Credit RepairMay 21, 20268 min read

What Credit Score Do You Start With? The Truth About Your First Score in 2026

Ashley Rivera

Credit Repair Specialist

Ashley Rivera

Credit Repair Specialist

Continue your reading with these related articles on credit repair and financial health.

If a credit bureau says an account was verified but gives you almost no detail, a method of verification letter can be the next smart move. Here is how it works in 2026.

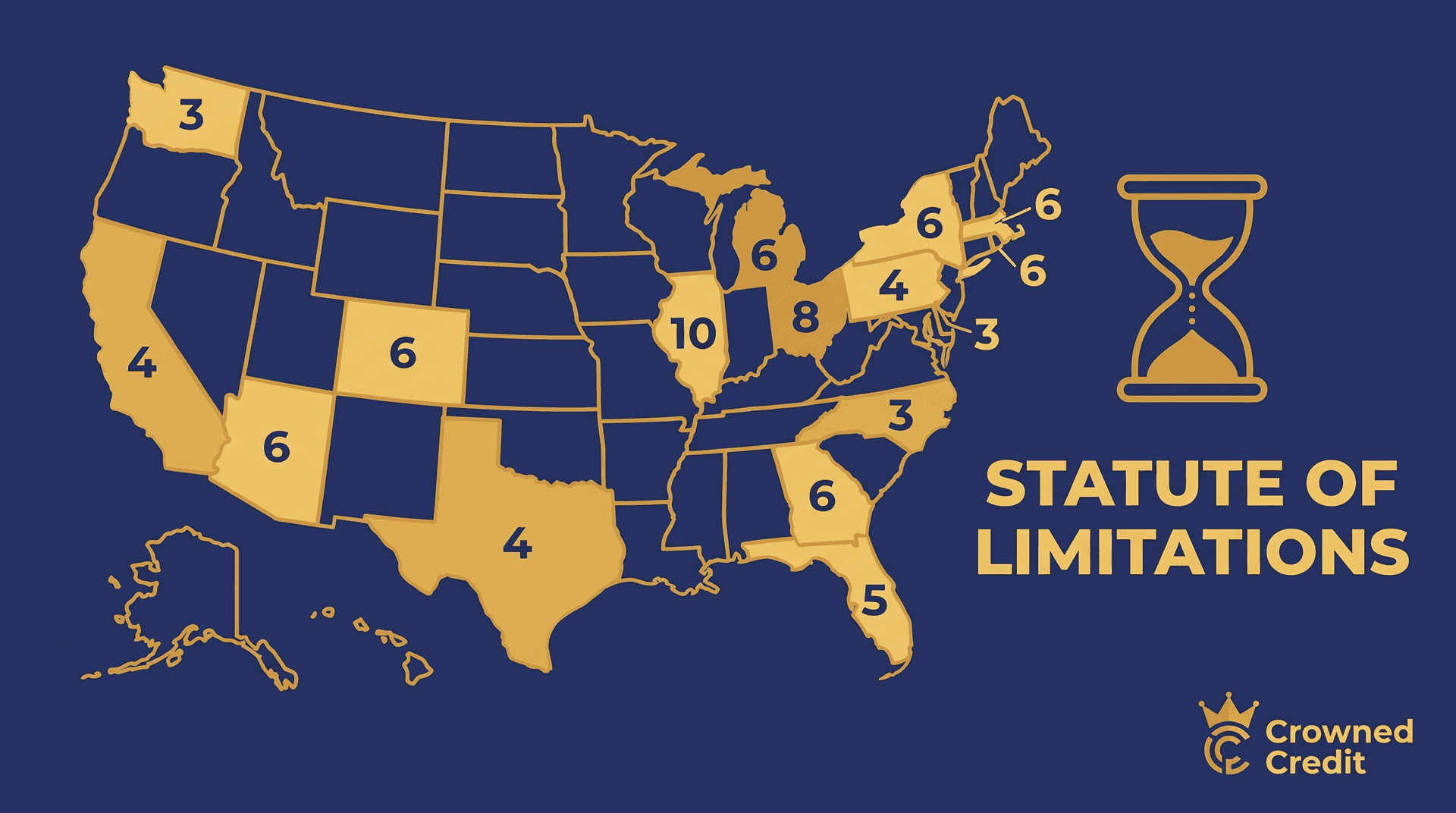

Learn your state's statute of limitations on debt in 2026, what time-barred debt means, and how expired debt still affects your credit report.

Seeing ‘account closed by credit grantor’ on your credit report can feel like a red flag. Here’s what it usually means, when it hurts, and what to do next in 2026.

VA loans do not have an official minimum credit score from the government, but lenders still set their own standards. Here is what score range usually gets you in the door in 2026.

A mixed credit file happens when someone else’s accounts or personal information end up on your credit report. Here is how to spot it, dispute it, and protect your approvals in 2026.

If a deleted account showed back up on your credit report, do not assume you are stuck with it. Here is what reinsertion means, why it happens, and what to do next in 2026.

Take the first step towards financial freedom today. Schedule your free consultation with our credit repair experts.