Medical Debt on Your Credit Report in 2026: What Actually Changed and What You Can Do

Ashley Rivera

Credit Repair Specialist

You went to the ER two years ago. You thought insurance covered it. Then a $3,200 bill showed up in collections — and tanked your credit score by 80 points.

Sound familiar? You're not alone. Medical debt is the single largest source of collections on American credit reports, affecting roughly 100 million people across the country. And in 2026, the rules around how that debt hits your credit are more confusing than ever.

The federal government tried to ban medical debt from credit reports entirely. A court struck that down. The credit bureaus made their own voluntary changes. And a wave of state laws is adding another layer on top of all of it.

Here's exactly where things stand right now, what's already been removed from your report, and what you can do about medical collections that are still dragging your score down.

The Big Federal Rule That Got Killed

In early 2025, the Consumer Financial Protection Bureau (CFPB) finalized a rule that would have completely banned medical bills from credit reports. The idea was straightforward: medical debt is different from other debt because you rarely choose to take it on, the billing is notoriously confusing, and it's a poor predictor of whether someone will repay a loan.

The rule never took effect. In July 2025, a federal court in Texas vacated it entirely, ruling that the CFPB exceeded its authority under the Fair Credit Reporting Act (FCRA). The court said the CFPB didn't have the power to tell credit bureaus they couldn't report this information.

So if you were counting on that federal ban to wipe medical collections off your report — it's not happening. At least not through that rule.

What the Credit Bureaus Changed on Their Own

Here's what most people miss: even without the federal rule, Equifax, Experian, and TransUnion made significant voluntary changes in 2022 and 2023 that are still in effect right now. These changes removed roughly 70% of medical collection tradelines from consumer credit reports.

Here's what the bureaus did:

- Paid medical collections are removed. If you had a medical bill go to collections and you eventually paid it off, it should no longer appear on your credit report. Before this change, paid collections stayed on your report for up to seven years.

- Medical debt less than one year old doesn't appear. The bureaus extended the waiting period from six months to a full year. So if you just received a medical collections notice, it won't show up on your credit report for at least 12 months — giving you time to sort out insurance disputes and billing errors.

- Medical collections under $500 are excluded. As of April 2023, any medical collection balance under $500 is no longer reported. This alone affected millions of consumers with smaller unpaid medical bills.

These three changes are voluntary — meaning the bureaus could reverse them — but they've been in place for over two years now and there's no indication they're going away.

