Portfolio Recovery Associates on Your Credit Report: What It Means and How to Deal With It

Ashley Rivera

Credit Repair Specialist

You pulled your credit report and there it is — Portfolio Recovery Associates listed as a collection account. Your score dropped. Now you're wondering: who are these people, do I actually owe them anything, and can I get this off my report?

The short answers: they're one of the largest debt buyers in the country, you may or may not owe what they claim, and yes — there are legitimate paths to getting this removed. Here's the full picture.

Who Is Portfolio Recovery Associates?

Portfolio Recovery Associates, LLC — commonly called PRA — is a subsidiary of PRA Group (NASDAQ: PRAA), headquartered in Norfolk, Virginia. They don't extend you credit and they didn't issue your original loan or credit card. What they do is buy old, charged-off debt from original creditors — banks, credit card companies, medical providers, utilities — for pennies on the dollar. Sometimes as little as 2–5 cents per dollar of face value.

Once they own the debt, they attempt to collect the full balance from you. That's their business model. The gap between what they paid and what you owe is their profit margin.

This matters because it changes the nature of your relationship with them. The original creditor charged your debt off and sold it. PRA is now a new party to that debt — and that has legal implications for what they can and can't do.

PRA is one of the biggest players in this space. They've also been the subject of significant regulatory action. In 2015, the Consumer Financial Protection Bureau (CFPB) hit them with an enforcement order for FDCPA and CFPA violations. Then in 2023, the CFPB went after them again — this time alleging PRA violated the 2015 order, the FCRA, and the FDCPA in connection with how they handled consumer disputes. They paid to settle. This history is relevant when you're deciding how to respond to them.

Why Portfolio Recovery Associates Is on Your Credit Report

PRA shows up on your credit report as a collection account. This happens when:

- An original creditor charged off a debt (usually after 120–180 days of non-payment)

- They sold that charged-off account to PRA

- PRA started reporting the collection to Experian, Equifax, and TransUnion

The original charge-off from the original creditor may also still appear separately on your report. This is common — and it can feel like double-dipping. Whether both can legitimately appear is something worth scrutinizing carefully, which we'll cover below.

Under the Fair Credit Reporting Act (FCRA), collection accounts can stay on your credit report for up to seven years from the date of first delinquency — not from when PRA bought the debt. This is a critical distinction. The seven-year clock started ticking when you first missed a payment to the original creditor, not when the account changed hands. If that original delinquency happened five years ago, PRA's entry only has two years left regardless of when they bought it.

How Much Damage Does a PRA Collection Do?

A collection account from Portfolio Recovery Associates can drop your credit score significantly — often 50 to 100+ points depending on where your score was before and how recently the original delinquency occurred. The newer the delinquency, the harder the hit.

Beyond the score hit, lenders see collection accounts and flag you as a higher credit risk. This affects mortgage approvals, car loan rates, credit card applications, and in some states, even rental applications and insurance premiums. A single collection can cost you thousands of dollars in higher interest rates over time.

That's why taking action matters — letting it sit there for seven years is an expensive choice.

Your Rights When PRA Comes Calling

Before you do anything, understand that you have substantial legal rights here. Two federal laws specifically govern this situation.

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA is the law that regulates how third-party debt collectors — including PRA — can contact you and pursue payment. Under the FDCPA:

- You can request debt validation. Within 30 days of PRA's first written contact, send a written validation request. They must stop collection activity until they provide proof that (a) the debt exists, (b) the amount is correct, and (c) they have the right to collect it.

- You can send a cease and desist. A written cease-and-desist letter legally requires PRA to stop contacting you. They can still sue you, but they can't call or write to collect.

- They can't harass or threaten you. No calling before 8am or after 9pm. No threats of legal action they can't legally take. No profane language or deceptive practices.

- FDCPA violations are actionable. If PRA violates the FDCPA, you can sue them in federal court and recover damages plus attorney's fees. Given their CFPB history, document every contact.

The Fair Credit Reporting Act (FCRA)

The FCRA governs what gets reported to credit bureaus and how disputes work. Under the FCRA:

- You have the right to dispute any item on your credit report. When you dispute, the credit bureau must investigate — and so must the furnisher (PRA). They must verify the accuracy of every detail: the balance, the dates, the account number, the delinquency date. Everything.

- The investigation window is 30 days (45 days if you provide supporting documentation). If they can't verify the account within that window, it must be deleted.

- Inaccurate or unverifiable items must be removed. If PRA is reporting the wrong balance, wrong dates, or anything that can't be properly verified, that's grounds for removal.

- FCRA violations also carry damages. $100–$1,000 in statutory damages per violation, plus punitive damages and attorney's fees.

Here's the thing people miss: the credit bureaus and furnishers are required to verify the information they report — every detail, upon request. If Portfolio Recovery Associates can't produce the documentation to back up what they're reporting, under the FCRA it must come off.

Step-by-Step: How to Handle Portfolio Recovery Associates

Step 1: Pull All Three Credit Reports

Get your free credit reports from AnnualCreditReport.com (the only federally mandated free source). Look at Experian, Equifax, and TransUnion separately — PRA may be reporting differently across bureaus. Note the following for each entry:

- Reported balance

- Date of first delinquency

- Account open/close dates

- Whether the original creditor is also reporting

- Any inconsistencies between bureaus

Inconsistencies across bureaus are a red flag and useful in disputes. If PRA is reporting a balance of $4,200 on Experian but $4,600 on Equifax, that's already an accuracy problem.

Step 2: Request Debt Validation

If PRA has recently contacted you (within 30 days of their first written notice), send a debt validation letter by certified mail with return receipt. Request:

- Proof they own the debt (the purchase agreement or assignment document)

- A complete payment history from the original creditor

- The original credit agreement bearing your signature

- Verification of the amount owed

Many debt buyers purchase portfolios of accounts with incomplete documentation. When they bought pennies-on-the-dollar accounts, they didn't always receive complete paper trails. If they can't produce validation, their ability to collect and report becomes legally questionable.

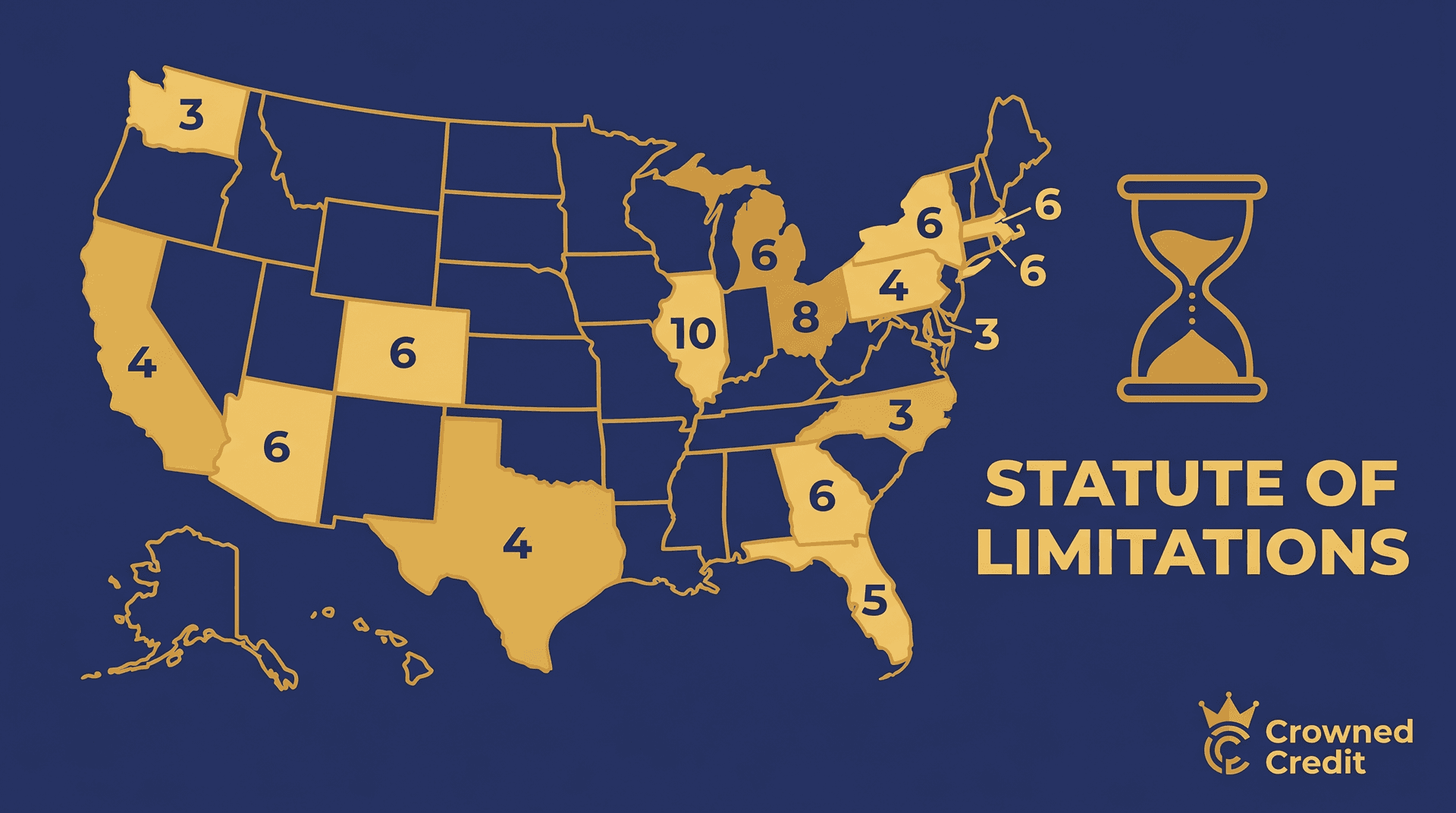

Step 3: Check the Statute of Limitations

Every state has a statute of limitations (SOL) on debt — the time window during which a creditor can sue you to collect. After this window closes, the debt is "time-barred." PRA can still try to collect and still report the debt, but they can't win in court if you raise the SOL as a defense.

State SOLs range from 3 to 6 years for most credit card and personal loan debt, though some states go higher. The SOL typically starts from the date of last activity or last payment. If your original delinquency was several years ago, look up your state's SOL for the type of debt involved before making any payment — even a partial payment or written acknowledgment of the debt can restart the clock in some states.

Step 4: Dispute Through the Credit Bureaus

File disputes with Experian, Equifax, and TransUnion. You can do this online or by certified mail (mail is recommended — it creates a paper trail). In your dispute, be specific: identify the account, state what you're disputing (accuracy of the balance, dates, ownership, the account itself), and include any supporting documentation.

The bureaus must forward your dispute to PRA, who then has 30 days to verify every detail. If they can't — or don't respond within the window — the item must be deleted. If they verify and it remains, you still have options: request the method of verification to understand exactly what they checked and how, then dispute again with additional evidence if warranted.

Step 5: Consider Pay-for-Delete

PRA's stated credit reporting policy says they will request deletion of the tradeline after an account is paid in full or settled. This is somewhat unusual for major debt buyers — many won't agree to deletion — but PRA has made this part of their public policy.

If you want to negotiate a settlement, get any agreement in writing before sending a dime. The letter should explicitly state: the settlement amount, that PRA agrees to accept this as payment in full, and that they will request deletion of the account from all three credit bureaus upon receipt of payment. Then keep your proof of payment forever.

A few important caveats here:

- Settling doesn't automatically fix your credit immediately. The deletion request takes time to process through the bureaus.

- Forgiven debt may be taxable. If PRA forgives $600 or more of debt, they may issue a 1099-C and the IRS may consider that forgiven amount taxable income. Talk to a tax professional.

- Don't pay an old time-barred debt without legal advice. In some states, payment restarts the statute of limitations.

Step 6: Dispute Directly With PRA

Beyond disputing through the bureaus, you can also dispute directly with Portfolio Recovery Associates under the FCRA. Send your dispute to:

You can find PRA's current dispute mailing address at their official disputes page: portfoliorecovery.com/contact-us/disputes. Always send by certified mail with return receipt and keep your tracking number.

Disputing directly with the furnisher (PRA) creates a parallel obligation for them to investigate and correct or delete inaccurate information. It's another pressure point and another paper trail.

When DIY Hits a Wall

Credit bureaus and debt collectors don't always play fair. You file a dispute, they "verify" in 72 hours without actually checking anything, and the account stays. This is the CFPB's documented complaint about PRA specifically — their dispute resolution practices were so bad that the bureau took enforcement action twice.

If you've disputed and PRA keeps verifying without removing the item, if the debt is old and complex, or if you're dealing with multiple derogatory accounts while trying to qualify for a mortgage or major purchase — this is when professional credit repair makes sense.

At Crowned Credit, we work through the FCRA dispute process systematically. We analyze every item on all three reports, identify what can be challenged and on what grounds, and pursue every angle — including direct furnisher disputes, method-of-verification requests, and regulatory escalations when warranted. Most of our clients are working toward real goals: buying a house, getting a better car loan, building business credit. We keep that end goal in focus throughout the process.

Our plans start at $150 setup + $99/month (Essential) and go up to $249 setup + $199/month (Accelerated) for more intensive work. We also offer a one-time Momentum plan at $1,095 for those who want a defined-scope engagement. See all plans here or book a free consultation to talk through your specific situation.

What NOT to Do When You See PRA on Your Report

A few mistakes people make that hurt them more than help:

- Don't ignore it. Collection accounts don't improve on their own. Seven years is a long time to let something drag your score down.

- Don't call them before you know your rights. Verbal conversations are harder to document. Get things in writing.

- Don't pay without a written agreement. "I'll remove it once you pay" means nothing without documentation.

- Don't make a partial payment on a time-barred debt without legal advice. In some states, this restarts the clock and revives the debt legally.

- Don't assume paying will automatically remove the account. Paid collections still appear on your credit report — the status just changes to "paid." Deletion requires an explicit agreement or a successful dispute.

The Big Picture: What This Does to Your Credit Timeline

A Portfolio Recovery Associates collection account that's, say, two years old has about five more years before it ages off your report naturally. That's five years of score suppression, higher interest rates, and tougher loan approvals. On a 30-year mortgage, even a half-point higher interest rate can cost $30,000–$60,000 over the life of the loan depending on the amount borrowed.

That's the math that makes taking action now — disputing, validating, negotiating, or getting professional help — worth the effort and cost.

If you have multiple derogatory accounts beyond just PRA, the leverage compounds. Clearing a cluster of negative items — collections, late payments, charge-offs — can have a dramatic cumulative effect on your score compared to addressing any single item in isolation. See our guide on how to remove collections from your credit report for the broader picture, or check out our full breakdown of derogatory marks and what each one actually costs you.

Final Thoughts

Portfolio Recovery Associates on your credit report is not a dead end. It's an account that can be disputed, negotiated, and in many cases removed — particularly when PRA can't fully verify what they're reporting or when their documentation from the original creditor is incomplete.

The key is approaching it strategically rather than reactively. Know your rights under the FCRA and FDCPA. Get everything in writing. Check the dates. Check the statute of limitations. And don't let seven years of score damage accumulate when there are legal tools available to address it now.

If you want help navigating this — especially if you're dealing with PRA alongside other negative items — schedule a consultation with Crowned Credit. We'll pull your reports, walk through every account, and build a specific plan for your situation. Call us at 336-310-0090 or book online.

Legal Disclaimer: Crowned Credit is a credit repair organization as defined by the Credit Repair Organizations Act (CROA). Results vary based on individual circumstances and credit history. We do not guarantee the removal of any specific item from your credit report or promise any specific improvement in your credit score. Nothing in this article constitutes legal or financial advice. Consult a licensed attorney or financial advisor for advice specific to your situation.

Share this article: