo or one wrong old apartment, DIY can be enough.

But if you are dealing with any of the following, professional help can save a lot of time:

- Multiple bad addresses across all three bureaus

- Collections tied to addresses where you never lived

- Mixed file issues

- Fraudulent accounts or identity theft indicators

- Repeated “verified” responses despite clear errors

Crowned Credit handles these issues as part of a broader dispute strategy. The goal is not just to tidy your report. The goal is to challenge inaccurate, unverifiable, and misleading negative items while keeping the process compliant and documented.

Our plans are straightforward: Essential is $150 enrollment plus $99 per month, Accelerated is $249 enrollment plus $199 per month, and Momentum is a $1,095 one-time option. If you want to talk through which path fits your file, call 336-310-0090 or book your consultation here.

Final takeaway

Old addresses on a credit report are easy to ignore because they do not look dramatic. No huge balance. No scary collection amount. Just a few lines in the personal information section.

But those few lines can matter.

If an address is wrong, duplicated, unfamiliar, or tied to suspicious reporting, fix it. Clean files are easier to defend, easier to dispute, and easier to understand. And once the identity section is cleaned up, you can move on to the problems that usually do the most damage, like collections, late payments, utilization, and charge-offs.

If you want a second set of eyes on the whole report, Crowned Credit can help you sort out what is noise, what is dangerous, and what is actually worth disputing first. Book a consultation and we will walk through it with you.

Disclaimer: Individual results vary. Crowned Credit does not guarantee specific credit score increases, item removals, or timelines. Credit repair outcomes depend on the accuracy of the information reported, the documentation available, and the response of credit bureaus and furnishers. Crowned Credit works to exercise your rights under the Fair Credit Reporting Act and related consumer protection laws.