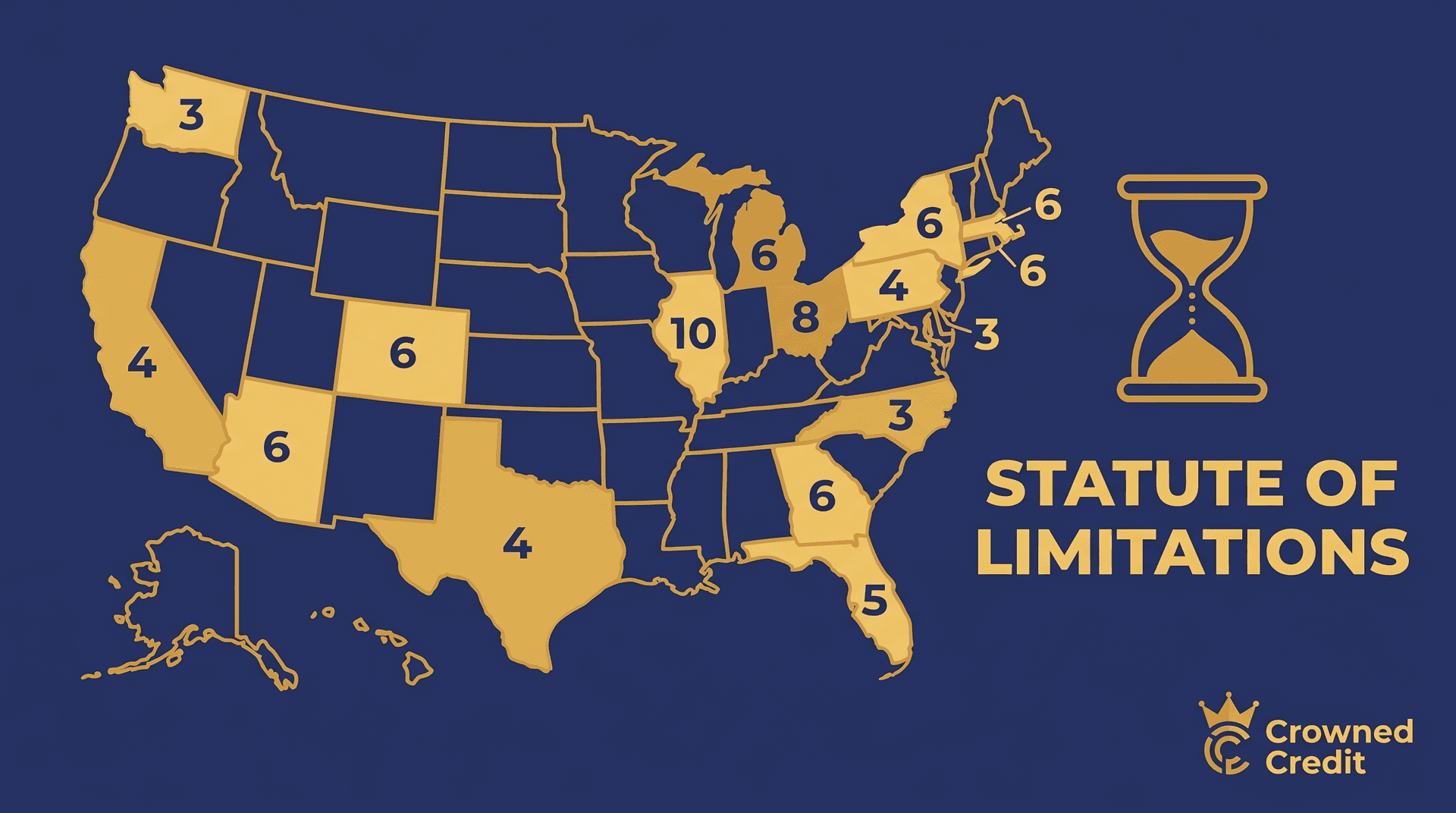

State Laws Are Filling the Gap

With the federal rule dead, states have been stepping up. As of early 2026, at least 15 states have passed their own laws restricting how medical debt can be reported on credit reports. Nine of those laws went into effect in 2025 or January 2026.

The specifics vary by state. Some ban medical debt reporting entirely. Others raise the threshold above $500 or extend the waiting period beyond one year. A few prohibit medical debt from being used in lending decisions for specific types of loans like mortgages.

If you live in a state with one of these laws, you may have additional protections beyond what the credit bureaus offer voluntarily. Check your state attorney general's website or consumer protection office to see what applies to you.

What Medical Debt Can Still Hurt Your Credit

Despite all these changes, plenty of medical debt can still appear on your credit report and damage your score. Here's what's not protected:

- Unpaid medical collections over $500 that are more than one year old. This is the big one. If you have a $2,000 hospital bill that went to collections 14 months ago and you haven't paid it, it's almost certainly on your report.

- Medical debt sold to a debt buyer. When a hospital or doctor's office sells your debt to a third-party collector, it can get murky. The collection may not even be labeled as "medical" anymore — it might just show up as a generic collection account.

- Balances that were partially paid but not fully resolved. If you made a payment plan and stopped, the remaining balance can still be reported once it goes back to collections.

And here's something critical: even when medical debt doesn't appear on your standard credit report, some specialty consumer reports (used for things like tenant screening or insurance underwriting) may still include it.

