How to Write a Goodwill Letter That Actually Gets Late Payments Removed (2026 Guide)

Ashley Rivera

Credit Repair Specialist

You paid late — once, maybe twice — and now a single missed payment is dragging your credit score down by 50, 80, even 100 points. You've since caught up. The account is current. But that late mark? It's sitting on your credit report like a stain, and it'll stay there for seven years unless you do something about it.

A goodwill letter is one of the simplest tools you can use to fix this. It's a written request to your creditor asking them to remove the late payment from your credit report as a gesture of goodwill. No legal threats. No disputes. Just a polite, strategic ask — and it works more often than most people think.

This guide covers exactly how to write a goodwill letter that gets results, when to send one, who to send it to, and what to do if it doesn't work.

What Is a Goodwill Letter?

A goodwill letter is a formal request sent to a creditor or lender asking them to remove a negative item — usually a late payment — from your credit report. Unlike a credit report dispute, you're not claiming the information is wrong. You're acknowledging the late payment happened and asking the creditor to remove it anyway, as a courtesy.

Here's the key distinction:

- Dispute: "This late payment is inaccurate. I paid on time, and I have proof."

- Goodwill letter: "I did pay late, but I've been a loyal customer since then. Would you consider removing it?"

Creditors aren't legally required to honor goodwill requests. But many do — especially when the customer has an otherwise strong payment history, the late payment was isolated, and the account is now in good standing.

Why Goodwill Letters Work

This surprises people, but creditors have full authority to update what they report to the credit bureaus. Under the Fair Credit Reporting Act (FCRA), creditors must report accurate information, but nothing in the law prevents them from choosing to remove a negative mark if they want to. It's entirely at their discretion.

From the creditor's perspective, keeping a good customer happy has real business value. If you've been paying on time for 18 months since one late payment, removing that mark costs them nothing — and it keeps you loyal. That's the leverage you're working with.

Some creditors have formal goodwill adjustment policies. Others handle it case by case. A few — mostly the very largest banks — have blanket policies against goodwill removals. But you won't know unless you ask.

When a Goodwill Letter Has the Best Chance of Working

Not every situation is a good fit for a goodwill letter. Your chances are highest when:

- You have only one or two late payments on the account. A single 30-day late looks very different from six months of missed payments. Creditors are far more willing to forgive an isolated slip.

- The account is current and in good standing. If you're still behind, a goodwill letter won't help. Bring the account current first.

- You have a long history with the creditor. Five years of on-time payments and one late? That's a strong case. Three months into a new account? Not so much.

- You had a legitimate reason for paying late. Job loss, hospitalization, a death in the family, military deployment — these resonate. "I forgot" is weaker but can still work if the rest of your case is solid.

- Some time has passed since the late payment. Asking six months to a year later (with perfect payments since) is the sweet spot. Asking the week after you paid late feels premature.

When a Goodwill Letter Probably Won't Work

Be realistic about your odds. A goodwill letter is unlikely to succeed if:

- You have multiple late payments across several accounts

- The account went to collections or was charged off

- You're asking the credit bureau instead of the original creditor (bureaus can't make goodwill adjustments — only the creditor who reported the information can)

- You've already disputed the same item and lost

For charge-offs and collections, you'll typically need a more comprehensive approach. A charge-off removal strategy or collections dispute process under the FCRA may be more effective.

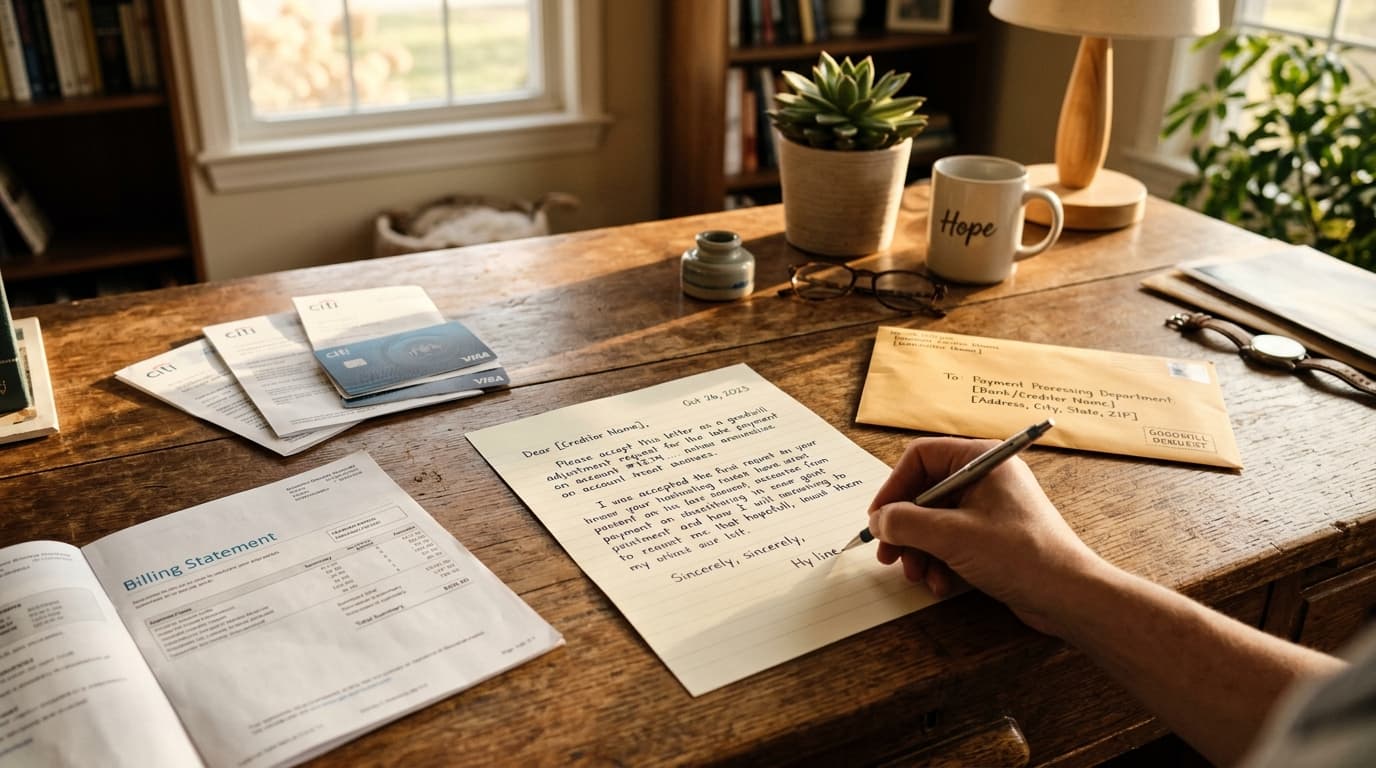

How to Write a Goodwill Letter: Step by Step

Your goodwill letter needs to hit four things: acknowledge the late payment, explain what happened, show what's changed, and make the ask. Keep it to one page. Creditors process thousands of these — respect their time.

1. Start With Your Account Information

At the top of your letter, include:

- Your full legal name

- Your account number

- Your address

- The date

This ensures your letter gets routed to the right department and matched to your account without any back-and-forth.

2. Acknowledge the Late Payment

Don't dance around it. State clearly that you know a late payment was reported and that you understand it was accurate. This isn't a dispute — you're not challenging the information. Creditors respond better when you take responsibility upfront.

3. Explain the Circumstances

Be honest but concise. What caused the late payment? A few examples:

- "I was hospitalized for two weeks in March 2025 and missed my billing cycle."

- "I was laid off from my job in January and fell behind while transitioning to new employment."

- "I switched bank accounts and my autopay didn't transfer correctly."

- "I was dealing with a family emergency and the payment slipped through the cracks."

You don't need documentation at this stage (it's not a formal dispute), but a believable, specific explanation carries weight.

4. Highlight Your Track Record

This is where you make your case. Mention how long you've been a customer, how many on-time payments you've made since the late one, and your current account status. Numbers matter here:

- "I've been a cardholder since 2019 and have made 71 consecutive on-time payments before and after this incident."

- "Since the late payment in April 2025, I've made 11 consecutive on-time payments."

5. Make the Ask

Be direct. Ask the creditor to remove the late payment from your credit report as a goodwill adjustment. Don't use legal threats, don't cite laws, and don't imply you'll take your business elsewhere. Goodwill letters work because they're polite and genuine — not because they're aggressive.

Goodwill Letter Template

Here's a template you can customize. Replace the bracketed sections with your information:

[Your Name]

[Your Address]

[City, State, ZIP]

[Date]

[Creditor Name]

[Creditor Address]

[City, State, ZIP]

Re: Account #[XXXX] — Goodwill Adjustment Request

Dear [Creditor Name] Customer Service,

I'm writing to request a goodwill adjustment on my account ending in [last 4 digits]. In [month/year], a [30/60/90]-day late payment was reported to the credit bureaus. I want to acknowledge that this reporting was accurate — I did miss the payment deadline.

At the time, [brief explanation of circumstances — e.g., "I was recovering from an unexpected medical procedure and fell behind on several bills during that period"]. Since then, I have [describe your corrective actions — e.g., "set up automatic payments and have not missed a single payment in the 14 months since"].

I've been a [Creditor Name] customer since [year] and value my relationship with your company. This late payment was an isolated incident that doesn't reflect my typical payment behavior.

I'm respectfully asking if you would consider removing the late payment notation from my credit report as a goodwill gesture. This adjustment would make a meaningful difference in my ability to [specific goal — e.g., "qualify for a mortgage for my family" or "refinance my auto loan at a better rate"].

Thank you for your time and consideration. I can be reached at [phone number] or [email] if you need any additional information.

Sincerely,

[Your Name]

Where to Send Your Goodwill Letter

This is where a lot of people go wrong. Sending your letter to the right place matters as much as what it says.

- Don't send it to the credit bureaus. Experian, Equifax, and TransUnion can't make goodwill adjustments. They only report what creditors tell them.

- Send it to the creditor's executive office or customer relations department. The generic customer service address works, but executive offices tend to have more authority to approve these requests.

- Try both mail and email. Some creditors accept goodwill requests through their secure messaging portals. A physical letter via certified mail creates a paper trail.

- Follow up by phone. Call the creditor 10-14 days after sending your letter. Ask to speak with a supervisor if the first representative can't help.

Creditors Known for Accepting Goodwill Adjustments

Based on consumer reports and credit forums, some creditors have better track records than others:

- More likely to approve: American Express, Discover, USAA, Navy Federal, smaller credit unions, local and regional banks

- Sometimes approve: Capital One, Citi, Wells Fargo, Bank of America

- Rarely approve: Chase, Synchrony Financial (though individual results vary)

These aren't guarantees — just patterns. Your specific account history, the representative you reach, and how you frame your request all influence the outcome. It's always worth trying regardless of the creditor.

What to Do If Your Goodwill Letter Gets Denied

A denial isn't the end of the road. You have several options:

Send Another Letter

Seriously. Some people get approved on their second or third attempt. Different representatives review these requests at different times. Wait 30-60 days and try again — potentially with a slightly different angle or updated payment history.

Call and Ask Verbally

Phone calls can work when letters don't. You can gauge the representative's receptiveness in real time, adjust your pitch, and escalate to a supervisor if needed. Be patient and polite — the person on the phone didn't put the late payment on your report.

File a Formal FCRA Dispute

If the goodwill approach doesn't work, switch strategies. Under the FCRA, you can dispute any item on your credit report that the creditor cannot fully verify. When you file a dispute, the credit bureau must investigate within 30 days. If the creditor can't verify the late payment with complete documentation — exact dates, amounts, account details — the bureau must remove it.

This is where many consumers find success, especially with older late payments where the original creditor may not have complete records readily available.

Get Professional Help

If you've got multiple late payments, collections, charge-offs, or other negative items dragging your score down, a goodwill letter alone probably isn't enough. A credit repair company can review your full credit profile and build a strategy that addresses everything at once — not just one late payment.

At Crowned Credit, we handle the entire dispute process for our clients using FCRA rights, direct creditor negotiations, and strategic dispute methods. Our team reviews your credit reports line by line and challenges every negative item that can be disputed — including late payments, collections, charge-offs, and more.

*Results vary by individual. Credit repair involves challenging negative items using consumer rights under federal law, including the Fair Credit Reporting Act. No company can guarantee specific credit score improvements or removal of accurate, verifiable information.*

Goodwill Letters vs. Other Removal Methods

A goodwill letter is just one tool. Here's how it compares:

- Goodwill letter: Best for isolated late payments on otherwise-good accounts. You're asking nicely, not disputing accuracy.

- FCRA dispute: Best when information may be inaccurate, incomplete, or unverifiable. The bureau must investigate and remove items they can't confirm.

- Pay-for-delete negotiation: Best for collections accounts where you offer payment in exchange for removal.

- Section 609 request: An information request under the FCRA asking the bureau to provide their documentation on a specific item. If they can't produce it, you have grounds for a dispute.

The most effective credit repair strategies combine multiple methods. A goodwill letter might handle one late payment, while FCRA disputes tackle the rest of your report.

How a Late Payment Removal Affects Your Score

Payment history accounts for 35% of your FICO score — more than any other factor. Removing even one late payment can produce a noticeable score jump, though the exact impact depends on your overall credit profile.

Some rough benchmarks:

- One 30-day late removed from an otherwise clean report: 40-80 point increase

- One 60-day late removed: 50-90 point increase

- One 90-day late removed: 60-110 point increase

- Multiple late payments removed across accounts: 100+ point increase possible

If you're sitting at a 620 and need a 680 to qualify for a mortgage, removing a single late payment could close that gap entirely. That's why this matters — the financial impact of a higher credit score can be worth tens of thousands of dollars in lower interest rates over the life of a loan.

Common Mistakes to Avoid

After helping thousands of clients clean up their credit reports, we've seen every version of this process go wrong. Here's what to watch for:

- Sending the letter to the credit bureau. This is the #1 mistake. Credit bureaus don't make goodwill adjustments — only creditors can.

- Being hostile or threatening. The moment you threaten legal action or mention an attorney, you've left goodwill territory. If you want to go that route, file a formal dispute instead.

- Using a generic template without customizing it. Creditors see hundreds of these. A letter that clearly references your specific account, dates, and circumstances stands out from obvious copy-paste templates.

- Giving up after one try. One rejection doesn't mean the door is closed. Different reps, different days, different outcomes.

- Lying about the reason. If the creditor checks and your story doesn't hold up, you've lost all credibility. Honesty is your best strategy here.

Taking the Next Step

If you have one or two late payments on an otherwise solid credit history, a goodwill letter is absolutely worth trying. It costs you nothing but time, and the potential payoff — a 50-100+ point score increase — can change what you qualify for.

But if your credit report has multiple negative items — collections, charge-offs, multiple late payments, excessive inquiries — a single goodwill letter won't move the needle enough. You need a comprehensive strategy that leverages your full rights under the FCRA.

That's exactly what we do at Crowned Credit. Our team reviews your credit reports across all three bureaus, identifies every item that can be challenged, and handles the dispute process from start to finish. Plans start at $150 setup + $99/month, and we offer a free consultation to walk through your specific situation.

Book your free credit consultation here or call us at 336-310-0090.

*Credit repair results vary by individual. Crowned Credit disputes negative items on behalf of clients using their legal rights under the Fair Credit Reporting Act (FCRA). We cannot guarantee specific score increases or the removal of any particular item. The Credit Repair Organizations Act (CROA) requires this disclosure.*