What Is a Good Credit Score in 2026? Ranges, Rates, and How to Improve Yours

Ashley Rivera

Credit Repair Specialist

Your three-digit credit score quietly runs your financial life. It determines whether you get approved for that apartment, how much you pay for car insurance, and whether your mortgage costs you an extra $87,000 over 30 years. Yet most Americans have no idea where they actually stand — or what "good" even means in 2026.

The average FICO score in the U.S. right now is 715, according to Experian's latest data. That puts the typical American squarely in the "good" range. But "good" and "great" are separated by real money — thousands of dollars per year in interest charges, insurance premiums, and deposit requirements.

Here's exactly where the lines fall, what each range gets you, and how to push your score higher if you're not where you want to be.

The Five FICO Score Ranges (300–850)

FICO scores — the ones used by 90% of top lenders — break down into five tiers. Each one unlocks different rates, terms, and opportunities:

- Exceptional (800–850): The top tier. You'll qualify for the lowest interest rates available and get approved almost anywhere. About 21% of Americans fall here.

- Very Good (740–799): Near-prime territory. Lenders compete for your business, and you'll get rates just slightly above the absolute best. Roughly 25% of consumers land in this range.

- Good (670–739): The average American sits here. You'll get approved for most credit products, but your rates won't be the lowest. Around 21% of the population.

- Fair (580–669): Subprime territory. You can still get approved, but expect higher rates, larger deposits, and fewer options. About 17% of consumers.

- Poor (300–579): Most traditional lenders will decline your applications. Secured cards and credit-builder loans become your main tools. Roughly 16% of Americans are here.

One thing worth noting: these ranges apply to the standard FICO Score 8 model. Some lenders use industry-specific versions (like FICO Auto Score 9 or FICO Bankcard Score 8) that range from 250 to 900. The tier names stay the same, but the cutoff numbers shift slightly.

What Your Credit Score Actually Costs You (Real Numbers)

The difference between "fair" and "excellent" credit isn't abstract. Here's what it looks like on actual loan products in April 2026:

Mortgage Rates by Credit Score

On a $350,000, 30-year fixed mortgage (based on current Experian/Curinos data):

- 760+ score: ~6.15% APR → $2,133/month → $417,880 total interest

- 700–759 score: ~6.63% APR → $2,240/month → $456,400 total interest

- 660–699 score: ~7.10% APR → $2,350/month → $496,000 total interest

- 620–659 score: ~7.72% APR → $2,505/month → $551,800 total interest

That 620-vs-760 gap? It's $372/month — $133,920 over the life of the loan. That's a college education, a rental property down payment, or a decade of vacations. All because of a number on a screen.

Auto Loan Rates by Credit Score

On a $35,000 new car loan (60 months), based on Q1 2026 Experian data:

- Super prime (781+): ~5.1% APR → $661/month

- Prime (661–780): ~6.9% APR → $693/month

- Subprime (501–600): ~12.3% APR → $786/month

- Deep subprime (300–500): ~15.5%+ APR → $844/month (if approved at all)

The subprime borrower pays $7,500 more over five years compared to the super-prime borrower — on the exact same car. Used car rates are even worse, with subprime borrowers paying 18–21% APR on average.

Insurance Premiums

We covered this in detail in our guide to credit scores and insurance rates, but the short version: drivers with poor credit pay 40–115% more for auto insurance than those with excellent credit, depending on the state. That's an extra $800–$2,000 per year in many markets.

Where Do Most Americans Actually Stand?

The national average FICO score hit 715 heading into 2026 — a slight dip from the pandemic-era peak of 717 in 2023, but still historically strong. Here's how it breaks down by age group:

- Gen Z (18–27): Average score of 680. Many are just starting to build credit history, which keeps the average lower.

- Millennials (28–43): Average around 690. Student loans, early credit mistakes, and shorter histories drag this down.

- Gen X (44–59): Average of 709. The generation most likely to carry mortgage debt and have experienced the 2008 crisis.

- Baby Boomers (60–78): Average of 745. Decades of credit history and (generally) paid-off mortgages boost these scores.

- Silent Generation (79+): Average of 760. Long histories and low utilization rates.

Geography matters too. Minnesota averages 742 (highest in the nation), while Mississippi sits at 680 (lowest). Southern and southeastern states tend to run lower, which tracks with income levels and cost-of-living differences.

The Five Factors That Build Your Score

Your FICO score is calculated from five weighted categories. Understanding them is the first step to improving your number:

1. Payment History (35% of your score)

This is the single biggest factor. One 30-day late payment can drop a 780 score by 60–100 points. A 90-day late payment or a collection account hits even harder. The good news: the impact fades over time. A late payment from three years ago matters far less than one from three months ago.

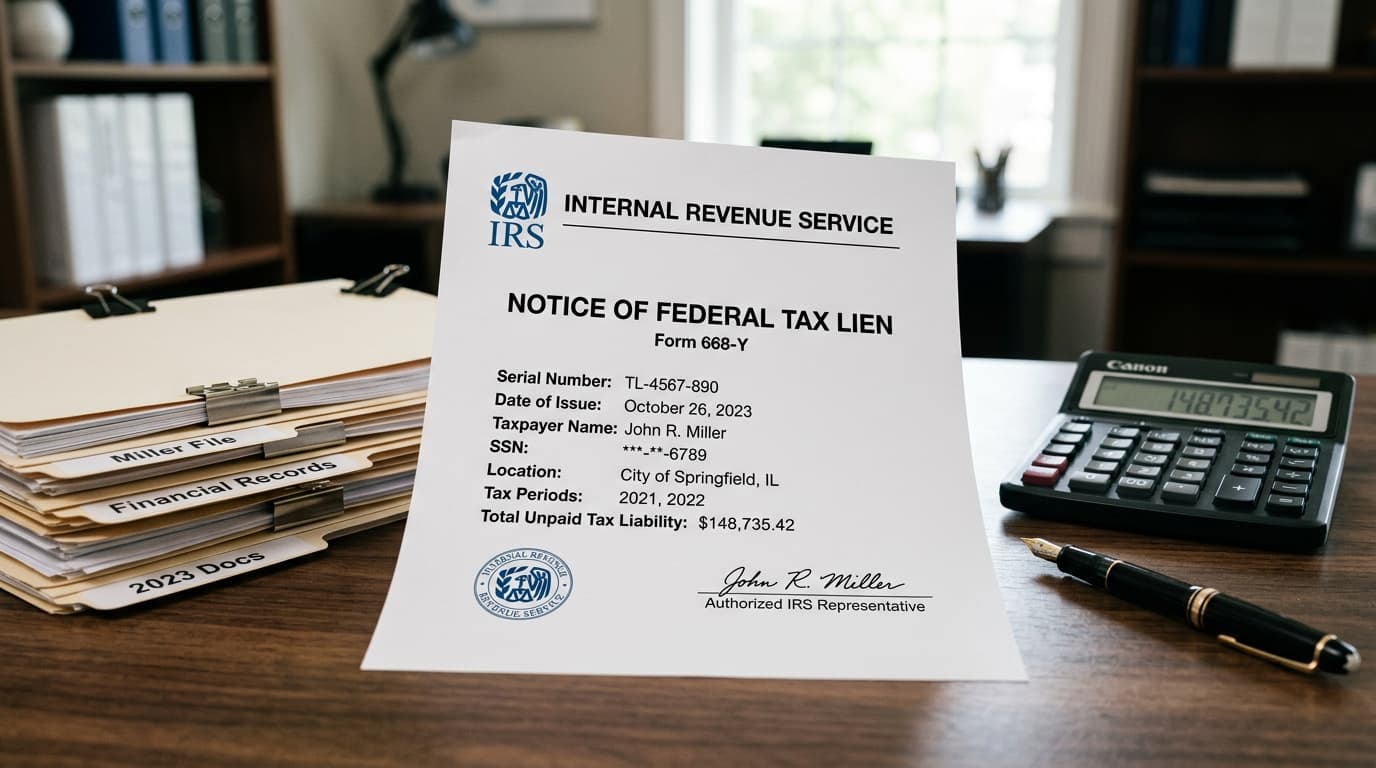

Under the Fair Credit Reporting Act (FCRA), creditors must be able to verify every item they report to the bureaus. If they can't produce documentation proving the accuracy of a late payment, it must be removed. This is one of the primary tools professional credit repair companies use — and it works because bureau reporting errors are shockingly common.

2. Credit Utilization (30% of your score)

This measures how much of your available credit you're actually using. If you have $10,000 in total credit limits and $3,000 in balances, your utilization is 30%. FICO rewards lower utilization — borrowers with 800+ scores typically keep theirs under 7%.

We wrote an entire breakdown on this: credit utilization and how to fix it. The quick version: pay balances down before your statement closing date, and request credit limit increases on existing cards.

3. Length of Credit History (15%)

Older accounts help your score. The average age of your accounts, the age of your oldest account, and how recently you've used certain accounts all factor in. This is why closing old credit cards — even ones you don't use — can actually hurt your score.

4. Credit Mix (10%)

FICO likes to see you managing different types of credit: revolving (credit cards), installment (auto loans, personal loans), and mortgage debt. Having only credit cards isn't ideal. Neither is having only installment loans. A healthy mix shows lenders you can handle different repayment structures. Our credit mix guide digs deeper into this.

5. New Credit Inquiries (10%)

Every time you apply for credit, a hard inquiry appears on your report. Each one can ding your score by 5–10 points. Multiple inquiries in a short period (except for rate-shopping on mortgages or auto loans, which FICO bundles into one) signal desperation to lenders. For strategies on removing unnecessary inquiries, check out our hard inquiry removal guide.

How to Improve Your Credit Score (Strategies That Actually Work)

If your score isn't where you need it to be, here's what moves the needle — ranked by impact:

Pay Down Credit Card Balances

This is the fastest legal way to boost your score. Paying a $3,000 balance down to $300 on a $10,000 limit card can improve your score by 30–50 points within one billing cycle. Utilization has no memory — once it drops, the score jumps immediately.

Dispute Inaccurate Negative Items

A 2023 Consumer Financial Protection Bureau study found that 1 in 5 consumers had a verified error on at least one credit report. Late payments reported on the wrong date, collections for debts that were already paid, accounts that don't belong to you — all of these can be disputed under the FCRA.

You can file disputes yourself through each bureau's online portal, or work with a professional credit repair company that knows how to build effective dispute packages. The key is understanding that under the FCRA, the burden of proof falls on the creditor — they must verify what they're reporting, or the item gets removed.

Become an Authorized User

Getting added as an authorized user on a family member's old, low-utilization credit card can add years of positive history to your report. The card's payment history, age, and utilization all get inherited by your credit profile. This strategy is perfectly legal and widely used — it's one of the fastest ways to build or rebuild credit.

Use a Secured Credit Card

If you're starting from scratch or rebuilding after a major setback, a secured card is your foundation. You deposit $200–$500, and that becomes your credit limit. Use it for small purchases, pay in full each month, and you'll build positive history fast. Most issuers will graduate you to an unsecured card after 6–12 months of responsible use. We compared the best options in our secured credit card guide.

Request a Rapid Rescore

If you're in the middle of a mortgage application and need a quick score boost, ask your loan officer about a rapid rescore. This process updates your score at the bureau level within 3–5 business days, reflecting recent payments or balance reductions that haven't hit your normal report yet.

Don't Close Old Accounts

Closing a credit card reduces your total available credit (hurting utilization) and eventually reduces your average account age (hurting history length). Even if you're not using a card, keep it open. Sock-drawer it. Set a small recurring charge on it so the issuer doesn't close it for inactivity.

When to Consider Professional Credit Repair

DIY credit repair works for some people — especially if you only have one or two simple errors to fix. But if you're dealing with multiple collections, charge-offs, late payments, or identity theft damage spread across all three bureaus, the process gets complex fast.

Professional credit repair companies handle the entire dispute cycle: pulling your reports, identifying every disputable item, building strategic dispute packages, tracking responses, and escalating with the bureaus and creditors when verification fails. They understand the nuances of FCRA, FDCPA, and state-specific consumer protection laws that most people don't.

At Crowned Credit, we take a strategic approach to every client's file. Our team reviews your full credit profile, identifies items that creditors may not be able to verify under the FCRA, and builds customized dispute campaigns targeting all three bureaus simultaneously. We offer three plans depending on your situation:

- Essential Plan: $150 enrollment + $99/month — ideal if you have a moderate number of negative items and want steady progress.

- Accelerated Plan: $249 enrollment + $199/month — for clients with more complex files who need aggressive disputing across multiple fronts.

- Momentum Plan: $1,095 one-time payment — our most comprehensive option, designed for clients who want everything handled upfront.

You can call us at 336-310-0090 or book a free consultation to see where you stand and what's realistically possible for your specific situation.

Disclaimer: Credit repair results vary by individual. No company can guarantee specific score improvements or timelines. Under the Credit Repair Organizations Act (CROA), we cannot promise to remove accurate, verifiable information from your credit report. Results depend on your unique credit profile, the nature of the items being disputed, and the responses from creditors and credit bureaus.

What Score Do You Actually Need?

The "right" score depends entirely on what you're trying to do. Here's a quick reference:

- Renting an apartment: Most landlords want 620+, competitive markets push that to 700+. Full details in our apartment credit score guide.

- Buying a car: You can get approved with a 500+, but you'll pay 15%+ interest. Aim for 700+ to get reasonable rates. See our car buying score breakdown.

- Buying a house: FHA loans accept 580+ (with 3.5% down), conventional loans typically want 620+. For the best rates, you need 740+. Our home buying guide covers every loan type.

- Getting a business loan: SBA loans generally want 680+, conventional business loans want 700+.

- Premium rewards credit cards: 740+ for the best cards (Chase Sapphire Reserve, Amex Platinum, etc.).

The Bottom Line

A "good" credit score in 2026 is 670–739 — but good isn't great, and great saves you real money. The difference between a 650 and a 750 can mean $130,000+ in extra mortgage interest, thousands more in car loan costs, and hundreds per year in higher insurance premiums.

If your score isn't where you need it, the fastest path depends on what's dragging it down. High utilization? Pay it down and watch the score jump within weeks. Negative items from collections, charge-offs, or late payments? Those need to be disputed strategically — either on your own or with professional help.

Check your score for free at AnnualCreditReport.com, then make a plan. And if your report is a mess and you don't know where to start, talk to our team. We'll tell you exactly what we see and what we can do about it — no pressure, just straight answers.