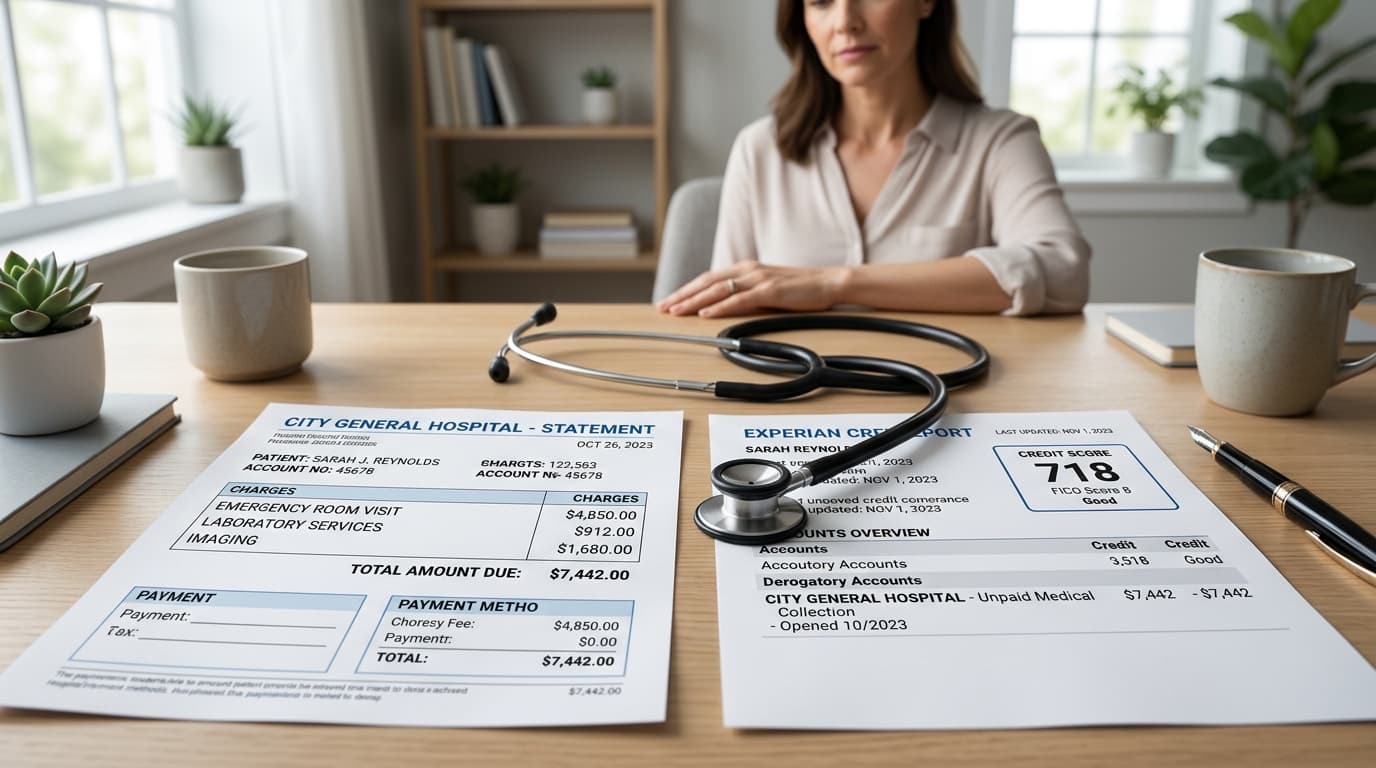

How Medical Collections Affect Your Credit Score

The impact of a medical collection on your credit score depends on your overall credit profile, but here's a rough picture:

- FICO Score 9 and VantageScore 3.0+ ignore paid medical collections entirely. If the collection is paid, these models treat it as if it doesn't exist.

- FICO Score 8 (still the most widely used model for lending decisions) does factor in unpaid medical collections, though it weights them slightly less than other types of collections.

- A single medical collection can drop a good score by 50-100 points. If you had a 720 and a medical collection hits, you could easily land in the 630-670 range — which changes the interest rates you qualify for on everything from car loans to mortgages.

The newer scoring models are more forgiving of medical debt, but most lenders — especially mortgage lenders — still use older FICO versions. So don't assume your medical collection doesn't matter just because the industry is "moving in the right direction."

5 Steps to Deal With Medical Debt on Your Credit Report

1. Pull all three credit reports and identify every medical collection

Go to AnnualCreditReport.com and pull your reports from Equifax, Experian, and TransUnion. Medical collections don't always appear on all three. Write down every medical collection: the creditor name, collection agency, balance, and date opened.

2. Verify the debt is actually yours

Medical billing errors are shockingly common. Industry analyses suggest that anywhere from 49% to 80% of medical bills contain at least one error. Common problems include being billed for procedures you didn't receive, charges that should have been covered by insurance, and duplicate billing.

Send a written debt validation letter to the collection agency within 30 days of first contact. Under the FCRA and the Fair Debt Collection Practices Act (FDCPA), they're required to provide verification of the debt — including the original creditor, the amount, and proof that you actually owe it.

3. Check if the bureaus' voluntary rules should have removed it

Cross-reference what's on your report against the current rules:

- Is the balance under $500? It shouldn't be there.

- Has the collection been paid? It shouldn't be there.

- Is the collection less than one year old? It shouldn't be there.

If any of these apply and the collection is still showing, file a dispute directly with each credit bureau reporting it. Reference their own policies — this isn't even a legal dispute at that point, it's the bureaus failing to follow their own rules.

4. Dispute inaccurate or unverifiable items under the FCRA

The Fair Credit Reporting Act gives you the right to dispute any item on your credit report that you believe is inaccurate, incomplete, or unverifiable. When you file a dispute, the credit bureau has 30 days to investigate. They contact the data furnisher (the collection agency), and if the furnisher can't verify the debt, the bureau must remove it.

Medical collections are particularly vulnerable to disputes because the chain of documentation from hospital to billing company to collection agency is long and often breaks down. (For a deeper look at the dispute process, read our guide on how to dispute errors on your credit report.) If the collection agency can't produce proper documentation linking the debt to you, it has to come off.

This is where working with a professional credit repair company can make a real difference. At Crowned Credit, we build custom dispute strategies for every client — including targeting medical collections that creditors can't properly verify. Our team understands the specific FCRA provisions that apply to medical debt and knows exactly what documentation to request.

5. Negotiate a pay-for-delete or settlement

If the debt is legitimate and verifiable, you still have options. Many collection agencies — especially those handling medical debt — will agree to a pay-for-delete arrangement, where they remove the collection from your credit report in exchange for payment (often at a reduced amount).

Get any agreement in writing before you pay a single dollar. A verbal promise means nothing. You want a signed letter on the collection agency's letterhead stating they'll request deletion from all three bureaus upon receipt of payment.

If they won't agree to deletion, negotiate the balance. Medical debt collectors typically purchase debt for 10-20 cents on the dollar. A $3,000 medical bill might settle for $600-$900. And remember — once you pay it, the bureaus' voluntary policy means it gets removed from your report anyway.

When to Get Professional Help

Dealing with medical collections on your own is possible, but it's time-consuming and easy to get wrong. A poorly worded dispute letter can actually hurt your case. And if you have multiple medical collections mixed in with other negative items like late payments or charge-offs, you need a coordinated strategy — not a one-off dispute. (Not sure if professional help is worth it? Read our breakdown of whether credit repair is worth it.)

Crowned Credit works with clients dealing with medical debt every day. Our Accelerated plan ($249 enrollment + $199/month) is popular with clients who have a mix of medical collections and other negative items because it covers disputes across all three bureaus simultaneously. For clients focused specifically on medical debt, our Essential plan ($150 enrollment + $99/month) provides a focused dispute strategy at a lower price point.

We don't just send template letters — we build cases using FCRA rights, FDCPA protections, and bureau-specific policies. Every negative item on your report gets reviewed, and we dispute strategically to maximize removals.

Disclaimer: Credit repair results vary by individual. Under the Credit Repair Organizations Act (CROA), no company can guarantee specific outcomes or promise a particular credit score increase. Crowned Credit disputes negative items on your behalf using your legal rights under the FCRA, but results depend on the specifics of your credit profile and the responses from creditors and credit bureaus.

The Bottom Line

Medical debt rules in 2026 are a patchwork. The federal ban is dead. The credit bureaus' voluntary changes help but don't cover everything. State laws vary wildly depending on where you live.

What hasn't changed: your rights under the FCRA. Every item on your credit report must be accurate, complete, and verifiable. Medical collections — with their long paper trails and frequent billing errors — are some of the most disputable items you'll find on a credit report.

If medical debt is dragging your credit score down, don't wait for the next federal rule that may or may not survive the courts. Take action now. Pull your reports, identify what shouldn't be there, and start disputing.

Or book a free consultation with Crowned Credit and let our team handle it. We'll review your credit report, identify every medical collection that can be challenged, and build a dispute strategy tailored to your situation. Call us at 336-310-0090 or schedule online.