What Credit Score Do You Need to Buy a House in 2026?

Ashley Rivera

Credit Repair Specialist

You've been saving for a down payment. You found a neighborhood you love. Then your lender pulls your credit and suddenly that dream house feels a lot further away.

This happens more often than people talk about. According to the Federal Reserve Bank of New York, roughly 8.5% of mortgage applications get denied — and the number one reason is credit-related. Not income. Not the property. Credit.

So what score do you actually need? The answer depends on which loan program you're using, how much you can put down, and whether you're willing to pay higher interest for a lower score. Here's the full breakdown for 2026.

The Quick Answer: Minimum Credit Scores by Loan Type

Every mortgage program has its own threshold. Here's where things stand right now:

- Conventional loans: 620 minimum, but most lenders want 640-660+ for approval. Programs like Fannie Mae's HomeReady and Freddie Mac's Home Possible technically start at 620.

- FHA loans: 580 with 3.5% down. You can go as low as 500, but you'll need 10% down — and good luck finding a lender willing to do it.

- VA loans: No official minimum from the VA itself. In practice, most lenders set a floor between 580 and 620.

- USDA loans: 620 through most lenders, though the USDA's automated system (GUS) technically works with lower scores if the rest of your application is strong.

Those are the minimums. Meeting the minimum doesn't mean you'll get a good deal — it means you'll get through the door. The rate waiting for you on the other side? That's a different conversation.

How Your Credit Score Changes Your Mortgage Rate (With Real Numbers)

This is where the math gets painful. Based on FICO data from early 2026, here's what borrowers are paying on a 30-year fixed-rate mortgage:

- 760-850: ~7.24% APR

- 700-759: ~7.45% APR

- 680-699: ~7.56% APR

- 660-679: ~7.61% APR

- 640-659: ~7.71% APR

- 620-639: ~7.84% APR

That spread between 760 and 620 might look small — about 0.6%. It's not small at all.

On a $400,000 mortgage, the borrower at 620 pays roughly $165 more per month than the borrower at 760. Over 30 years, that's $59,274 in extra interest. That's a new car. That's four years of property taxes. That's real money disappearing because of a three-digit number.

What "Good Enough" Actually Looks Like

Let's stop talking about minimums for a second and talk about what actually gets you a competitive deal.

740+ is the magic number. At 740, you unlock the best conventional rates. You skip the pricing adjustments (called loan-level price adjustments, or LLPAs) that Fannie Mae and Freddie Mac charge borrowers with lower scores. You get more negotiating power with lenders because you're a low-risk borrower.

700-739 is still solid. You'll pay slightly more than the 740+ crowd, but most lenders will still fight for your business. The rate difference between 720 and 740 might be 0.1-0.2% — meaningful over 30 years, but manageable.

660-699 is where things get noticeably more expensive. You're still getting approved for most programs, but you're paying premium rates. If you have time before buying, even 3-6 months of credit work can push you above 700 and save you tens of thousands.

Below 660 is tough territory. FHA becomes your best bet. Conventional loans either won't approve you or will charge rates that make the payment uncomfortable. This is the range where people often rush into a purchase and regret it later when they realize how much they're overpaying each month.

The Hidden Costs of Buying With a Low Score

The interest rate is just the start. Here's what else happens when you buy with below-average credit:

