LVNV Funding LLC on Your Credit Report: What It Is and How to Remove It

Ashley Rivera

Credit Repair Specialist

You're checking your credit report and there it is: LVNV Funding LLC. Maybe it's a name you've never heard. Maybe you have no idea what debt it's attached to. And almost certainly, it's dragging your score down at exactly the wrong moment — right when you're trying to buy a house, get a car, or rent an apartment.

Here's what you need to know: LVNV Funding is one of the largest debt buyers in the country. They purchased your old debt from a creditor, and now that collection account is sitting on your report. But appearing on your credit report doesn't mean it stays there forever — and it doesn't mean you're out of options.

This guide covers what LVNV Funding actually is, why it showed up on your report, and every realistic path to getting it removed.

What Is LVNV Funding LLC?

LVNV Funding LLC is a debt purchasing company based in Greenville, South Carolina. They don't lend money or issue credit cards — their entire business model is buying charged-off debts from original creditors for cents on the dollar, then collecting the full balance from consumers.

LVNV operates under the umbrella of Resurgent Capital Services, which is part of the Sherman Financial Group. Resurgent is typically the company that actually contacts you — LVNV holds the debt, Resurgent tries to collect it. You might see both names on your credit report or in collection letters.

The debts they buy come from everywhere:

- Credit cards (Capital One, Citi, Synchrony, Discover)

- Personal loans and installment loans

- Retail store credit accounts

- Medical debt and utility accounts

- Auto loan deficiencies

Most of this debt is old — 2, 3, sometimes 5+ years past the original delinquency. LVNV buys portfolios of these accounts in bulk. By the time they show up on your report, the original creditor has long since written off the debt and sold it. The records are often incomplete, which matters a lot when it comes to your dispute options.

Why Does LVNV Funding Appear on Your Credit Report?

When you default on a debt and the original creditor charges it off, they have two choices: keep trying to collect it in-house or sell it. Most large lenders sell delinquent accounts to debt buyers like LVNV. When LVNV purchases your debt, they become the new owner and can report the collection account to all three credit bureaus — Experian, Equifax, and TransUnion.

This means you might see two separate negative entries from the same original debt:

- The original charged-off account from your creditor (e.g., "Capital One — Charged Off")

- A collection account from LVNV Funding LLC

Both entries can stay on your credit report for 7 years from the original delinquency date — meaning the date you first missed the payment that led to the charge-off. The clock doesn't restart when LVNV buys the debt. If the original account went delinquent in 2021, both entries should fall off by 2028 regardless of when LVNV acquired it.

If LVNV is reporting a delinquency date that's newer than the original creditor's date, that's a red flag worth disputing immediately. Debt re-aging — artificially extending how long a negative item appears — is illegal under the FCRA.

How Much Does LVNV Funding Hurt Your Credit Score?

A lot. Collection accounts are among the most damaging items on a credit report, second only to bankruptcy. A single collection account can drop a good credit score by 50-100 points or more. The exact hit depends on:

- Your starting score: Higher scores drop further when a collection appears

- The account balance: Larger balances tend to carry more weight

- How recent it is: A collection from last year hurts more than one from five years ago

- Which scoring model is being used: FICO 9 and VantageScore 4.0 ignore paid collections, but many lenders still use older models that don't

The impact doesn't just affect your score. Lenders can manually review your report and decline you specifically because of a collection — even if your score technically qualifies. Many mortgage underwriters, for example, require collections to be resolved before closing. If you're trying to buy a home, an LVNV account can derail the entire process.

Your Rights Under Federal Law

Before you do anything, understand what the law gives you. Two federal statutes protect consumers dealing with debt collectors and credit reporting errors:

The Fair Debt Collection Practices Act (FDCPA)

LVNV and Resurgent are debt collectors subject to the FDCPA. Under this law, they must:

- Send you written notice of the debt within 5 days of first contacting you

- Stop collection activity if you request debt validation in writing within 30 days

- Honor cease-and-desist letters for communication

- Refrain from harassment, false statements, and unfair practices

If they violate the FDCPA, you can sue them in federal or state court for actual damages, statutory damages up to $1,000, and attorney's fees.

The Fair Credit Reporting Act (FCRA)

The FCRA gives you the right to dispute any information on your credit report. Critically, the FCRA places the burden of verification on the furnisher — LVNV must be able to prove that every piece of information they're reporting is accurate and verifiable. If they can't, the credit bureaus are required to remove it.

This is key: you're not limited to disputing only "wrong" information. Under the FCRA, any information that cannot be verified must be deleted. With debt buyers like LVNV — who often have incomplete records from the original creditor — this matters more than people realize.

How to Remove LVNV Funding from Your Credit Report

There are several legitimate strategies. The right approach depends on your situation — how old the debt is, whether you can afford to pay, and what your goal is.

1. Send a Debt Validation Letter

Your first move should almost always be a debt validation letter. Under the FDCPA, LVNV must provide documentation proving:

- They own the debt (chain of title from original creditor)

- The amount owed is accurate

- You are the person responsible for the debt

Debt buyers frequently purchase accounts with minimal documentation — sometimes just a spreadsheet with account numbers and balances. If LVNV can't produce a proper account agreement, payment history, and assignment documentation, they have a problem.

Send your validation letter via certified mail with return receipt to Resurgent Capital Services (LVNV's servicer). Keep copies of everything. If they fail to validate and continue collection activity, that's an FDCPA violation.

2. Dispute Directly with the Credit Bureaus

You can file disputes with Experian, Equifax, and TransUnion directly. Each bureau will contact LVNV and ask them to verify the account within 30 days. If LVNV can't verify — or fails to respond — the bureau must remove the entry.

When disputing, be specific. Don't just say "this isn't mine." If there's an inaccurate balance, wrong date, account number discrepancy, or if you've moved the debt beyond the reporting period — cite it. You can also use a method of verification letter to find out exactly what documentation LVNV submitted.

Dispute all three bureaus simultaneously. LVNV may report slightly different information to each one, and sometimes only one or two bureaus remove the account.

3. Negotiate a Pay for Delete

If the debt is valid and within the statute of limitations, you can try to negotiate a pay for delete agreement. This means offering to pay all or part of the debt in exchange for LVNV deleting the collection account from your credit report.

LVNV/Resurgent is actually one of the more negotiable debt buyers for this strategy. They often accept settlements well below the full balance — sometimes 40-60 cents on the dollar — because they paid pennies for the debt to begin with. Starting offers of 30-40% are not unreasonable.

Important: Get any pay-for-delete agreement in writing before sending a single dollar. Verbal agreements are worthless. The written agreement should specifically state that LVNV will request deletion of the tradeline from all three bureaus upon payment. Once you pay and they delete, that collection entry is gone.

4. Goodwill Deletion Request

If you've already paid the debt and it's still showing on your report, you can try a goodwill letter requesting removal. Paid collections are treated more favorably by newer scoring models, but many lenders still see a paid collection and hesitate. A goodwill deletion request appeals to LVNV's discretion to remove accurate-but-paid negative information.

This works less reliably than the other options — especially with debt buyers vs. original creditors — but it costs nothing to try after payment.

5. Wait for Natural Expiration

If the original delinquency date is more than 6 years old, it may make more sense to wait it out. The entry will fall off automatically at the 7-year mark. Paying an old, nearly-expired debt can sometimes trigger updates to the account that make it more visible in the short term — though this doesn't restart the 7-year clock.

Check the original delinquency date on your full credit report from AnnualCreditReport.com. If LVNV is showing a more recent date than the original creditor, that needs to be disputed as re-aging.

What NOT to Do

A few traps that can make your situation worse:

- Don't acknowledge the debt verbally or in writing before you've decided your strategy. In some states, acknowledging a debt or making a partial payment can restart the statute of limitations for lawsuits.

- Don't pay without a written agreement if you're doing pay for delete. Payment without an agreement just means you paid and the collection entry stays.

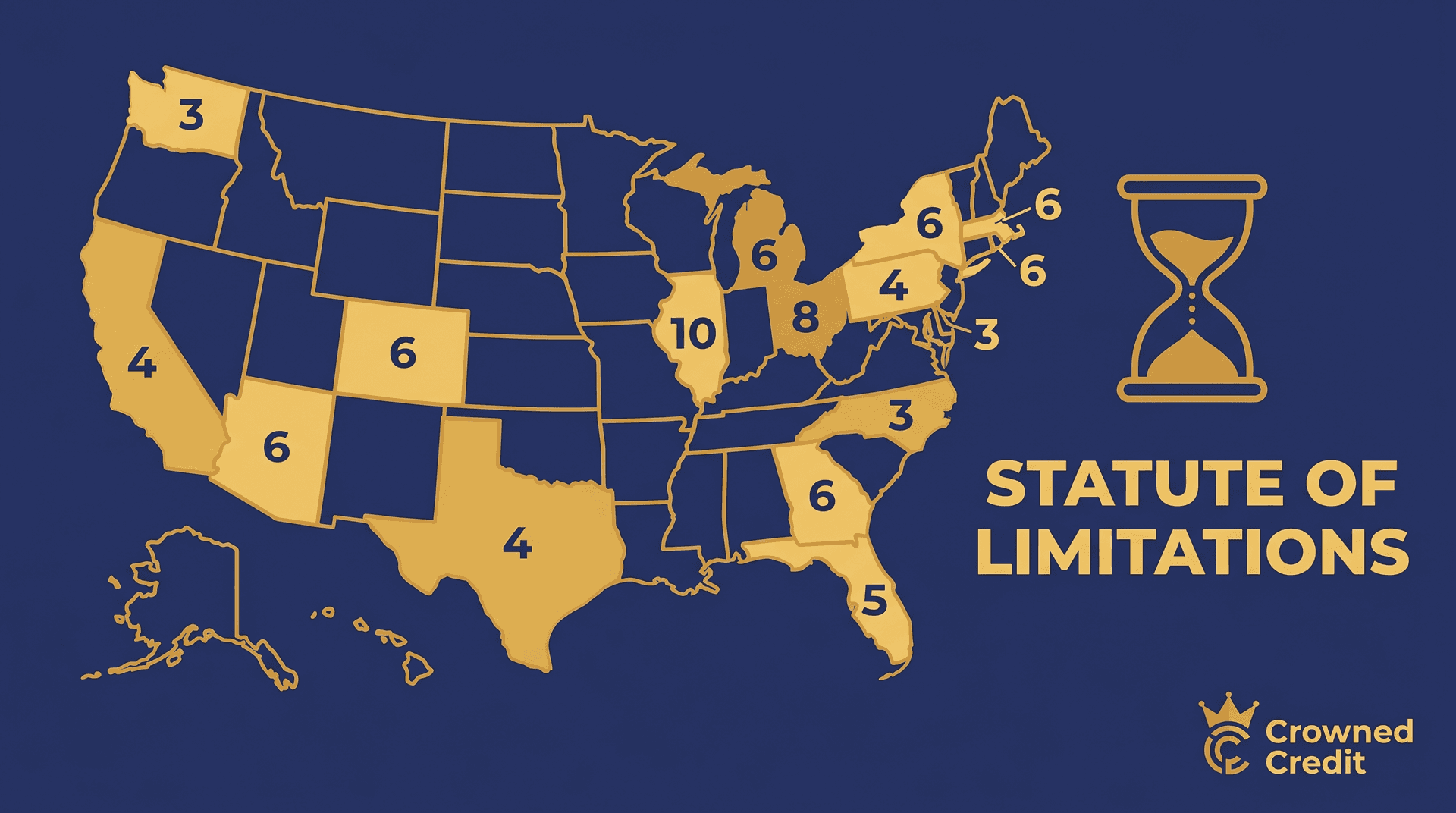

- Don't ignore LVNV completely. If the debt is within your state's statute of limitations, ignoring it means they can sue you. Check the statute of limitations in your state.

- Don't fall for a credit sweep scheme. If anyone promises to "wipe your credit clean" in days through mass disputes or synthetic identities, walk away. That's a credit sweep — and it's illegal.

Should You Pay the LVNV Debt?

It depends on three things: how old the debt is, what your goals are, and whether you can negotiate a deletion.

If the debt is old (5+ years from original delinquency), close to falling off, and LVNV can't verify it — paying may not be the right move. But if the debt is a few years old, you're planning to apply for a mortgage or car loan soon, and you can negotiate a pay-for-delete agreement at a reduced amount — then payment in exchange for removal makes real sense.

One thing to factor in: under FICO Score 9 and VantageScore 4.0, paid collections are largely ignored. But most mortgage lenders still use FICO 8 or older models, where even paid collections count against you. If you're going through a mortgage application, ask your lender specifically which scoring model they use before making any payment decisions.

How Crowned Credit Can Help

Dealing with LVNV Funding alone is doable — but it's time-consuming and requires persistence. One missed step in the validation process, one improperly worded dispute letter, or one verbal agreement instead of a written one can set you back months.

At Crowned Credit, we work these situations every day. Our team knows the FCRA and FDCPA inside and out, and we know how debt buyers like LVNV operate. We'll pull your full credit report, identify every dispute angle, send properly documented validation requests, and pursue every leverage point available under federal law.

We offer three service tiers to fit different situations:

- Essential: $150 enrollment + $99/month — great for straightforward collection disputes

- Accelerated: $249 enrollment + $199/month — for multiple negative items across all three bureaus

- Momentum: $1,095 one-time — for clients who need comprehensive credit restoration

Ready to get LVNV off your report? Book a free consultation call and we'll review your credit report together and tell you exactly what we can do. Call us at 336-310-0090 or schedule online here.

The Bottom Line

LVNV Funding LLC on your credit report isn't a dead end. It's a collection account from a debt buyer that, like any other credit entry, is subject to the verification requirements of the FCRA and the consumer protections of the FDCPA.

Your playbook:

- Request debt validation in writing immediately

- Dispute with all three credit bureaus with specific, documented grounds

- If the debt is valid and you need it gone fast, negotiate a pay-for-delete in writing

- Check the original delinquency date — if it's being re-aged, dispute it

- Know your state's statute of limitations before making any payment

The process takes time and attention to detail. But people get LVNV removed from their credit reports regularly — through disputes, debt validation, and negotiated settlements. You can too.

Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. Results from credit dispute processes vary based on individual circumstances. Crowned Credit is a credit repair organization operating in compliance with the Credit Repair Organizations Act (CROA). We do not guarantee specific outcomes or score improvements. Under the FCRA, you have the right to dispute inaccurate information on your credit report for free directly with the credit bureaus.

Share this article: