Credit RepairMay 27, 20268 min read

VantageScore 4.0 and FICO 10T: What the 2026 Credit Score Changes Mean for You

Ashley Rivera

Credit Repair Specialist

Ashley Rivera

Credit Repair Specialist

Continue your reading with these related articles on credit repair and financial health.

If a credit bureau says an account was verified but gives you almost no detail, a method of verification letter can be the next smart move. Here is how it works in 2026.

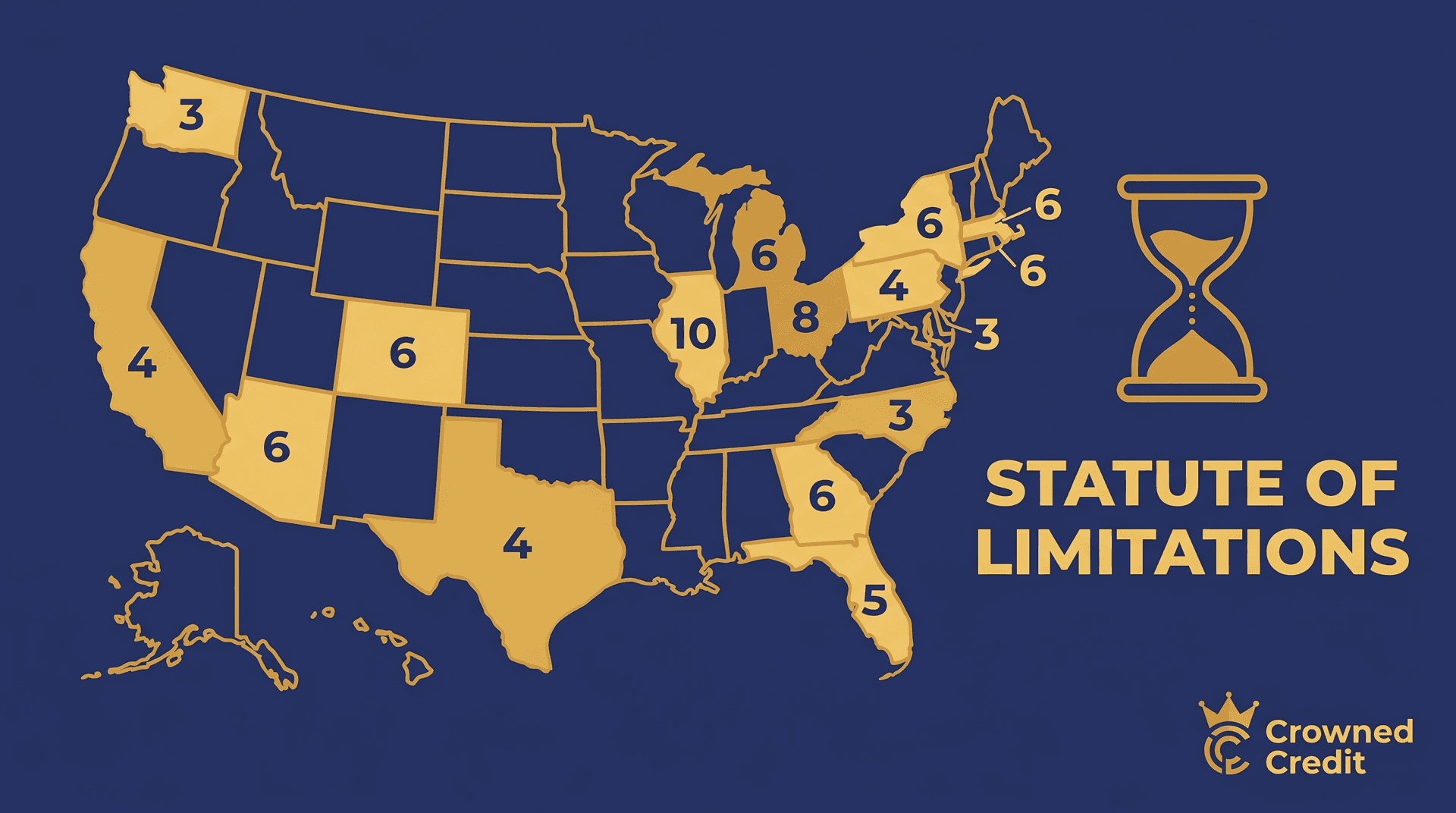

Learn your state's statute of limitations on debt in 2026, what time-barred debt means, and how expired debt still affects your credit report.

Learn how to remove collections from your credit report in 2026. Step-by-step guide covering disputes, debt validation, pay-for-delete, and expert help.

Unfamiliar collection from I.C. System, Inc. on your credit report? Discover what they are, why they are there, and how you can legally dispute and remove them in 2026.

Portfolio Recovery Associates showing up on your credit report? Here's exactly what they are, why they're there, and your real options for dealing with them.

Settled your debt but your credit took a hit? Here's the complete roadmap to rebuild your credit score after debt settlement—including realistic timelines, proven strategies, and mistakes to avoid.

Take the first step towards financial freedom today. Schedule your free consultation with our credit repair experts.