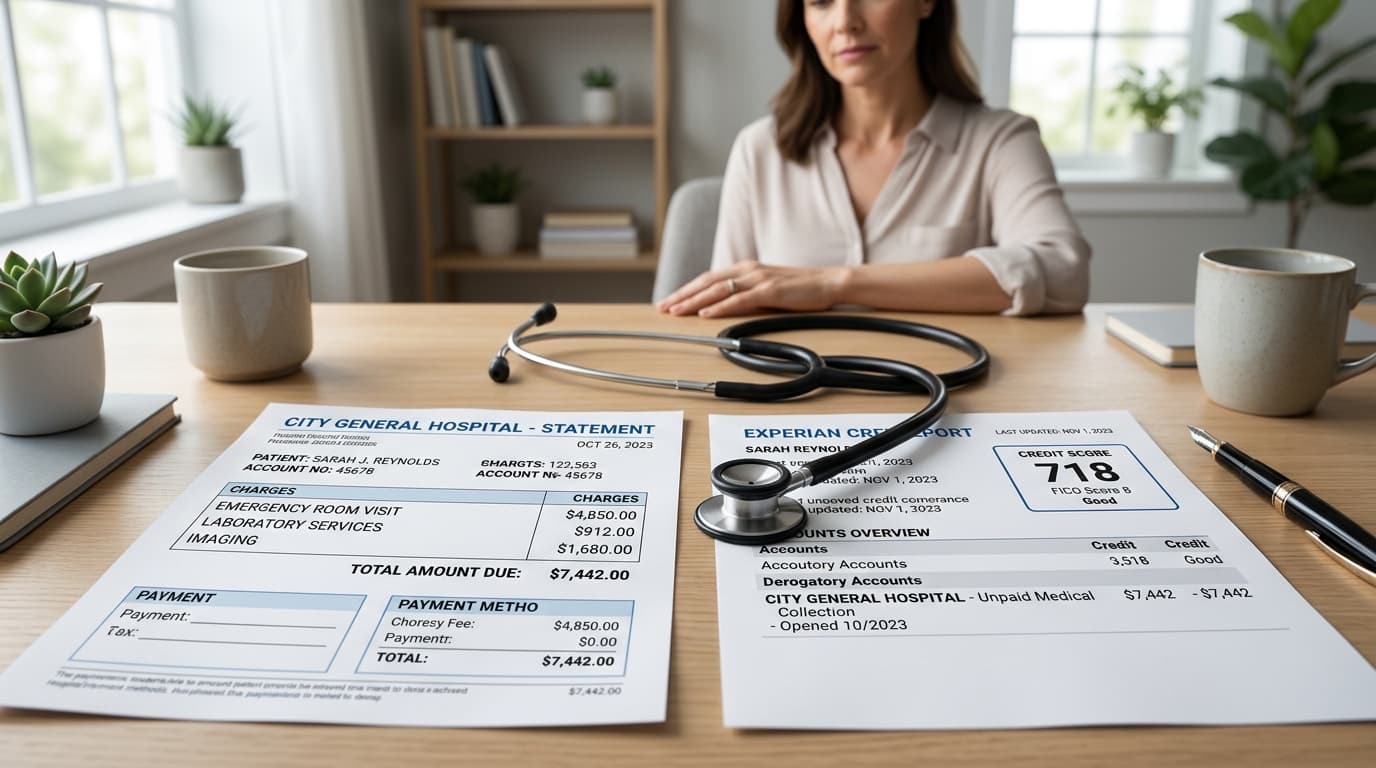

Mortgage insurance gets more expensive. With conventional loans, private mortgage insurance (PMI) is priced partly on credit score. A 640 borrower might pay 1.5% of the loan amount annually in PMI, while a 760 borrower pays 0.3%. On a $400K loan, that's $6,000/year vs. $1,200/year. FHA loans charge the same mortgage insurance premium (MIP) regardless of score — 0.55% annually for most borrowers — but you're stuck paying it for the life of the loan if you put less than 10% down.

You need a bigger down payment. Especially with FHA. Below 580, you're looking at 10% down instead of 3.5%. On a $350,000 house, that's $35,000 instead of $12,250 — an extra $22,750 you need in cash.

Sellers might skip your offer. In competitive markets, sellers and listing agents look at buyer pre-approval letters. A conventional pre-approval at 740+ signals reliability. An FHA offer from a 580-score buyer signals potential issues — appraisal requirements, longer closings, higher fall-through risk. This isn't fair, but it's reality.

FHA vs. Conventional: Which One Makes Sense for Your Score?

This decision trips up a lot of first-time buyers.

Choose FHA if:

- Your score is between 580 and 659

- You have limited savings for a down payment (3.5% minimum)

- You have a past bankruptcy or foreclosure (FHA has shorter waiting periods)

- Your debt-to-income ratio is on the higher side

Choose conventional if:

- Your score is 680 or above

- You can put 5-20% down

- You want PMI to drop off automatically at 80% loan-to-value

- You're buying a condo (many condo associations aren't FHA-approved)

The trap people fall into: getting an FHA loan when they're close to conventional territory. If you're at 610 today, it might be worth spending a few months cleaning up collections and addressing late payments to cross that 640-660 threshold where conventional loans become realistic. The lifetime savings can be massive.

How Fast Can You Improve Your Score Before Buying?

Here's what moves the needle fastest, based on what actually works in practice:

30-60 days: Quick wins

- Pay down credit card balances below 30% utilization (below 10% is even better). This alone can swing your score 20-50 points if your cards are currently maxed out. Check out our deep dive on credit utilization for the exact strategy.

- Get added as an authorized user on a family member's old, low-balance credit card. Their payment history transfers to your report.

- Dispute inaccurate negative items on your credit report. Under the Fair Credit Reporting Act (FCRA), creditors and bureaus must verify every item they report. If they can't, it gets removed.

60-120 days: Strategic cleanup

- Address collections and charge-offs through proper dispute channels. Many collection accounts have reporting errors — wrong dates, wrong balances, incomplete documentation. Each successful removal can add 15-40 points.

- Negotiate pay-for-delete agreements on smaller collection accounts.

- Open a secured credit card or credit-builder loan if you have thin credit history.

4-6 months: Full rebuild

- Establish consistent payment history across all accounts.

- Build a mix of credit types (revolving and installment).

- Continue disputing inaccurate, unverifiable, or incomplete items.

The biggest mistake people make is assuming their score is stuck. A borrower at 580 right now could realistically hit 660-680 within 3-5 months with the right approach. That jump unlocks conventional loans, better rates, and tens of thousands in savings over the life of the mortgage.

What Lenders Look at Beyond Your Score

Credit score gets all the attention, but lenders evaluate your full financial picture:

Debt-to-income ratio (DTI). Most lenders want your total monthly debt payments (including the new mortgage) to stay below 43-45% of your gross monthly income. Some FHA lenders go up to 50% with compensating factors. If your DTI is high, paying off a car loan or credit card before applying can help more than raising your score by 10 points.

Employment and income stability. Lenders typically want two years of consistent employment. Self-employed borrowers need two years of tax returns showing stable or growing income. Job-hopping within the same field is usually fine. Switching from W-2 to 1099 right before buying? That creates problems.

Down payment and reserves. More cash means less risk for the lender. Even if your score qualifies you for 3.5% down FHA, coming in with 5-10% shows financial stability and can offset credit concerns. Having 2-3 months of mortgage payments in savings (called reserves) also strengthens your application.

Credit history depth. A 680 score with 10 years of credit history looks very different from a 680 with 18 months of history. Lenders look at how long your accounts have been open, how many accounts you have, and the overall pattern of your credit behavior.

First-Time Buyer Programs You Should Know About

Several programs exist specifically to help buyers who don't have perfect credit:

- FHA 203(b): The standard FHA program. 3.5% down at 580+. Available everywhere.

- VA loans: If you're a veteran or active-duty military, this is almost always the best option. No down payment, no PMI, and competitive rates even with lower scores.

- USDA Rural Development: Zero down payment for eligible properties in designated rural areas (which includes a surprising number of suburban communities). Usually needs a 620+ score.

- State housing finance agency programs: Most states offer down payment assistance and below-market rates for first-time buyers. Income limits apply but they're higher than you'd expect — check your state's HFA website.

- Fannie Mae HomeReady / Freddie Mac Home Possible: 3% down conventional loans for borrowers earning at or below 80% of area median income. Score minimum is 620.

The Real Cost of Waiting vs. Buying Now

People ask this constantly: "Should I buy now with a lower score or wait until my credit improves?"

Here's a framework that actually helps:

Wait if: You're below 660, you have active collections or charge-offs dragging your score down, and you're not in a time-sensitive housing situation. Three to six months of focused credit work can save you $40,000-$60,000+ over a 30-year mortgage. That math is hard to argue with.

Buy now if: You're above 700, your housing costs are going to go up anyway (rent increases, lease expiring), and waiting means competing in a hotter market later. At 700+, the rate difference between now and a 740+ score is relatively small, and home price appreciation could offset it.

Get help first if: Your report has errors, unverifiable accounts, or outdated information pulling your score down. Many people are sitting at 620 when they should be at 680+ — they just haven't addressed the inaccurate items on their reports. This is exactly what credit repair professionals handle.

Under the FCRA, every item on your credit report must be accurate, timely, and verifiable. Creditors have 30 days to respond to disputes, and if they can't verify the information, it must be removed. At Crowned Credit, our team uses these rights strategically to challenge questionable items across all three bureaus — Equifax, Experian, and TransUnion. If you're planning to buy in the next 6-12 months, schedule a free consultation to see what's actually fixable before you apply.

Your Pre-Mortgage Credit Checklist

Before you talk to a lender, do this:

- Pull all three credit reports at AnnualCreditReport.com (it's the only official source — everything else charges you). Review each one carefully.

- Identify every negative item — collections, charge-offs, late payments, public records. Write them down with dates and amounts.

- Check for errors. Duplicate accounts, wrong balances, accounts that aren't yours, dates that don't match. These are more common than you'd think — the FTC found that 1 in 4 consumers had errors on their reports that could affect their scores.

- Calculate your utilization. Add up all credit card balances and divide by total credit limits. Above 30%? Pay those down before applying. This is the fastest score boost available to most people.

- Don't open new credit accounts. New inquiries and new accounts lower your average age of credit. If you're buying in the next 6 months, freeze your applications.

- Don't close old accounts. Even if you're not using them. Closing them reduces your available credit (raising utilization) and eventually shortens your credit history.

Bottom Line

You don't need an 800 to buy a house. You don't even need a 700. But the difference between buying at 620 and buying at 740 is roughly $59,000 in extra interest payments — and that number goes up with larger loan amounts.

If you're 3-6 months away from buying and your score isn't where you want it, that window is exactly enough time to make meaningful changes. Dispute inaccurate items, pay down utilization, address old collections. Every point matters when you're shopping for a 30-year financial commitment.

Need a professional assessment of your credit before you start house hunting? Crowned Credit's team analyzes all three bureau reports and builds a personalized strategy to maximize your score before you apply. Plans start at $150 enrollment with the Essential plan ($99/month), or step up to the Accelerated plan ($249 enrollment, $199/month) for faster results. Call us at 336-310-0090 or book a free consultation online.

Disclaimer: Credit repair is not guaranteed. Results vary based on individual credit profiles, the accuracy and verifiability of reported items, and creditor/bureau responses. Crowned Credit does not guarantee specific score increases or timelines. Services are provided in compliance with the Credit Repair Organizations Act (CROA) and applicable state regulations.